Posted by:

Admin

Date:

June 8, 2026

Category:

blogs

What Is an HMRC Payment Plan? A Clear Guide for 2026

Struggling with a large tax bill? A HMRC payment plan could give you the space you need to manage your payments.

A HMRC payment plan is a formal agreement between you and HMRC. It allows you to pay your tax over several months instead of paying in one go. This can make large tax bills easier to manage.

The amount you pay each month depends on your financial situation. HMRC may ask about your income, spending, savings and other debts.

They want to make sure the payment plan is affordable for you. Many people use a payment plan for self assessment tax bills.

According to HMRC official data, taxpayers with debts of up to £30,000 may be able to set up a payment plan online without calling them directly.

Key Takeaways

- A HMRC payment plan (also called Time to Pay) lets you spread your tax bill into smaller monthly payments instead of paying in one lump sum.

- It is mainly used by self-employed people, landlords, and businesses who cannot pay their tax bill on time due to cash flow or financial pressure.

- HMRC usually allows payment plans for taxes like Self Assessment, VAT, PAYE, and Corporation Tax, depending on eligibility and debt level.

- Most payment plans are set for around 6 to 12 months, although longer arrangements may be approved in special cases.

- HMRC data shows that thousands of taxpayers use payment plans each year, and many arrangements are completed successfully when payments are made on time.

- A HMRC payment plan does not reduce your tax debt—you still pay the full amount, but over time in manageable instalments.

- Interest continues to apply while you are on a payment plan, so the longer the repayment period, the more interest you may pay.

- Setting up a plan early can help you avoid serious consequences such as penalties, debt collection, or legal action.

- Most applications require financial details like income, expenses, and bank information to check affordability.

- A payment plan works best when payments are realistic and strictly followed, as missed payments can lead to cancellation of the agreement.

Understanding HMRC Payment Plans

HMRC understands that financial problems can happen to anyone. Rising costs, slow business periods or sudden personal expenses can make tax payments more difficult. A payment plan gives taxpayers extra time to clear their debt in an easy way.

These plans are often called “Time to Pay” arrangements. They are designed to help people avoid serious actions like penalties, debt collection or legal action.

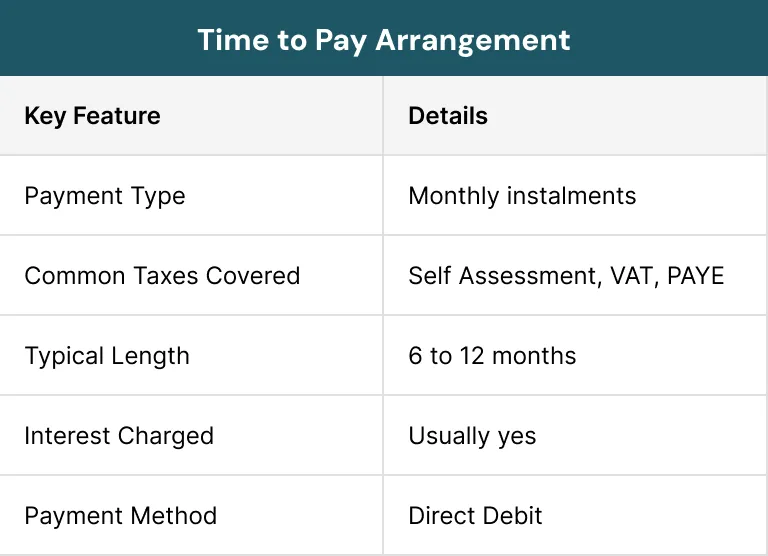

What Is the HMRC Time to Pay Arrangement?

A Time to Pay (TTP) arrangement is the official term for a formal payment plan negotiated directly with HMRC. It is designed for people and businesses that are struggling to pay taxes by the deadline.

Under this arrangement, you agree to make regular monthly payments. Most plans are between 6 and 12 months. Although longer plans may be allowed sometimes.

TTP does not remove the tax debt. You still need to pay the full owed amount. Interest may also continue until the balance is cleared completely.

