Posted by:

Admin

Date:

April 17, 2026

Category:

blogs

How to File Your Tax Return: A Step-by-Step Guide

Are you thinking about whether to file tax return online in the UK? Are you unsure about what HMRC requires from you? Most people initially find UK tax laws perplexing, but you are not the only one.

For the tax year 2024/25 in the UK, more than 11.48 million people completed self-assessment tax returns. This is the HMRC report, which tells us how common it is to file tax return online.

It is important to understand how to file tax return if your earnings are untaxed in the UK.

If you are self-employed or running a company, it is important as well. It may seem confusing but when you break this process into simple steps, it is not hard.

In this blog, you will find a step-by-step guide on how to file tax return online in the UK.

Key Takeaways

- Ensure you understand when to file tax return, especially if you are self-employed, earn income from property or have untaxed income

- It’s quicker and less error-prone to file tax return online through the HMRC portal, where you can complete and submit your forms with ease

- If you’re wondering how do I file income tax return, you need to register for self-assessment, gather necessary documents and enter your details into the HMRC system before submission

- Not everyone needs to do I need to file a tax return; generally, only those with untaxed income, self-employment or other specific situations require filing

- Do pensioners need to file a tax return? Pensioners may need to file if they have additional untaxed income, such as rental income or dividends

- Avoid penalties by correctly filing a tax return on time and keep in mind the specific deadlines for submission and payments to stay compliant with HMRC

- Be aware of the deadline to file tax return, which for online submissions is January 31st after the tax year ends and make sure you meet it to avoid unnecessary fines

What Is Tax Return in the UK?

The paperwork you submit to HMRC to record your income is called a tax return. It aids in determining your tax obligation. In the UK, this is typically accomplished with the use of a self-assessment system.

It includes all of your income information, such as rent and self-employment revenues. It also includes dividends, savings and other untaxed income. You can also claim costs and deductions to minimise your tax bill.

When you file tax return, HMRC tells you how much you must pay by working it out. In some cases, you may even receive a refund instead.

With the help of the tax return, HMRC checks your total earnings for the tax year. The purpose of this is to ensure you pay the accurate amount of tax.

Who Needs to File Tax Return in the UK?

When you hear the term ‘file tax return’, your first thought is, ‘Do I need to file tax return?’. It is not necessary for everyone living in the UK to file tax return. The majority of people use PAYE to make their payments. Under this system, taxes are automatically subtracted from wages or pensions.

However, you must file tax return if you have earnings that are not taxed at source. For this reason, most people need to complete a self-assessment tax return.

Generally, you will need to file tax return in the following cases:

Self-Employed (The £1,000 Rule)

If you make more than £1,000 from self-employment in a tax year, you must file tax return. This includes freelancing, side employment and owning a small business.

If your income is under £1,000, you may not need to file due to the trading allowance.

Landlords and Property Income

If you make money by renting out property, you must report it. This includes:

- Renting a house or flat

- Renting a room

- Holiday rentals

Even small rental income must be declared to HMRC.

Company Directors (PAYE + Dividends)

You may have to file tax return if you are a director of a company. This occurs when you:

- Take a salary through PAYE

- Take dividends from the company

Dividends are taxed differently from income, so they need to be reported.

Large Income Earners (£100,000+)

If your yearly income is above £100,000, you must file tax return. This holds even if you have already used PAYE to clear your taxes.

Foreign Income or Overseas Residents

You must file tax return if you:

- Earn income from outside the UK

- Live abroad but have UK income

This includes foreign salary, rent or investments.

Capital Profits (Shares, Crypto, Real Estate)

You might have to report it if your source of income is from the sale of assets. This covers:

- Shares

- Cryptocurrency

- Second property

This is called Capital Gains Tax and must be included in your return.

- You make more than £1,000 from self-employment

- Your property provides rental income

- Your investments, dividends and savings generate income

- You receive income from another country

- You have more than one income source, for which tax has not been fully paid

Also, if your income is not taxed through PAYE, you may need to file. To illustrate, HMRC may need a return if your income is higher than £100,000.

