Posted by:

Admin

Date:

May 6, 2026

Category:

blogs

How to Read Financial Statements: A Simple Guide for Non-Accountants

Have you ever wondered how to check your business’s financial health?

Knowing financial statements is vital. However, many people don’t grasp what financial statements mean.

In the FinWell Index 2025, young adults aged 18‑24 secured an 87.7 score in financial health. This score is lower than that of older age groups. This shows that younger UK adults may find it harder to know basic financial management and information.

There are three main financial statements to read. You will explore them here in detail, one by one.

These financial statements give key insight into your company’s financial position, production and cash flow.

For instance, a balance sheet tells what a company owns and owes. On the other hand, the income statement shows how much profit the firm produces over time. In addition, the cash flow statement tells whether the company has enough money to pay its bills.

In this blog, you will learn how to read financial statements. Also, you will be able to make smart business or investment choices.

Key Takeaways:

- How to read financial statements is essential for understanding your business’s financial health

- Start with how to read a financial statement of a company, focusing on assets, liabilities, and equity

- Reading financial statements helps you assess a company’s profitability and cash flow

- Use the balance sheet to track what a company owns and owes, and how do I read a balance sheet to understand its financial position

- The income statement shows how much profit or loss a company has made

- The cash flow statement reveals if the company has enough money to cover its bills

- Regular reading of financial statements is key to making informed business decisions

- Understanding financial statements is crucial for making smarter business and investment choices

What Are Financial Statements?

Financial statements are official data of a business’s or a person’s economic position and activities. They provide a review of the money dealings and goings-on of a company over a period of time. For firms, financial statements assist in getting loans, tracking performance and attracting investors. Its main types include:- Balance sheet

- Income statement

- Cash flow statement

Did You Know?

Financial statements are not just for accountants. Business owners and investors use them to make crucial decisions about growth, investment, and financial planning. Knowing how to read these statements can save you time and money in the long run.

Why Are Financial Statements Important?

Business owners, employees, managers and investors see the progress of a company with the help of financial statements. They use these details to make better decisions. They give crucial data about cash flow, profit, debt and how smoothly the business runs.

Consider an example, if an investor wants to buy stock, they will study the balance sheet. The purpose of this is to check the firm’s financial position. They will also look over the income statement to analyse profit trends.

On the other side, a business owner might also check the cash flow statement. With the help of this, they will know that the business has enough money to pay its bills.

In addition, knowing financial statements is also good for handling accounts.

Knowing how to read financial statements is one of the most valuable skills an investor can possess. They provide essential insights into a company’s financial health, helping to make informed decisions about the future.

Warren Buffett

How to Read Financial Statements?

To understand financial statements, each document should be reviewed separately. All these statements are important for assessing your business’s financial position. Let’s begin:

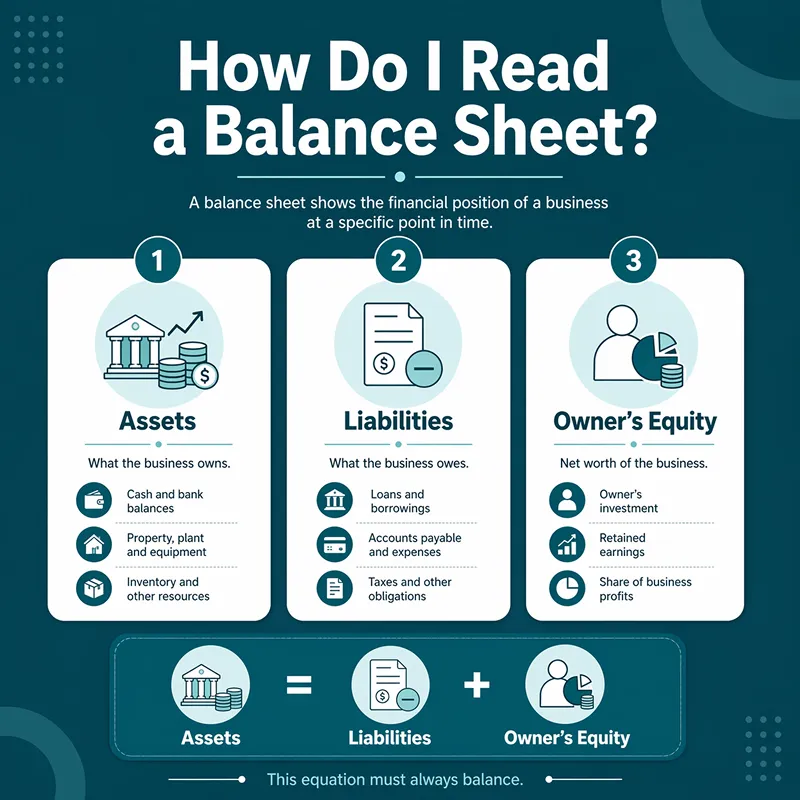

How Do I Read a Balance Sheet?

If you want to know the firm’s financial position at a certain time, the balance sheet needs to be read. It explains to you what the company owns (assets) and what it owes (liabilities). Besides this, it also shows shareholders’ equity (the difference between liabilities and assets).

If you want to know how do i read a balance sheet, the given formula will help you:

Assets = Liabilities + Owner’s Equity

The main parts of a balance sheet are given below:

1. Assets

The valuable things a company owns are called assets. They are divided into:

Current Assets

The assets of a company that can be transformed into cash in one year. Their examples are cash, inventory and accounts receivable.

Non-Current Assets

The long-term assets are called non-current, such as property, equipment and patents.

2. Liabilities

The debts that the company has to pay are called liabilities. They are divided into two groups:

Current Liabilities

These are the short-term debts, such as short-term loans and accounts payable.

Non-Current Liabilities

Mortgages or long-term loans are examples of long-term debts.

3. Owner’s Equity

This term is called the net worth, too. It represents the value left for shareholders when all the debts are paid. It is worked out as:

Owner’s equity is found by subtracting debts from assets.

You can know its financial stability by comparing its assets, debts and equity.

If a business has £500,000 in assets and £200,000 in debts, its value is £300,000 (£500,000 – £200,000). This tells that the company’s value is £300,000 after submitting all its debts.

Pro Tip

When reading a balance sheet, always compare current assets with current liabilities to assess the company’s short-term financial health. A current ratio above 2 is generally considered a good sign of financial stability.

How Do I Read an Income Statement?

The other name of the income statement is also the profit and loss statement. It shows, at a certain time, how much profit or loss the business made. This can be a month, quarter or year. You can find out the net income by taking out expenses from revenue.

The income statement includes:

Revenue

The total money the company receives from sales or services is called revenue.

Cost of Goods Sold

It is the direct cost involved in creating the products or services the business offers.

Gross Profit

You can find the gross profit by subtracting the cost of goods sold from sales.

Operating Expenses

These are the expenses needed to run the business, such as utilities, salaries and rent.

Operating Income

You can find out operating income by subtracting operating expenses from gross profit.

Net Income

Net income tells the final profit or loss after all expenses, including taxes and interest, are subtracted.

If a firm makes £1 million and spends £600,000, the profit is £400,000. This is the business’s profit after all values are subtracted.

How Do I Read a Cash Flow Statement?

The cash flow statement shows how money comes in and goes out of a firm. It helps you review whether the firm has enough cash to pay its bills and progress.

Key components of the cash flow statement are given below:

Operating Activities

It is the cash flow from the company’s main business activities, such as payments and sales to suppliers.

Funding Activities

Cash flow from buying and selling lasting assets, like property or equipment.

Financing Activities

Cash flow from raising money (like selling stock) or paying off debts (like loans).

A firm would have £150,000 in cash if it makes £200,000 from operations and spends £50,000 on equipment.

