Posted by:

Admin

Date:

March 4, 2026

Category:

blogs

Understanding the Accounting Cycle: Step-By-Step Breakdown

Have you ever wondered how businesses can monitor all the pounds they make and spend without losing it? That is where the accounting cycle fits in.

Accounting cycle is a straightforward and well-structured process that assists companies in recording, categorising and reporting their money well. Once you learn it, you will know how all financial information fits together like the pieces of a puzzle.

Here we will explain the steps of the accounting process in a simple way. In conclusion, you will know the answer to the question: what are the steps in the accounting process?

What Is the Accounting Cycle?

An accounting cycle is the complete description and analysis of every activity in an accounting period. It is an 8-step process that gives accuracy to the financial process. In the absence of this cycle, businesses will not be able to:

- Track profits and losses.

- Know how much cash they have.

- Pay the correct tax.

- Make smart decisions.

- Avoid legal trouble.

It maintains a record of finances which is correct and well organised. This is why each company, even the small shop or global brand adheres to the steps of the accounting process attentively.

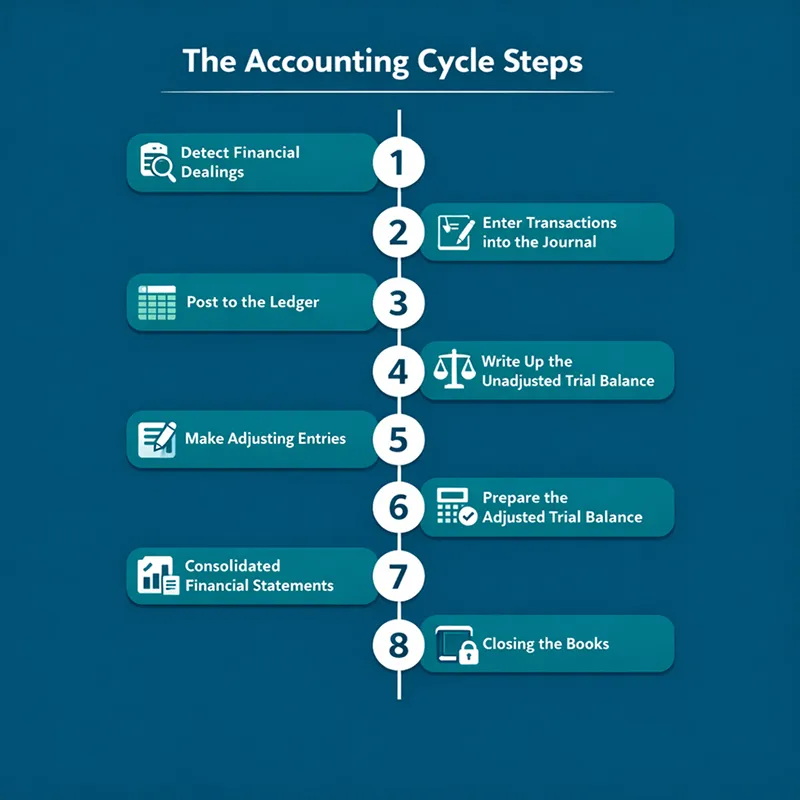

The Accounting Cycle Steps

The cycle has 8 steps. Let us take them separately and in simple terms.

Detect Financial Dealings.

Money in motion generates a transaction every time.

Examples include:

- Selling a product.

- Paying wages.

- Buying equipment.

- Receiving a loan.

The initial part of the cycle is the identification of the events that influence the business in a financial manner. Not every event counts. When one is hired, the operations are influenced but the payment of salary is the transaction.

Enter Transactions into the Journal.

After being identified, they are recorded in a journal.

This is called journalising. Each entry records:

- The date.

- The accounts affected.

- The amounts.

- A short description.

The accounting process and cycle is always based on the system of double-entry. That means:

In all transactions, there are two sides.

One account is debited, another account is credited. This maintains the books in balance.

Post to the Ledger

Upon recording of journal entries they get transferred into the ledger.