You may also be required to file in certain situations and roles. These cover:

- If you are a business partner

- If you are the director of a company and are taking dividends

- If you are handling a trust or are a trustee

- If you are part of certain organisations, such as Lloyd’s

There are situations where HMRC can ask you directly to file a return. Even if you think you don’t need to, you must complete it upon receiving one.

You might be asked to file a tax return even if you think you don’t need to. The purpose of this is often to claim a tax refund.

You might be eligible to claim money back in the following circumstances:

- If you paid too much tax through PAYE

- You incurred costs related to your work

- You made pension contributions

- You contributed to welfare schemes

To have specific benefits, HMRC may also ask you to file tax return.

If you are not sure, it is good to have an early check. Failing to meet the requirement can lead to charges and additional stress later.

If you want tax‑saving, you can follow top tax saving tips.

HMRC Tools and Resources to File Tax Return

These tools are helpful:

- HMRC Self Assessment portal

- Tax calculator

- UTR recovery tool

- Eligibility checker

Using these tools makes filing easier and faster.

Step-by-Step Guide on How to File Tax Return in the UK

When you are going to file tax return, it may seem hard. If you follow all the steps given here, it will get easier. I have listed the key steps after careful research. Following them will make filing smoother:

Step 1: Identifying if You Need to File Tax Return

You must first decide if you need to file tax return online. If in doubt, check as soon as possible to prevent further fees. The following circumstances must be met for you to file a tax return:

- If you run your own business and your income is over £1,000

- If your income comes from rent or investments

- Your income is not taxed directly

- Have a notice from HMRC

Step 2: Registering for Self Assessment

Registering for self-assessment is for those who need to file tax return online for the first time. After the tax year ends, make sure to register by 5 October.

Follow these steps to register with HMRC:

- Go to the HMRC website

- Choose “Register for Self Assessment”

- Create a Government Gateway account

- Fill in your personal details

- Submit your registration

What Is a Government Gateway Account?

This is your HMRC account online. You use it to:

- File your tax return

- Check your tax bill

- Send messages to HMRC

When you make an account, you will receive a user ID and password.

UTR Number

Unique Taxpayer Reference is referred to as UTR. You are identified by this ten-digit number.

After you register, it will be sent to you by post. It often arrives in ten to fourteen days.

Already Registered Before

If you already filed, you do not need registration again. In simple words, for signing in, use the previous login details.

You can retrieve your UTR or log in on the HMRC website if you have forgotten it.

Once you have registered, you will be given a unique taxpayer reference (UTR). You will also get access to your online account. In order to file your tax return online, you must also create a Government Gateway account.