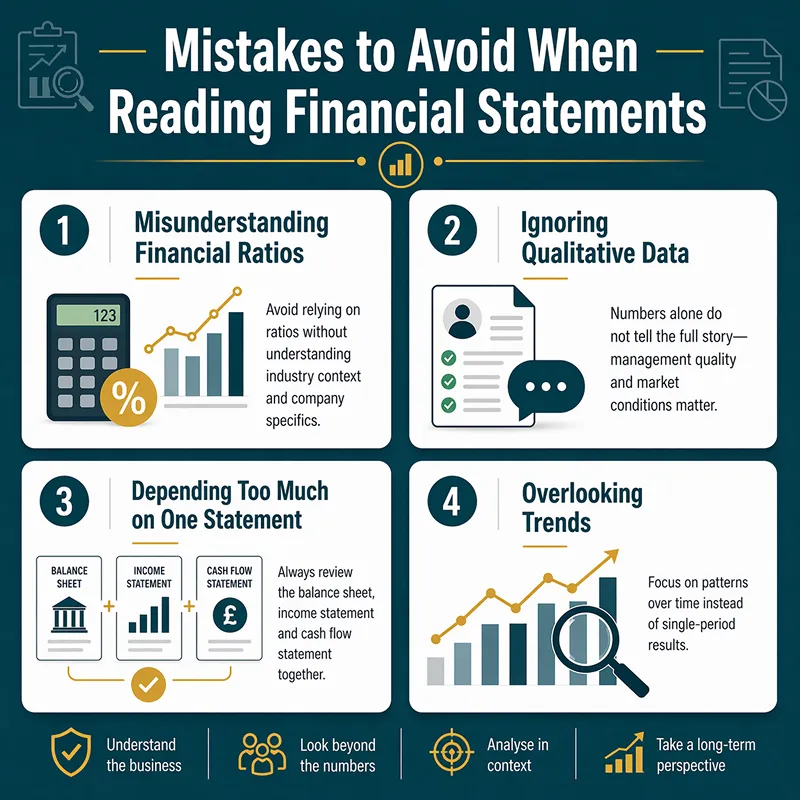

Mistakes to Avoid When Reading Financial Statements

When reading financial statements, avoid the following mistakes:

Misunderstanding Financial Ratios

Ratios like the current ratio are helpful, which is current assets divided by current liabilities. However, you should not look at them only. If a ratio is low, it could mean liquidity issues. On the other hand, it might also indicate that a firm is investing in growth.

Ignoring Qualitative Data

You will not understand the full story from financial statements only. Market situation or management changes can have a huge impact on the company’s performance. These may not be visible in the numbers.

Depending Too Much on One Statement

Among these three major financial statements, each one provides different details. If you rely on just one, it will result in a misguided understanding of the company’s financial health.

Overlooking Trends

One-time events might not tell the complete performance of the company. Therefore, you should also look at trends over time. This is helpful in understanding if the firm is improving or getting worse.

How to Analyse Financial Statements Effectively?

To know the finances is one thing, but interpreting them is another. I have explained below how to get the most from your financial statements.

How to Analyse a Balance Sheet?

The balance sheet shows a company’s financial state at some time. Focus on areas:

Current Ratio

You can achieve this ratio by dividing current assets by current liabilities. It will explain if the firm has enough assets to cover temporary debts. If a ratio is above 2, it is considered good. It means the business has twice as many assets as liabilities.

The current ratio can be calculated by dividing current assets by current liabilities.

For example, the ratio will be 2 if a firm has £500,000 in assets and £250,000 in debts. This tells a good position.

Debt-to-Value Ratio

This ratio compares a company’s total debts to its owners’ value. This represents how much the business depends on debt compared to its own equity.

Its formula is given below:

Debt-to-value ratio = total liabilities ÷ shareholder equity

For instance, if a business has £1 in debt for every £1 in value, the ratio is 1. If the ratio is over 1, it means the company depends more on debt.

Quick Ratio

You can also call the quick ratio the acid-test ratio. It checks if a firm can pay temporary debts without selling inventory.

The quick ratio can be calculated by first subtracting inventory from current assets. After this, divide it by current debts.

For example, if a business has a quick ratio of 1 or more, it means the firm can pay its temporary debts without selling inventory.

How to Analyse an Income Statement?

The income statement tells us how much profit a company is delivering. It focuses on:

Gross Profit Margin

This shows how much money is left after subtracting the expense of goods sold (COGS). This will tell you how efficiently the firm makes its goods or services.