The ledger lumps together similar transactions into such accounts as:

- Cash

- Sales

- Expenses

- Equipment

- Wages

The journal, in case it is a diary, is the ledger, which is a filing cabinet. This accounting process would assist the businesses in viewing sums of money in each account.

Write Up the Unadjusted Trial Balance.

Then accountants make a trial balance.

This is nothing but a list of all ledger accounts and balances. It checks whether:

- Total debits = Total credits.

In case they do not coincide, there was some mistake in the process previously.

The trial balance will not ensure that no mistakes are made. It merely establishes the fact that debt and credit amounts are equal.

Make Adjusting Entries

There are transactions that are not registered on a daily basis. These require the adjustment of entries at the end of the period.

Common adjustments include:

- Unpaid wages and other accrued expenses.

- Expenses paid in advance (such as insurance in advance).

- Depreciation of equipment.

- Accrued income,

This aspect of the accounting process is important in ensuring that incomes and expenses are accrued within the right period.

It is based on the principle of accrual accounting which states:

- Record income when earned.

- Expenses to be recorded at the time they occur.

- Not when cash changes hands.

Prepare the Adjusted Trial Balance.

A new trial balance is prepared after recalculations. In this version, the figures are updated. It ensures:

- All accounts are accurate.

- Debits still equal credits.

This is a modified version required during the accounting cycle process prior to the preparation of final reports.

Consolidated Financial Statements.

Businesses prepare financial reports using adjusted trial balance. These usually include:

Income Statement

Indicates profit or loss within a period of time.

Financial Position (Balance Sheet).

Discloses assets, liabilities and equity.

Cash Flow Statement

Tracks the movement of cash within and out.

These reports assist the owners, investors, and banks to know the health of the company.

This phase indicates the importance of the accounting process and cycle. These reports would be misguided without the preceding steps.

Closing the Books

Closing of temporary accounts is the last operation of the bookkeeping cycle.

Temporary accounts include:

- Revenue.

- Expenses.

- Drawings.

Their balances are moved into retained earnings. After closing:

- The revenue accounts are brought back to zero.

- Expense accounts are brought back to zero.

- The new period starts fresh

- Then the cycle of accounting starts all over again.

Accounting Cycle in Real Life.

Suppose that we consider a small cupcake store.

Step 1:

The shop sells £200 of cupcakes.

Step 2:

It registers the sale in the journal.

Step 3:

The sale is recorded on Sales and Cash accounts.

Step 4:

At the end of the month, a trial balance is made.

Step 5:

The owner understands that electricity of £50 has been used but not paid. An adjusting entry is made.

Step 6:

A modified trial balance is developed.

Step 7:

A profit is to be seen in an income statement.

Step 8:

The new month is closed in terms of revenue and expenses.

This basic illustration reveals why the bookkeeping cycle ensures everything is in order.

To learn more about managing small businesses, check out our guide on how to start and manage a business.

Major Theories That Enable the Accounting Cycle to Operate.

There are some basics to know when it comes to the accounting steps.

Double-Entry System

Each debit is accompanied by a credit.

Accrual Accounting

Recognise revenue when it is earned and not when received.

Consistency

The same applies with businesses every period.

Accuracy

The process verifies the one before it.

These regulations render the accounting process and cycle dependable and dependable. You can learn more from our guide on accounting terms.

Common Mistakes.

Errors may occur even with a system.

Here are some common issues:

- Omission of recording transactions.

- Posting to the wrong account.

- Skipping adjusting entries.

- Mathematical errors.

Failure to close accounts in the right manner.

These errors are minimised by examining every phase of the bookkeeping cycle carefully.

The Influence of Technology on Changing the Financial Cycle.

Previously, it was all hand-operated. Software today accomplishes it at a faster pace.

The modern accounting software can:

- Recording transactions automatically.

- Post to ledgers instantly.

- Generate trial balances.

- Prepare financial reports.

Nevertheless, the accounting cycle process is the same. Nothing more than software automates the steps.

It is still necessary to have the bare minimum knowledge, though computers may do all the heavy lifting.