Why Do People Need An HMRC Payment Plan?

Many people face financial problems in life at some point. A sudden drop in income, rising costs or unexpected bills can make it difficult to pay taxes on time. A payment plan can help to reduce this pressure.

Self-employed workers often face changes in income each month. Some months may be busy for them, while others may be quiet. This makes it harder to save enough money for tax deadlines.

Businesses may also struggle because of late customer payments or any economic problem. Instead of ignoring the debt, arranging a HMRC payment plan can help businesses to stay stable.

Common Reasons for Tax Debt

One common reason for tax debt is poor budgeting. Many people forget to save money for taxes. When the deadline arrives, the bill feels much larger than expected.

Unexpected life events can also cause problems. Illness, family emergencies or losing work can affect your finances.

Some businesses also face cash flow problems because customers pay late. Due to this, the company can face a shortage of money. In this case, a payment plan can help to manage these situations in a better way.

The Risks of Ignoring HMRC

Ignoring the letters or phone calls of HMRC can make the problem worse. Interest and penalties may continue to grow if no action is taken on time. This can increase the total amount you owe.

HMRC has strong powers to recover unpaid taxes. They may use debt collectors, take money from your bank account or start legal action against you. In serious cases, you could even face closure of business.

Pro Tip:

Contacting HMRC early is always the better option.

Risks of ignoring tax debt:

- Late payment penalties

- Daily interest charges

- Debt collection action

- Court action

- Damage to business cash flow

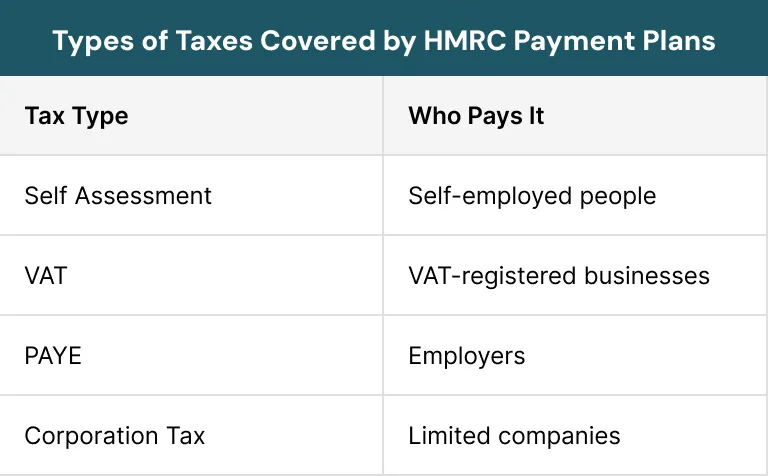

Which Types of Taxes Are Covered by HMRC Payment Plans?

A HMRC payment plan can be used for different types of tax debts. This includes self-assessment, VAT, PAYE and also Corporation Tax. Each tax type has different rules.

Many people use these plans for self-assessment because large yearly tax bills can be difficult to manage. Businesses also commonly use them for HMRC VAT payment plans and PAYE debts.

1. Self Assessment Tax Debts

Self-assessment is one of the main reasons people request a HMRC payment plan. Freelancers, landlords and self-employed workers often receive large tax bills after completing their returns.

