Posted by:

Admin

Date:

July 13, 2026

Category:

blogs

Budget vs Actual Reporting Explained

A budget can look perfect on paper but real business does not always follow the plan. Sales can drop, costs can rise and cash can become difficult to manage before anyone notices the problem. This is where budget vs actual reporting becomes important.

Tracking a budget properly is still not common enough. Only 51% of UK adults say they have a budget in place for 2026, up from 46% in 2025. This means nearly half of people in the UK are making financial decisions with no plan to compare against at all. For businesses, the consequences of that gap are far more serious.

Budget vs actual reporting compares planned financial figures with real financial results. It helps businesses see whether they are performing as expected. It also highlights areas where action may be needed before small problems become bigger ones.

Many businesses rely on budget vs actual reporting because it provides a clear picture of financial performance. Instead of guessing what is happening, managers can use real data to make better decisions. Later in this guide, a sample budget vs actual report will show how businesses compare planned figures with actual results.

Key Takeaways

- Budget vs actual reporting helps businesses compare planned financial figures with actual results, making it easier to spot problems and opportunities early

- The most common budget variances involve revenue, expenses, profit and cash flow, so these areas should be reviewed regularly during budget vs actual reporting

- Learning how to check the report budget vs actual can help businesses identify trends, investigate large variances and make more informed financial decisions

- A budget vs actual report template provides a simple structure for comparing budgeted and actual figures, helping maintain consistency across reporting periods

- Many small businesses start with a budget vs actual report excel template because it is affordable, easy to use and suitable for basic financial analysis

- A sample budget vs actual report or budget vs actual report example can help businesses understand how variances affect performance and what actions may be needed

- Regular budget vs actual reporting improves forecasting, strengthens cash flow management and supports better long-term business planning

What Is Budget vs Actual Reporting?

Budget vs actual reporting compares budgeted financial figures with actual financial results. The budget shows expected numbers. These numbers are made before the month, quarter or year starts.

Actual numbers show what really happened. For example, a business may plan to make £50,000 in sales in one month but at the end of the month, it only makes £45,000. The difference is £5,000. This difference is called a variance.

A budget vs actual report shows these differences clearly. It helps business owners and managers understand where the business is on track and where it is not. Without this report, money problems can stay hidden for too long.

1. Why Does Budget vs Actual Reporting Matter?

Budget vs actual reporting matters because it shows the real financial position of a business. A budget is based on expectations. Actual results show reality. When both are compared, the business can see if it is moving in the right direction.

For example, if costs are higher than planned for three months, this is a warning sign. The business can check why costs are rising and take action.

Budget vs actual reporting also supports better control. Each department can see if it is spending within budget. It also helps with planning. Future budgets become more accurate when past results are checked properly.

2. What Is Included in a Budget vs Actual Report?

A budget vs actual report usually includes income, costs, profit and cash flow. Revenue is the money earned from sales or services. Expenses are the money spent to run the business. This may include rent, wages, bills, marketing and supplies.

Profit is what remains after expenses are deducted from revenue. Cash flow shows how money moves in and out of the business.

Some reports also show separate figures for different departments. For example, sales, marketing and operations may each have their own budget.

A budget vs actual report template normally puts budget and actual figures side by side. This makes the differences easy to see.

What Are Variances in Budget vs Actual Reporting?

A variance is the difference between the budgeted amount and the actual amount. If the result is better than planned, it is called a favourable variance. For example, if sales were budgeted at £100,000 but actual sales reached £120,000, this is a favourable variance.

If the result is worse than planned, it is called an unfavourable variance. For example, if expenses were planned at £10,000 but actual expenses became £15,000, this is an unfavourable variance.

Watch Small Gaps:

Small variances can become big problems if they happen every month.

However, not every unfavourable variance is bad. Sometimes a business spends more because it is investing in growth. For example, it may spend more on marketing to bring in new customers. The reason behind the variance matters more than the number alone.