Gross profit margin = (revenue – COGS) ÷ revenue × 100

The margin is 60% if sales are £500,000 and COGS is £200,000. This means the business keeps 60% of its sales after production costs.

Net Profit Margin

This margin will tell you the percentage of revenue left after all expenses. This includes taxes and interest and shows the company’s overall profitability.

Its formula is as follows:

Net profit margin = profit ÷ sales × 100

For instance, the margin will be 10% if profit is £50,000 and sales are £500,000. This means the business keeps 10% as profit.

Operating Income

With this income, we become aware of how well the company is working in its core operations. It keeps out income and expenses from things like taxes or interest.

Operating income = gross profit – expenses

Consider an example, operating income is £150,000 if gross profit is £300,000 and expenses are £150,000.

How to Analyse a Cash Flow Statement

You can read the cash flow statement to know how cash is being generated and used. It’s key to know a company’s ability to grow, invest and pay bills.

Operating Cash Flow

This tells about how much cash the firm makes from regular business activities. A positive number shows the business can cover its costs.

Calculate it by:

Operating cash flow = cash from business – cash from working capital changes

The cash flow will be £150,000 if a firm makes £200,000 but has a £50,000 increase in working capital.

Free Cash Flow

Free cash flow is the cash left after a business has paid for capital expenditures like equipment or property. It’s vital for investing again or returning money to shareholders.

You can find it by:

Free cash flow = operating cash flow – money spent on assets

Free cash flow will be £150,000 if operating cash flow is £200,000 and asset spending is £50,000.

Cash Flow from Financing Tasks

This represents cash increased through debt or equity or cash used to settle debts and dividends. It helps you check how the firm is financing itself.

For example, if a company issues stock and increases £100,000, this will be indicated as a cash inflow in financing activities.

Vodafone Annual Report: Case Study

Vodafone is amongst the biggest phone companies in the United Kingdom. Every year, Vodafone publishes a report with all its financial information.

This report shows how much money Vodafone earned, spent, and the profit it made. In addition, there is also some information about the firm’s debts and cash flow.

This report includes:

Revenue

How much income Vodafone earned from its clients.

Profit

After paying for the costs, the amount left.

Cash Flow

This tells how payments are moving in and out of the firm.

Debt

The cost that the company owes to others.

You can see if the company is progressing or losing money by looking at these records. This is helpful for investors and managers to make smart decisions about the future.

You can understand real financial statements in a simple way through this case study.

Read more: Why annual reports still matter for businesses?

Final Thoughts

In conclusion, financial statements provide key tools for grasping a company’s financial health. You can make better decisions for your business by reading balance sheets, income statements and cash flow statements. For instance, the balance sheet tells your firm’s assets and liabilities. On the other hand, the income statement shows profitability.

However, reading these statements should not be a single task. Reviewing these statements often will help you find trends and make good choices. Also, knowing these documents allows you to handle cash flow and plan for progress.

At Sterling Cooper, we know the value of financial literacy. Our team is available to help you navigate these core tools. They give insights to improve your decision-making. For more help or information, contact us today.

Struggling to understand your financial statements?

We help businesses interpret balance sheets, income statements, and cash flow for smarter decisions. Contact us today to get started!

FAQs

Reading a financial statement of a company helps you understand its financial health, including profits, losses, assets, liabilities, and cash flow. It allows business owners and investors to make informed decisions about the company's performance.

The main components include the balance sheet, income statement, and cash flow statement. Each provides insights into different aspects of the company’s financial position, such as assets, liabilities, revenue, expenses, and cash flow.

To read a financial statement of a company, start with the balance sheet to check assets and liabilities, then review the income statement for profits or losses. Finally, analyse the cash flow statement to understand how cash moves in and out of the business.

The balance sheet shows what a company owns (assets), what it owes (liabilities), and the value left for shareholders (equity). It gives you a snapshot of the company’s financial position at a specific point in time.

For investors, reading a financial statement of a company helps evaluate its financial stability, profitability, and potential for growth. It provides critical data to make investment decisions.

Recent Posts