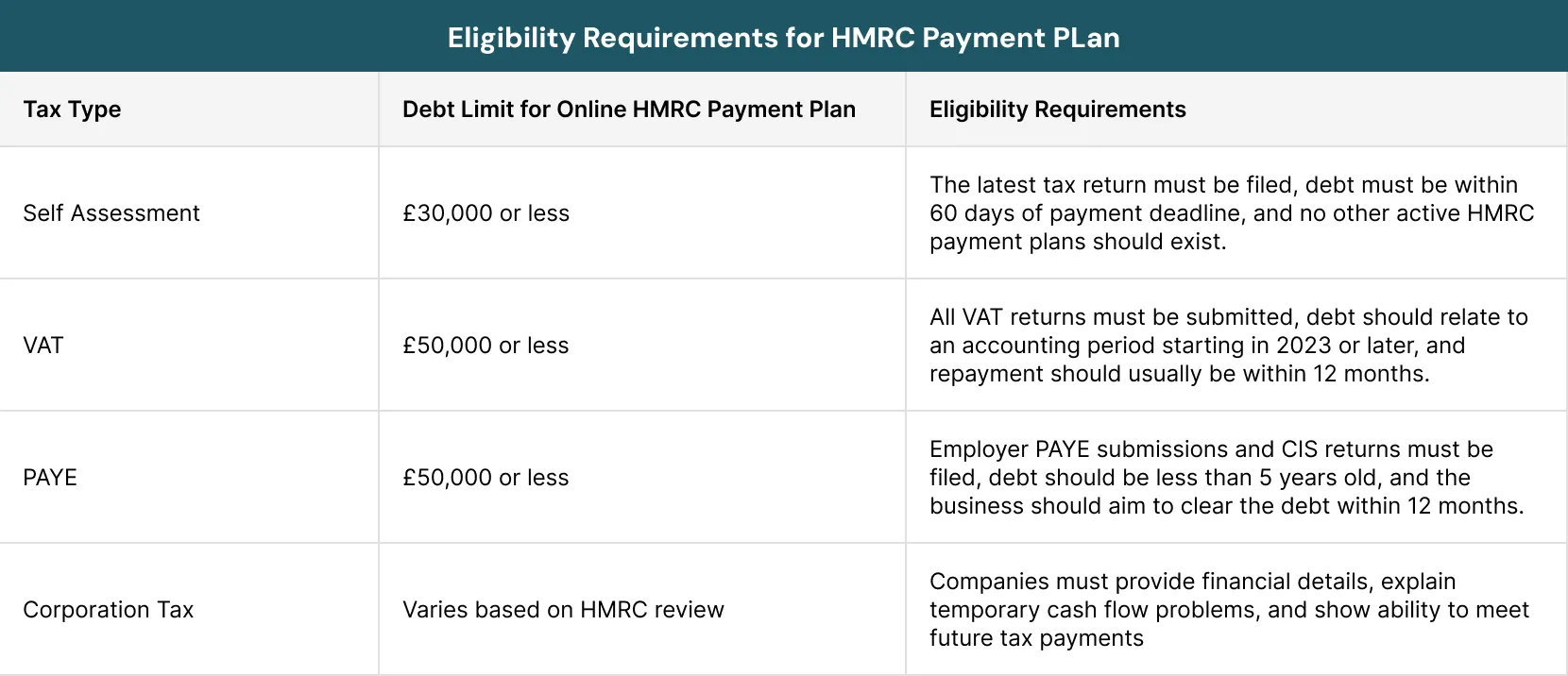

HMRC may allow online payment plans for Self Assessment debts. Usually, you must owe less than £30,000 and be within 60 days of the payment deadline.

2. VAT, PAYE and Corporation Tax Debts

Businesses can also apply for an HMRC VAT payment plan. VAT is treated seriously because companies collect it from customers on behalf of HMRC.

PAYE debts happen when employers cannot pay employee tax deductions on time. If the business remains cooperative, HMRC may still agree to a payment plan.

Payment plans for corporation tax are also possible for those companies that are facing short-term cash flow problems. Speaking to HMRC early can improve the chances of approval.

Read more: Using Losses to Reduce Your Corporation Tax Bill

Who Can Apply for an HMRC Payment Plan?

Not everyone applies directly for an HMRC payment plan. HMRC checks whether the taxpayer can easily afford the monthly payments or not. They also look at their previous payment history.

You usually need to file all outstanding tax returns before applying. HMRC wants to see that you are keeping your records up to date.

Did you know?

The earlier you contact HMRC, the better your chances of approval.

Eligibility Requirements

For many online applications, taxpayers must owe below a certain amount. Self Assessment payment plans usually require debts below £30,000.

When HMRC May Refuse a Payment Plan?

HMRC may refuse a payment plan if they believe the repayments are unrealistic. Offering payments that are too low can reduce the chances of approval.