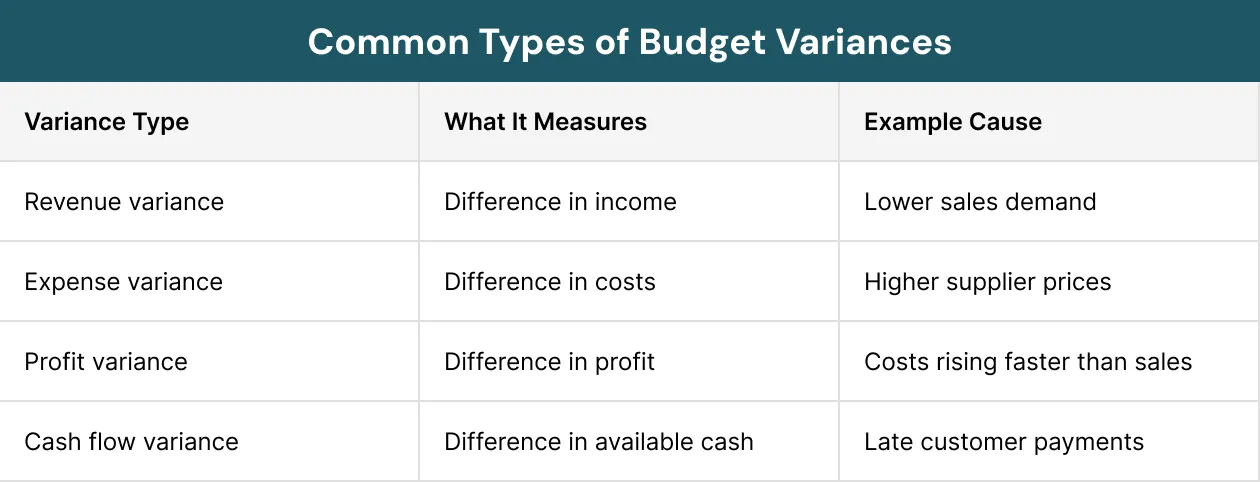

1. What Are the Common Types of Budget Variances?

The common types of budget variances are revenue variance, expense variance, profit variance and cash flow variance.

Revenue variance happens when actual income is different from planned income. This may happen because of lower sales, price changes or customer demand.

Expense variance happens when actual costs are different from planned costs. This may happen because of inflation, supplier price rises or extra business costs.

Profit variance happens when profit is different from the budget. A business may earn more sales but still make less profit if costs rise too much.

Cash flow variance happens when expected cash is different from real cash. This is important because a business needs enough cash to pay bills, staff and suppliers.

2. What Causes Budget Variances?

Budget variances can happen for many reasons. One common reason is poor planning. If the budget was not realistic, the actual results will often be different.

Market changes can also affect results. Prices may rise. Customers may spend less. Competitors may offer better deals.

Seasonal changes can also matter. Some businesses sell more in summer. Others sell more near Christmas.

Operational problems can also increase costs. Delays, waste, staff shortages and poor systems can all affect the budget.

Unexpected events can also create variances. This may include supply chain disruptions, new rules, economic changes or sudden business costs.

What gets measured gets managed.

– Peter Drucker, Management consultant & Educator

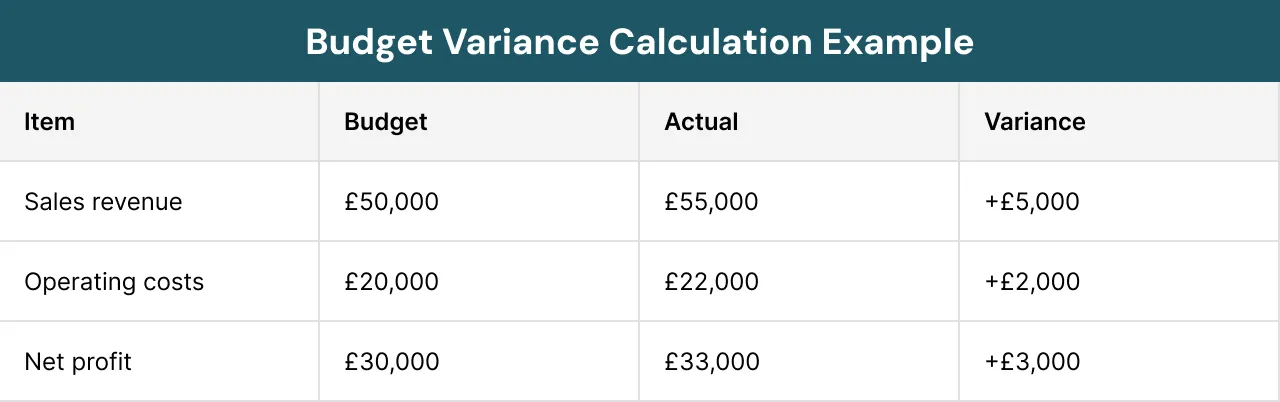

3. How Do You Calculate Budget Variance?

Budget variance is calculated by subtracting the budgeted amount from the actual amount. The basic formula is:

Budget Variance = Actual Amount − Budget Amount

For example, if monthly sales were budgeted at £50,000 and actual sales reached £55,000, the variance is £5,000. This means sales were £5,000 higher than planned.

Businesses also use percentage variance. The formula is:

Variance Percentage = (Actual Amount − Budget Amount) ÷ Budget Amount × 100

Using the same example:

- £55,000 minus £50,000 equals £5,000

- £5,000 divided by £50,000 equals 0.10

- 0.10 multiplied by 100 equals 10%

This means sales were 10% above budget. Percentage variance is useful because it shows how large the difference is compared to the original budget.

How Do You Create a Budget vs Actual Report?

To create a budget vs actual report, start with a clear budget, collect actual financial data, compare both sets of numbers, calculate variances and review the results.

Next, the business collects actual financial data. This information may come from accounting software, bank records or bookkeeping reports.

Then the budget numbers are compared with the actual numbers. The differences are calculated.

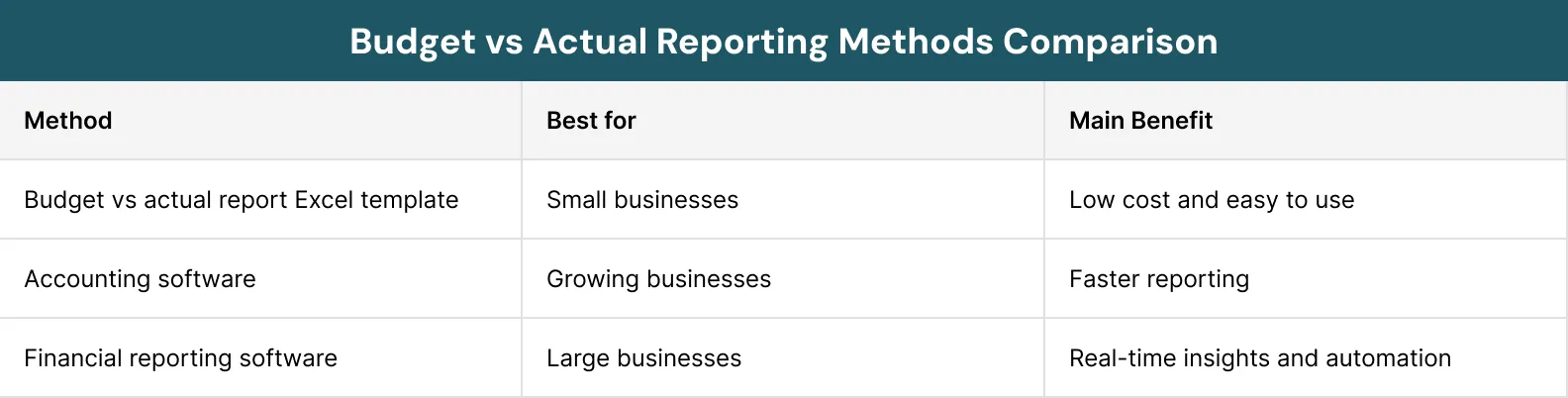

Many small businesses use a budget vs actual report excel template because it is simple and familiar. Larger businesses may use finance software. This can save time and reduce mistakes.

Reports Need Action:

A report only helps when the business uses it to make better decisions.

After the report is made, the numbers should be reviewed. Large variances should be checked first. The final step is action. A report is only useful when it helps the business make better decisions.

1. What Does a Sample Budget vs Actual Report Look Like?

A sample budget vs actual report is useful because it shows the budgeted amount, the actual amount and the variance between them. This makes it easy to see where the business is above or below budget.

For example, a business budgets for a monthly revenue of £50,000 and only manages to earn £47,000. This means revenue is £3,000 below target.