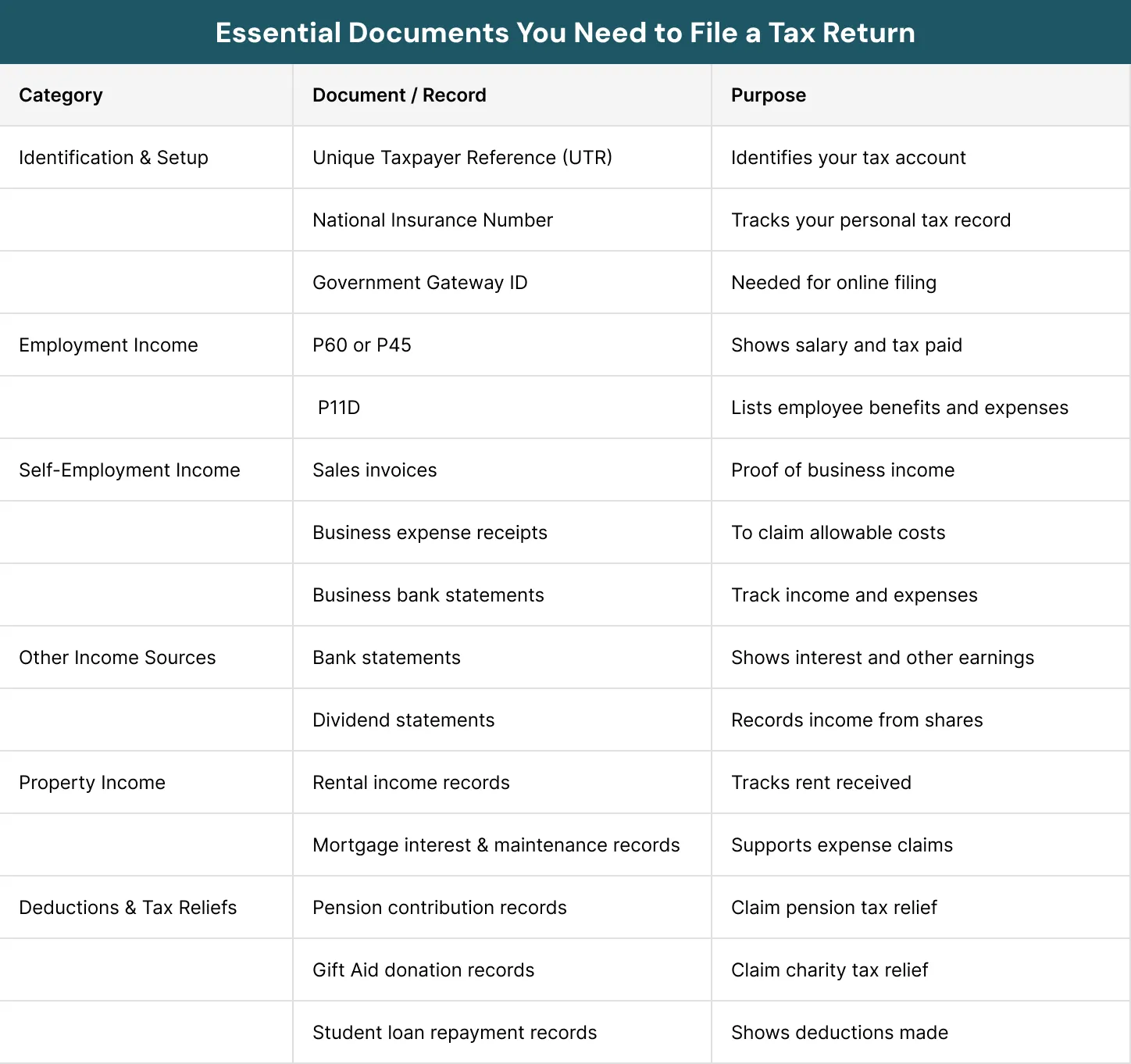

Step 3: Collecting Your Documents

Collect all required documents before going to the next step. This stage is essential because it saves time if everything is organised. This is also helpful to avoid mistakes, which could lead to major issues. The table below shows the documents you need to file tax return.

Keeping a clear record of all your expenses and payments is important. This is helpful for reporting correct figures and avoiding errors in your tax return.

Step 4: Signing in and Accessing Your Tax Return

Use your Government Gateway details to log in to the HMRC service. In case of signing in for the first time, verify your identity. Once logged in, open your self-assessment form.How to File Your Tax Return on HMRC Portal:

Follow these simple steps:

- Log in to your Government Gateway account

- Go to “Self Assessment”

- Open the tax return (SA100 form)

- Choose the salary types (job, self-employment, rent, etc.)

- Fill in each section carefully

- Save your progress as you go

- Check for errors before submitting

Step 5: Completing the Relevant Sections

The main form is SA100. It includes:

- Dividend and savings earnings

- Pension money

- Student loans

- Tax allowances and reliefs

After reviewing all the sections, you will identify which one applies to you. After this, you may have to fill in the extra sections for:

- SA102: employment

- SA103: self-employment

- SA105: property income

- SA106: foreign income

- SA108: capital gains

While filling in the forms, ensure you include all your earnings. You must mention it, regardless of the amount.