Missing the tax returns or ignoring previous HMRC letters can also create problems. Repeatedly breaking earlier payment plans may also lead to refusal.

HMRC prefers those taxpayers who communicate openly about their situation.

How to Set Up a HMRC Payment Plan?

Setting up an HMRC payment plan is usually easy if you prepare properly. Some people can apply online, while others may need to call HMRC directly.

Before applying, you should gather all the important information. This includes tax reference numbers, bank details and also details about your income and spending.

1. Applying Online

Many taxpayers can apply for an HMRC payment plan online through the HMRC website. This is often a quicker method.

You will usually need:

- Your tax reference number

- UK bank account details

- Information about missed payments

Once approved, payments are taken on a monthly basis by Direct Debit. Online systems are available for Self Assessment, VAT, PAYE, and Corporation Tax debts.

2. Contacting HMRC by Phone

Some cases are more complicated and require speaking to HMRC directly. Phone calls allow you to explain your situation in more detail.

Before calling, think about how much you can afford each month. During the conversation, HMRC may ask detailed questions about your finances.

3. Information You Need Before Applying

Preparation is very important when you are requesting a HMRC payment plan. Having the right and accurate details can help to speed up the process.

These details include:

- Tax reference numbers

- Business details

- Monthly income

- Household expenses

- Savings information

How HMRC Decides to Approve Your Plan?

HMRC carefully reviews your financial situation before approving an HMRC payment plan. They want to know whether you can stick to the time to pay arrangement or not.

The main goal is to recover the tax debt while allowing you enough time to pay. HMRC usually prefers those plans that are affordable and easy to manage.

Good communication can help to improve your chances of success.

Income and Spending Checks

HMRC may ask questions about your monthly income and expenses. This can help them to understand how much you can afford to pay.

They may ask about:

- Rent or mortgage payments

- Utility bills

- Food costs

- Business expenses

- Existing debts

What are Direct Debit and Payment Terms?

Most HMRC payment plan agreements use Direct Debit payments. This allows HMRC to collect the money each month automatically.

Payment terms depend on your financial situation. Shorter plans usually mean higher monthly payments.

If your circumstances change, then HMRC may review your arrangement. If you receive extra income, they could ask for larger payments.

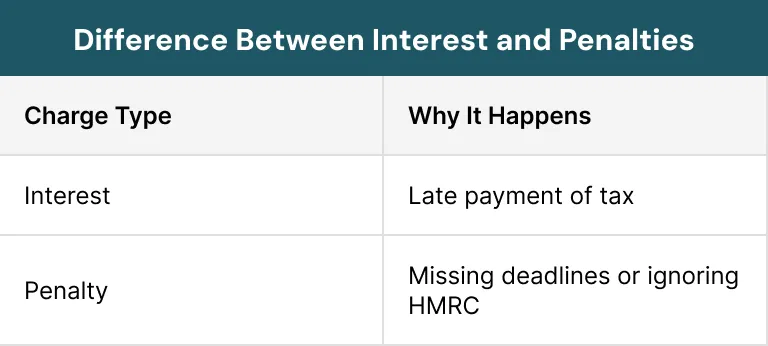

What are the Interest and Penalties on HMRC Payment Plans?

Many people think that interest will stop after setting up a HMRC payment plan. But this is not usually true. Interest normally continues until the debt is fully paid.

The good news is that payment plans can help to reduce penalties. Understanding the difference between interest and penalties can help you to avoid confusion.

How Interest Is Calculated?

HMRC usually calculates interest on the basis of the remaining balance. This means the longer the debt stays unpaid, the more interest builds up.

Making extra payments can help to lower the balance. Even small additional payments may help to reduce the total interest cost.

Read more: New HMRC Interest Rates Explained

What is the Difference Between Interest and Penalties?

When tax is paid late, then Interest applies automatically. It is based on the unpaid amount and the number of overdue days.

Penalties are different from interest because they are linked to behaviour. Missing the deadlines or ignoring HMRC letters may lead to penalties.

What are the Benefits of an HMRC Payment Plan?