The firm also budgets £20,000 for the month’s expenditure and ends up spending £22,000. This shows that the cost of operating the business exceeds £2,000. So the business earns less and spends more. This will affect its profit adversely.

A report like this makes the problem clear. The firm will realise that the situation needs some attention. It could be due to poor customer demand, low pricing, high cost from suppliers or a poor marketing strategy.

Most businesses begin with a sample budget vs actual report before preparing their reports. Others prefer starting with a budget versus actual report template or even budget versus actual report excel template.

2. How Do You Read and Analyse a Budget vs Actual Report?

To read and analyse a budget vs actual report, check the size of each variance, look for repeated patterns and then investigate the reason behind the numbers.

Then look for patterns. If revenue is below budget for one month, it may be a short-term issue. If revenue is below budget for three months, there may be a bigger problem.

Also look deeper into the numbers. For example, sales may look low across the business. However, when checked closely, only one product may be causing the issue. This deeper review is called drill-down analysis. It helps the business find the real cause.

What Are the Benefits of Budget vs Actual Reporting?

The main benefit of budget vs actual reporting is a clear view of business performance. It shows where money is coming from and where money is going. It also helps business owners make faster decisions.

If costs are rising, action can be taken early. If sales are growing, the business can plan for more stock, staff or marketing. This reporting also improves accountability. Teams can see if they are meeting their targets.

It also helps reduce waste. When spending is checked often, unnecessary costs are easier to find. Cash flow also becomes easier to manage. A business may make sales but still struggle if cash is not available at the right time. Regular reporting helps avoid that problem.

This challenge is more common than many people realise. Research from the Chartered Institute of Credit Management has shown that in the year 2025, 82% of UK-based small to medium-sized enterprises faced cash flow problems. This shows why budget vs actual reporting is important.

Cash Flow Warning

Profit does not always mean cash is available. Check cash flow often.

What Are the Challenges of Budget vs Actual Reporting?

Budget vs actual reporting is useful but it can have problems. The first problem is poor data. If the financial records are wrong, the report will also be wrong.

Another problem is late reporting. If a report is prepared too late, the business may miss the chance to fix the issue.

Spreadsheets can also become hard to manage. A budget vs actual report excel template is useful for small businesses. However, when the business grows, errors can happen more easily.

Formulas may break. Files may have different versions. Teams may use different numbers.

Another challenge is reading only the numbers. The report shows what happened but it does not always explain why it happened.

This is why discussion and analysis are important.

How Do Real-Time Reporting and Modern Tools Improve Financial Reporting?

Real-time reporting and modern tools improve financial reporting by giving faster updates, clearer dashboards and deeper detail behind the numbers.

Old reporting often happens once a month but modern reporting can happen in real time. Real-time budget vs actual reporting means managers can see updated numbers quickly.

This helps them act faster. For example, if expenses rise in the middle of the month, the business can respond before the month ends.

Dashboards are also helpful because they show charts, graphs and key numbers in one place. This makes financial information easier to understand.

Modern tools can also help users drill down into the numbers. For example, if expenses increased by 15%, the report can show which cost caused the increase.

This saves time and improves decisions.

Which Budget vs Actual Report Template Should You Use?

The choice of template depends on the size of the company and how detailed the reporting needs to be. Small companies usually use a budget vs actual report excel template, while larger companies may need financial software.

1. Purpose of a Budget vs Actual Report Template

Many companies usually prefer to start with the budget vs actual report template as it is pretty easy. It includes budget, actual result and variance.

2. Suitability of an Excel Template

This is usually enough for a small company. The program can calculate differences and provide simple charts. If the company is larger, it may need some financial software. The right choice depends on the company size and reporting needs.

How Does Budget vs Actual Reporting Improve Forecasting?

Budget vs actual reporting improves forecasting by showing the gap between expected results and real results. This helps a business update future plans with more accurate numbers.

When a business looks at real results, it can update its future plans. For example, a business may expect £1 million in yearly sales but after six months, sales may be much lower than expected.

If the forecast is not updated, the business may keep planning around wrong numbers. If the forecast is updated, decisions become more realistic.

Some businesses use rolling forecasts. This means the forecast is updated during the year, not only once a year. This makes planning more flexible.

What Are the Best Practices for Budget vs Actual Reporting?

The best practices for budget vs actual reporting are regular review, focusing on major variances, recording reasons, comparing trends and involving the right people.