Step 6: Mention Details of your Income and Expenses

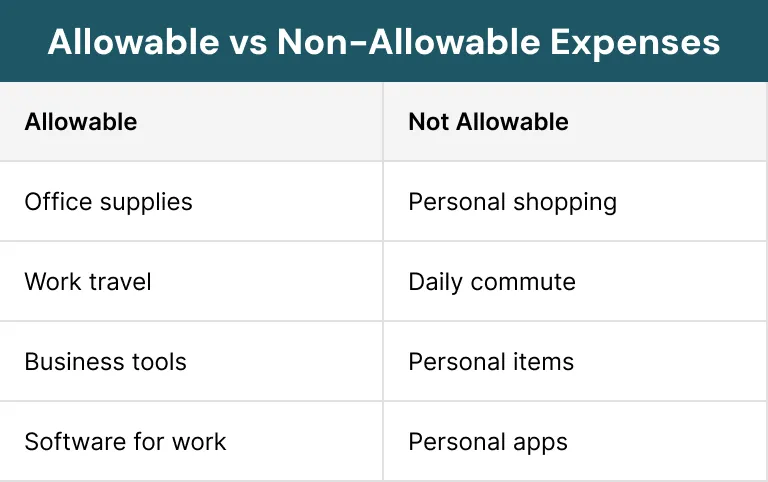

Enter the correct details in the income sections. First, report your total earnings (turnover) if self-employed. After that, add any allowable expenses.

To avoid complications later, only claim valid business expenses.

You can reduce your tax bill by claiming valid expenses. You can claim the following expenses:

Home Office Expenses

You can claim the following things if you work from home:

- Electricity

- Internet

- Work space use

HMRC also allows a simple flat rate method.

Mileage vs Fuel Costs

You can choose one method:

- Mileage rate (fixed rate per mile)

- Actual fuel cost

Using both at the same time is not recommended.

Simplified Expenses

HMRC allows fixed rates for:

- Working from home

- Vehicle use

This makes filing easier.

£1,000 Trading Allowance

You may not have to report your business revenue if it is less than £1,000. If you are above income wise, you may still use this allowance to cover expenses. It includes:

- Professional charges

- Business tools

- Travel related to work

- Office expenses

Step 7: Final Check

Make sure you go over your return in detail before submitting it. Pay close attention to the details because mistakes can lead to fines or delays. Check for:

- Inaccurate figures

- Expense claims that are not valid

- Incomplete details

Step 8: Submitting Your Tax Return Online

Your form will be able to be submitted when you double-check your information. Online form filling is a quick way and there are fewer chances of mistakes. After submission, you will receive:

- Your tax bill summary

- Confirmation of submission instantly

Step 9: Reviewing Your Tax Bill

After submission, HMRC will compute your tax. Be sure you are aware of the deadline for payment. This may include:

- Payments on account

- Income tax

- National Insurance

Step 10: Paying Your Taxes on Time

Your tax payment is due on 31 January. You may split your payments between 31 January and 31 July.

You will avoid additional penalties and interest if you pay on time. You can pay using the following:

- Direct debit

- Credit or debit card

- Bank transfer

Step 11: Keeping Your Records

After filing your tax return, you must maintain all records for a minimum of five years. This is because HMRC may ask to see these documents later. These records contain:

- Bank statements

- Expense records and receipts

- Your tax return

Step 12: After You Submit Your Tax Return

Once you submit your tax return, HMRC will evaluate it. The process is as follows:

HMRC Review Process

HMRC computes your tax bill and confirms all of your information. They might get in touch with you if they need further information.

Tax Refunds

HMRC delivers tax calculation letters, commonly known as P800s, to those who are owed an income tax refund.

If you paid too much tax, you may be eligible for a refund. This is often sent within a few weeks.

HMRC delivered over 4 million income tax refund letters between June and August of 2025.

How to Amend Your Return

If you made a mistake, you can correct your return. You can make changes for maximum of 12 months.

Records Should Be Maintained

Documents should be kept for a minimum of five years. This includes:

- Receipts

- Bank statements

- Tax returns

Common Issues While Filing Tax Return Online

While filing the form regarding tax return, you may encounter these issues:

- Session timeout if you stay inactive

- Missing income sections

- Wrong figures entered

When you complete your work, always save it and check it carefully before final submission.