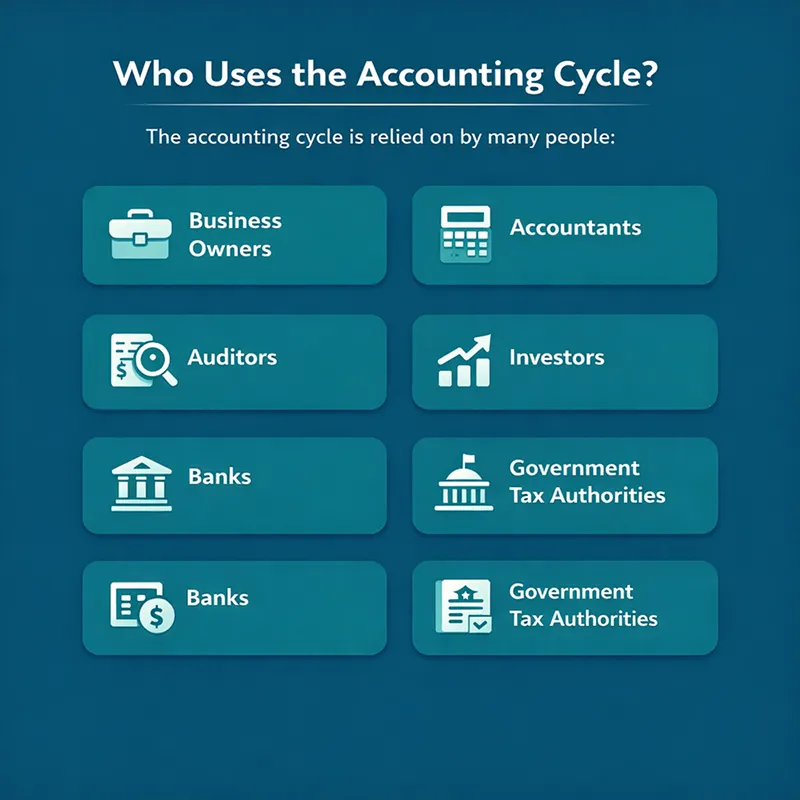

Who Uses the Accounting Cycle?

The accounting cycle is relied on by many people:

- Business owners.

- Accountants.

- Auditors.

- Investors.

- Banks.

- Government tax authorities.

It generates credible accounting data that is trusted by all.

Why Do You Need to Learn the Financial Cycle?

The accounting cycle is a basic understanding in case you are studying business or finance.

It helps you:

- Learn the way businesses quantify success.

- Read financial statements without fear.

- Study for advanced accounting subjects.

- Develop good financial consciousness.

After having knowledge of the accounting processes, more advanced-level subjects will be very easy.

The financial cycle may look long at first. But it is simply a clear system. It helps businesses stay organised and in control.

Each step builds on the one before it. Nothing is random. When the cycle is followed properly, the numbers make sense and the reports can be trusted.

Conclusion

At Sterling Cooper, we believe accounting should feel simple, not stressful. Clear systems create strong businesses. That is why understanding the accounting cycle matters more than ever.

If you want help setting up or improving your accounting process and cycle, we are here to guide you.

Contact us today and let’s make your numbers easy to manage.

Ready to simplify your accounting cycle and gain full control of your business finances?

Contact our accounting services today and let our experts guide you every step of the way.

FAQs

The accounting cycle is a step-by-step system businesses use to record and organise financial information.

It keeps financial records accurate and helps businesses prepare correct financial statements.

There are usually eight main accounting cycle steps followed in order.

The steps include identifying transactions, recording them, posting to the ledger, preparing trial balances, making adjustments, preparing statements, and closing accounts.

The journal records transactions first, while the ledger groups similar transactions into accounts.

A trial balance checks that total debits and credits are equal.

Adjusting entries ensure income and expenses are recorded in the correct accounting period.

Temporary accounts are closed and the system resets for the new period.

Yes, most businesses follow the same accounting process and cycle, even if they use software.

No, software automates the accounting cycle process, but the steps still exist behind the scenes.

It usually repeats every month, quarter, or financial year.

Recent Posts