Most businesses review these reports every month. Some businesses check them weekly if money moves fast.

Focus on the biggest variances first. Not every small difference needs action.

Write down the reason for each major variance. This helps when making future budgets.

Compare results over time because one month does not always tell the full story.

Also involve the right people. Finance teams can explain the numbers, while department managers can explain what happened in daily work.

Budget vs actual reporting works better when both sides talk to each other.

What Common Budget vs Actual Reporting Mistakes Should You Avoid?

A common budget vs actual reporting mistake is ignoring small issues. A small difference may not look serious at first but if it happens every month, it can become a bigger problem.

Another mistake is ignoring good results. In case something turned out even better than predicted, it makes sense to analyse what brought about such a positive outcome.

Some businesses treat budgets as fixed documents. This is wrong since changes happen continuously in any business process. Rather, budgets should guide people in decision-making processes.

The biggest mistake is not taking action. Even a detailed report becomes useless if the business does not use the information to make better decisions.

Budget vs Actual Reporting Example

A small retail business in Manchester created a budget at the start of the year. The company expected monthly sales of £60,000 and planned operating expenses of £25,000.

After three months, the budget vs actual report showed that sales averaged only £52,000 per month. At the same time, operating expenses had increased to £29,000 because of higher supplier prices and rising energy costs.

Without regular budget vs actual reporting, the business may not have noticed the problem until much later. The reports clearly showed that revenue was below target while expenses were increasing.

Management reviewed the numbers and identified two main issues. First, a popular product line was generating fewer sales than expected. Second, supplier costs had increased by nearly 12% compared to the original budget.

The business responded by adjusting product pricing, negotiating with suppliers and increasing promotions for its best-selling products. Within four months, monthly sales increased to £58,000 and operating costs began to stabilise.

This example shows how budget vs actual reporting can help businesses identify financial problems early, take corrective action and improve future performance before small issues become larger ones.

Conclusion

A budget shows the plan, while actual results show what really happened. Budget vs actual reporting brings both together and helps a business see if it is on track.

The process does not need to be complex. A business can start with clear budget figures, collect real results, compare the numbers, check the variances, find the reasons and then take action.

A simple budget vs actual report template can be enough for many small businesses. A budget vs actual report excel template can also help organise the numbers.

Larger businesses may need software for faster and clearer reporting. Still, the goal is always the same: understand the numbers, learn from the results and make better decisions.

When used regularly, budget vs actual reporting becomes more than a finance task. It becomes a simple way to protect profit, improve planning and help the business grow in a healthier way.

Sterling Cooper understands that good financial decisions start with clear and accurate reporting. This helps businesses stay in control of their finances throughout the year.

Contact us today and let experienced professionals turn your financial data into practical insights that support smarter planning, stronger cash flow and long-term business growth.

Not sure whether your business is performing as planned? Sterling Cooper helps businesses compare budgets with actual results, uncover financial risks and make smarter decisions.

We have helped businesses improve reporting accuracy and financial visibility. Get in touch today to see how accurate reporting can help your business stay on track, reduce financial surprises and plan for future growth.

FAQs

Budget vs actual reporting compares planned financial figures with actual business results. It helps businesses understand performance, identify variances and make informed financial decisions.

Variances can be caused by changing market conditions, inaccurate budgeting assumptions, inflation, operational issues, seasonal demand changes or unexpected business events.

A favourable variance occurs when actual results are better than budgeted expectations. Examples include higher sales revenue or lower operating costs.

Yes. A budget vs actual report excel template is often suitable for small businesses because it is affordable, flexible and easy to customise.

A budget vs actual report template provides a structured format for comparing budgeted figures with actual results. It improves consistency and makes reporting easier to understand.

To check the report budget vs actual, compare the budgeted amount with the actual amount, calculate the variance and look for big or repeated differences. Then check why the difference happened. This helps a business see if income, costs, profit or cash flow are on track.

A budget vs actual report example shows planned figures beside real results. For example, if a business budgets £50,000 in revenue but earns £47,000, the variance is £3,000 below target. This helps the business see where performance is different from the original plan.

Recent Posts

Tax-Free Benefits Directors Can Claim

July 8, 2026

How to Start Investing: A Step-by-Step Guide

July 7, 2026