An HMRC payment plan can reduce the financial pressure. It also helps taxpayers to manage their debts more easily. Instead of one large payment, you can pay on a monthly basis.

It can also improve cash flow for both individuals and businesses.

1. Better Cash Flow Management

Monthly instalments help to make budgeting easier. You can plan your spending in a better way without using all your savings at once.

Businesses can continue paying staff, suppliers and other bills. This can help to keep operations running smoothly.

2. Avoiding Enforcement Action

An HMRC payment plan can help to prevent serious recovery action. HMRC does not use debt collectors or any court action when payments are being made on time.

This can also protect your business reputation. Many people find peace of mind once an agreement is in place.

Pro Tip:

Taking early action is usually the best way to avoid bigger financial problems later.

What are the Common Mistakes to Avoid During a Payment Plan?

A HMRC payment plan works well when you stay organised and also communicate openly with HMRC.

Learning about common mistakes can help you to avoid unnecessary trouble.

What Happens If You Miss Payments?

Missing payments can cause serious issues. In case of missing the payments without any explanation, HMRC has the right to cancel the arrangement.

Interest will usually increase during this time. Penalties may also be added in some situations. If problems can happen, then the most important thing is to contact HMRC quickly.

1. HMRC Enforcement Actions

If a payment plan fails, HMRC may restart the debt recovery action. This could include debt collectors or legal action.

In serious cases, HMRC may:

- Take money from bank accounts

- Apply for bankruptcy

- Close a business

These actions are more likely when taxpayers ignore updates from HMRC.

2. Renegotiating Your Arrangement

If you cannot afford your payments anymore, then you should have to contact HMRC. Honest communication can help to prevent bigger issues.

If your problems are real, then HMRC may agree to adjust the payment plan for you.

What Are the Alternatives of HMRC Payment Plan?

A HMRC payment plan is not just a single option. Some people may find more suitable solutions.

It is important to compare all options. Different solutions have different costs and risks.

Professional advice can also help you to make better financial decisions in this process.

1. Loans and Overdrafts

Some people choose personal loans or business overdrafts to pay taxes on time. This may help to reduce the interest charges of HMRC.

However, bank loans may have higher interest rates compared to HMRC. It is important to compare both costs before borrowing money.

2. Advice from a Professional

An accountant or tax adviser can help you to understand the best option. They can also negotiate with HMRC on your behalf.

They can help you in certain areas including:

- Help to create realistic budgets

- Improve the payment proposals

- Reduce the stress during negotiations

Did you know?

Many people feel more confident when they are supported by a professional adviser.

Case Study: How a Small Business Used an HMRC Payment Plan?

James, a self-employed graphic designer from Manchester. After receiving a £12,400 Self Assessment tax bill in January 2025 he faced serious financial pressure.

In 2025, his income increased unexpectedly, but he had not saved enough money for taxes. Most of his earnings were used for business expenses.

At the same time, some clients delayed the payments, which disturbed the cash flow. He worried that missing the deadline would lead to penalties.

Instead of ignoring the situation, he quickly contacted HMRC to discuss the payment plan.

HMRC agreed to a 10-month Time to Pay arrangement after reviewing his income and monthly expenses. He made a small upfront payment of £1,400 and then agreed to pay around £1,120 each month.

Interest was still added to the remaining balance, but the payment plan helped him to avoid penalties and legal action.