Benefits of Filing Your Taxes Early

There may be problems if you wait until the last minute to file your taxes. To make the procedure easier and less complex, use a more structured approach. File early and enjoy the following benefits:

- Correct errors promptly

- Plan your payments effectively

- Avoid stress

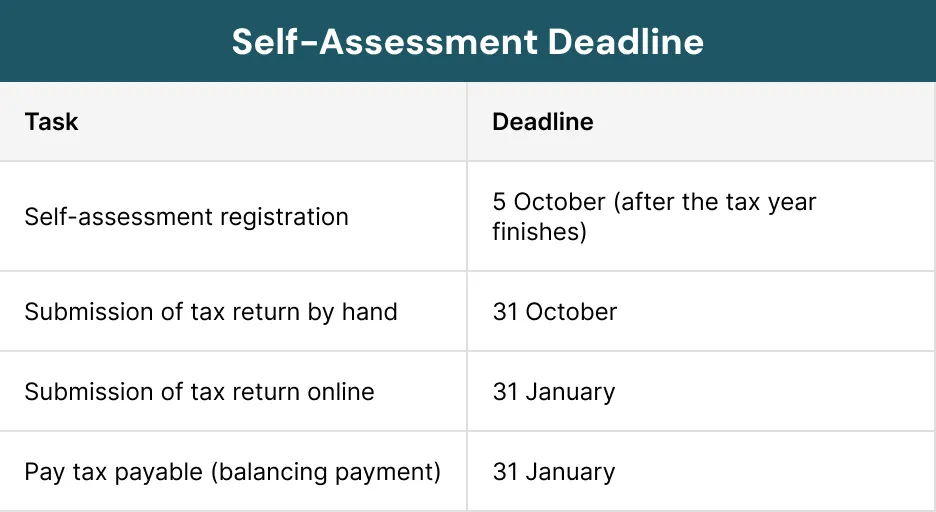

Deadline to File Tax Return

Understanding your tax dates helps avoid penalties and manage finances better. If you ever miss the deadline to file tax return, it will result in charges, extra stress and interest. Some important dates are mentioned here:

UK Tax Year

The tax year in the UK is from April 6 to April 5. Your return must include all earnings within this period.

Self-Assessment Due Date

It is essential to remember the due date to avoid any further difficulties. If you complete the forms online, you will get extra time and quicker confirmation. The key dates are given in the following table that you must remember:

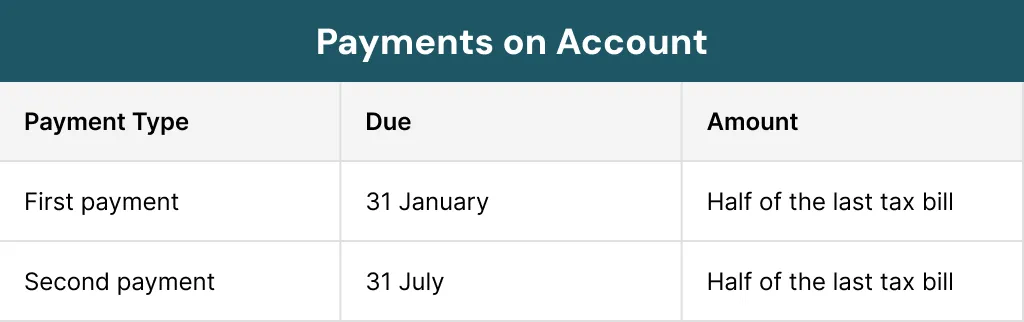

Payments on Account

You might have to pay in advance for the next year if your tax bill exceeds £1,000. These amounts are as per your last tax bill. If you are unable to pay in full at once, it may also be beneficial to make two installment payments. The following table contains the details:

Balancing Payment

After paying tax on account, if any tax remains to be paid, this is called a balancing payment. It includes:

- The previous tax year

- The 31 January deadline to file tax return

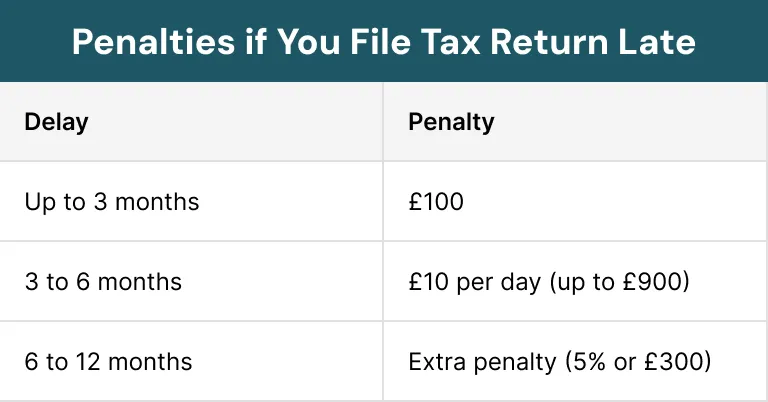

Penalties on Late File Tax Return

If you don’t pay the tax on time, it will result in fines and penalties by HMRC. There is also a greater likelihood that HMRC will inspect your return more thoroughly.

Interest on Late Payments

HMRC charges interest on unpaid tax. The longer you delay, the more you pay.

Time to Pay Option

If you cannot pay, you can contact HMRC. They may allow you to pay in installments.

Claim a Penalty Relief

In case you have a valid reason, you can appeal, such as:

- Serious illness

- System issues

- Family emergency

Key Reminders:

- Pay early if the deadline falls on a weekend or bank holiday

- Give bank payments time to clear

- File early to fix errors and plan your payments

Why Do Business Owners Consider Hiring an Accountant to File Tax Return?

Most of the business owners hire a professional to file tax returns to save time and avoid errors. Managing income and working solo can be tough. An accountant can help you understand tax rules and ensure accuracy. Tax rules change over time. Without the help of an expert, keeping up with all of this becomes difficult.

Another great advantage of hiring a professional is their accuracy. They help significantly in reducing fines, missed deadlines or the chance of errors. In addition, they also ensure that you have included all allowable reliefs and expenses. These are essential to include because they help reduce your tax bill.

They are also helpful in saving you time. You can focus on running your business instead of spending more time handling these taxes. Most business owners find hiring an accountant to be highly beneficial.

These experts support you in many other ways as well. For example:

- Guide you in planning your taxes

- Provide advice on your expenses and income

- Manage communication with the HMRC

- Assist if there is a tax enquiry or issue

The cost of hiring a professional to file a tax return depends on its complexity and the size of the firm.

In the UK, typical fees are as follows:

- For small to medium firms, the fee is typically £100 to £200 per hour

- For a simple tax return, it’s near £250 to £300

In most cases, self-employed individuals might be able to claim an expert’s fees as a business cost. This applies if the work is completely related to their own business revenue.

While there is an additional cost to hire an expert, it has many perks. With the help of this strategy, you can save time, avoid mistakes and ensure all the details are correct. Many people choose an accountant for peace of mind.

Common Mistakes to Avoid When You File Tax Return

Be aware and avoid mistakes for a smooth filing. Some of the most frequent errors are:

Incomplete Income

Most people ignore all sources of income like interest from savings, rental income, dividends and freelance work. To avoid any fines, it is important to mention every type of income source.

Inaccurate Claims for Expenses

Differentiate between business expenses and personal expenses. If you claim personal costs as business expenses, it will lead to complications. Only business-related costs should be included. Examples include work travel costs and office supplies.

Ignoring Small Income Sources

While working on a tax return, include even the smallest amounts of income. Such earnings could be from any side jobs or interest on savings. They may be so minor that they could be ignored but all of them must be reported to HMRC.

Not Reporting All Benefits

You must include all benefits when you file tax return. For example, some employer-provided bonuses are also taxable and must be added. Don’t forget to declare all the taxable perks to ensure you pay the correct amount of tax.

Incorrect Figures or Calculations

Calculation or data entry errors can cause mistakes or delays in your tax bill. Recheck all sections for accuracy and make corrections to reduce the risk of audits or penalties.

Overpayments Can Happen If You:

- Are on the wrong tax code (due to incorrect HMRC data)

- Switch jobs and get paid twice in the same month

- Start receiving a workplace pension

- Receive Employment and Support or Jobseeker’s Allowance

Missing Deadlines

Late filing leads to fines and stress. Always track key dates.