Read more: The Ultimate Guide to Small Business Taxes

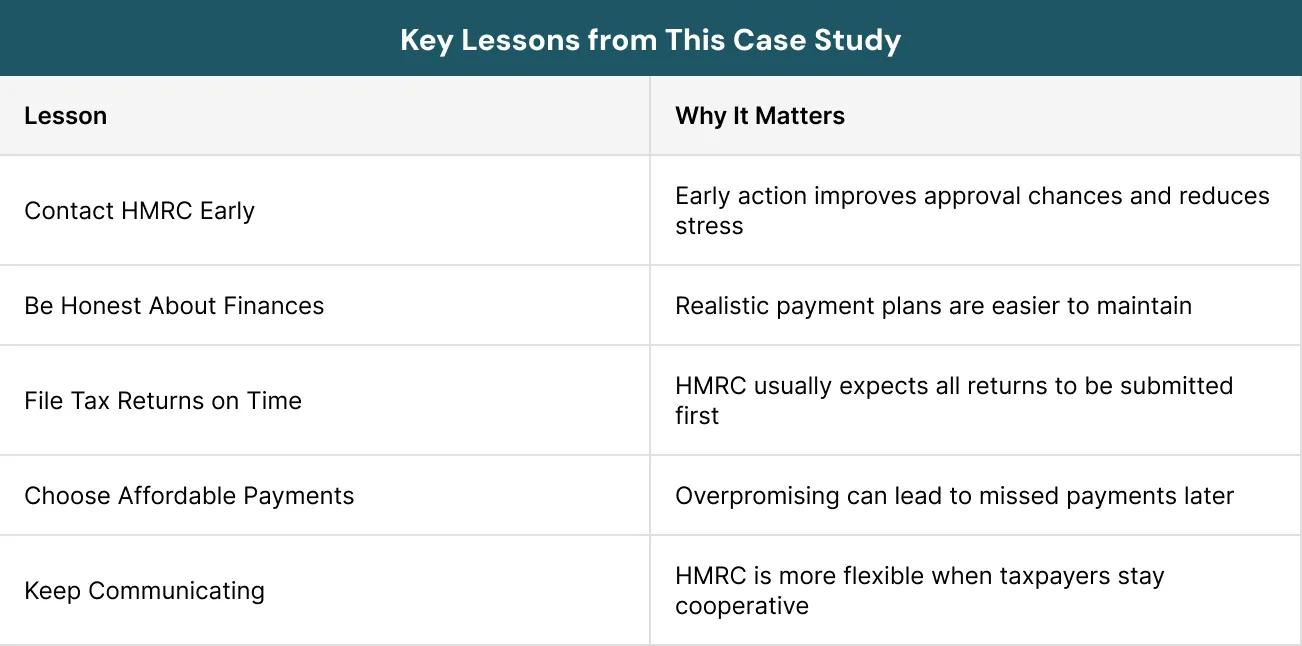

What Helped the Payment Plan Get Approved?

Several factors helped James’s to get approval including:

- He contacted HMRC early.

- His latest Self Assessment return had already been submitted.

- He provided honest financial details.

- He showed that his financial problems were temporary.

James stayed in contact with HMRC and made every payment on time. He successfully completed the arrangement without further action.

Conclusion

A HMRC payment plan can be a helpful solution for people and businesses who are struggling to pay tax bills on time. Instead of facing large payments, taxpayers can pay in monthly instalments.

The most important thing is to act early and communicate honestly with HMRC. Ignoring tax debt can lead to penalties, interest and also serious enforcement action.

A payment plan gives you the chance to regain control of your finances.

Whether you owe Self Assessment, VAT, PAYE or Corporation Tax, HMRC may be willing to support you. With good budgeting, realistic repayments and regular communication, payment plans can help you to clear your debt. At Sterling Cooper, we help you to set up a payment plan quickly. So you can manage your tax bill with more control. Feel free to contact us today.

Struggling with large tax bills? Or facing difficulty to manage the payment plans?

Our professional team is here to help you in this process. Look at our services for better understanding.

FAQs

A HMRC payment plan is an agreement that allows you to pay your tax debt in smaller monthly instalments instead of paying the full amount at once.

Self-employed individuals, landlords, limited companies and businesses can apply for a HMRC payment plan if they cannot afford to pay taxes on time.

The main HMRC Self Assessment payment plan helpline is 0300 200 3820. Different departments may have separate contact numbers for VAT, PAYE, and Corporation Tax queries. You can also visit HMRC Official Website for the latest contact details.

HMRC will always check whether it is possible to set up a payment plan under which you agree to make a monthly amount over an agreed period of 12 months or longer to settle the tax liability.

Yes, they will charge you interest on the outstanding tax balance.

Recent Posts