Not Keeping Records

Without records, you may face problems if HMRC checks your return.

Wrong Tax Code Assumptions

Do not assume your tax code is correct. Always check it.

Criticism of UK Income Tax

The UK income tax system has been critiqued for a variety of reasons. While it generates significant money, many experts and taxpayers see fundamental faults. Few are discussed below:

Complex and difficult to understand

Many people find the tax system overly confusing. It features multiple tax bands, laws and terms that are difficult to understand. This often causes uncertainty and concern, particularly among first-time taxpayers.

The 60% Tax Trap (£100,000–£125,000)

One of the most significant worries is the so-called “60% tax trap.” When income exceeds £100,000, the personal allowance is lowered. For every £2 earned, £1 in allowance is lost. This results in an extremely high effective tax rate, which can approach 60% (or even more with National Insurance).

Unexpected Tax Cliffs

The system has abrupt cut-offs. For instance, losing tax-free allowances or child benefits may result from exceeding specific income thresholds. This implies that people may occasionally become worse off after earning a little bit more money.

High Earners’ Tax Pressure

The top tax rate, according to some detractors, impacts more people than it was intended to. More taxpayers are forced into higher tax bands when salaries rise in tandem with inflation. Working professionals are burdened more as a result.

Unequal Income Treatment

The system is unfair, according to organisations like Tax Justice UK. Work-related income is frequently subject to higher taxes than wealth-related income, such as dividends or capital gains. Rich people may benefit more from this than average workers.

Rising Overall Tax Burden

According to recent reports, the UK tax burden is rapidly increasing. A higher share of national income is now taxed, putting pressure on people and businesses.

The power to tax is the power to destroy.

– John Marshall, Jurist

Weak Growth Incentives

Some experts argue that the system does not strongly inspire people to work more, invest more money or expand their firms. High marginal tax rates might diminish motivation to earn extra money.

Challenges for High-Earners with Shares

People who earn income from shares or stock options may confront difficulties. They may be required to pay taxes on profits they have not yet earned in cash, particularly if they are unable to sell the shares quickly.

Final Words

It is not a difficult process to file a tax return. A simple process makes it easy.

First, check if you need to file. After this, collect your documents and register with HMRC if required. Then, enter your data in the appropriate fields and file tax return online.

Before submitting your data, ensure it is thoroughly checked. Once you have completed this step, review your tax bill and make your payment before the deadline to file tax return. Your records must be kept for at least five years and include all your income.

Avoid common errors and check if you’re eligible for a refund. Small mistakes can lead to fines or lower refunds, so check in time if unsure.

Sterling Cooper understands that filing taxes can be tough for some people. We provide services to make the process clear, simple and manageable.

Contact us today if you need assistance with filing a tax return.

Confused about whether you need to file a tax return or how to avoid mistakes with HMRC?

We have successfully assisted individuals and business owners in understanding and filing tax returns accurately. We guide you through checking your tax status, preparing your return, and avoiding penalties with clear, actionable steps.

Reach out today for clear support and hassle-free filing.

FAQs

Check if you need to file a self-assessment with HMRC, then register if required.

Gather all income details and submit your tax return online through HMRC, making sure to check and pay any tax due before the deadline.

You need to file a tax return if you have untaxed income such as self-employment earnings over £1,000, rental income, dividends, savings interest or foreign income.

You may also need to file if HMRC asks you to or if you are a company director, partner, trustee or claiming certain tax refunds or benefits.

Most pensioners do not need to file a tax return in the UK if their income is only the State Pension and taxed through PAYE.

However, they may need to file if they have extra untaxed income, such as private pensions, rental income, savings interest or if HMRC asks them to complete a self-assessment.

Preparing early helps you meet deadlines and avoid penalties, interest charges, underpaying or overpaying tax. For the 2024/25 tax year, submit paper or online tax returns by 31 October 2025 or 31 January 2026, respectively.

Understand typical self-assessment tax return cost across the UK, with most accountants charging £150 to £350 for a standard return and higher costs where income sources or structures are more complex.

Recent Posts