Posted by:

Admin

Date:

June 10, 2026

Category:

blogs

How To Avoid Capital Gains Tax In The UK?

Capital Gains Tax (CGT) is one of the most important taxes for investors, landlords, business owners and anyone selling valuable assets in the UK. Whether you are selling shares, cryptocurrency, property or a business, understanding how avoiding Capital Gains Tax works can save you thousands of pounds legally.

Many people only think about taxes after selling an asset. It is often too late to reduce the tax bill properly. With smart planning and the right methods, you can significantly reduce, and sometimes completely avoid, Capital Gains Tax in the UK.

Higher-rate taxpayers in the UK may now face Capital Gains Tax rates of up to 24% on qualifying gains. This increases the importance of effective tax planning for investors, property owners and business sellers.

In recent years, CGT has become a bigger issue because the annual tax free allowance has been reduced dramatically. The Annual Exempt Amount fell from £12,300 to just £3,000, meaning many more people now face larger tax bills when selling a property.

The good news is that UK tax law still offers many completely legal ways to invest to avoid capital gains. These include using ISAs and pensions, transferring assets to spouses, offsetting losses, timing disposals carefully and using special HMRC reliefs.

Key Takeaways

- Capital Gains Tax is charged on the profit made when selling valuable assets.

- The current annual CGT allowance is £3,000 per person.

- ISAs and pensions can help protect investments from Capital Gains Tax.

- Spouse transfers may help reduce overall tax liability.

- Capital losses can be offset against gains to lower taxable profits.

- Private Residence Relief may reduce or remove CGT on your main home.

- Careful timing of asset sales can help lower CGT rates.

- Business owners may benefit from reliefs such as BADR and Rollover Relief.

- Proper record keeping is essential for accurate CGT reporting.

- Early tax planning can help investors, landlords and business owners save thousands legally.

What Is Capital Gains Tax?

The Capital Gains Tax is a tax on the profit you make when selling or disposing of an asset that has increased in value. You only pay tax on the gain, not on the total sale amount.

For example, if you buy shares for £15,000 and later sell them for £40,000, your capital gain is £25,000. After deducting any allowances or reliefs, the remaining gain may be taxable.

CGT commonly applies to:

- Buy-to-let property

- Second homes

- Shares and Capital

- Cryptocurrency

- Business assets

Some assets are usually exempt including:

- Your main home (in many cases)

- ISAs

- Pension investments

- Personal cars

What are the Current Capital Gains Tax Rates in the UK?

The amount of avoiding Capital Gains Tax you pay depends on your income tax band and the type of asset you sell. In the UK, basic rate taxpayers generally pay 18% CGT, while higher and additional rate taxpayers usually pay 24% on qualifying gains.

Each individual also receives an annual tax-free CGT allowance of £3,000. This means you only pay Capital Gains Tax on gains above this threshold after applying for any available reliefs or exemptions.

Use Your Annual Capital Gains Tax Allowance

One of the easiest ways to avoid Capital Gains Tax is to use your annual CGT allowance. Every UK taxpayer receives a tax-free allowance each year but it operates on a “use it or lose it” basis. If unused, it usually cannot be carried forward, so careful planning can help reduce your tax liability.

Spread Asset Sales Across Multiple Tax Years

Instead of selling all investments or assets at once, many of the investors spread disposals across different tax years to avoid Capital Gains Tax.

For example:

- Sell part of an investment portfolio before 6 April

- Sell the remaining assets after 6 April

This strategy allows you to use two separate annual CGT allowances, helping to reduce your overall tax bill. Careful timing alone can save thousands in taxes.

Transfer Assets Between Spouses or Civil Partners

One of the most effective legal ways to avoid Capital Gains Tax is by transferring assets between spouses or civil partners. HMRC generally allows these transfers without causing an immediate CGT charge. This strategy offers several benefits:

- Use both CGT allowances.

- Benefit from lower tax rates.

- Reduce overall tax liability.

Careful planning between partners can help maximise tax savings on future asset sales.

Example

Imagine a higher rate taxpayer owns shares with significant gains. By transferring some of the shares to their spouse before selling, both partners can use their £3,000 CGT allowance, and the lower income partner may pay tax at a lower rate. This strategy is commonly used for:

- Buy-to-let properties

- Share portfolios

- Business assets

- Family Funds

Many couples reduce their overall tax liability each year through careful ownership planning.

How Do ISAs Help You Avoid Capital Gains Tax?

Individual savings accounts, or ISAs, are savings accounts that allow you to save up to £20,000 from capital gains tax per year. It is one of the best ways to avoid capital gains tax in the UK.

A Stocks and Shares ISA allows you to invest in shares, ETFs, funds and bonds while keeping all growth protected from CGT.

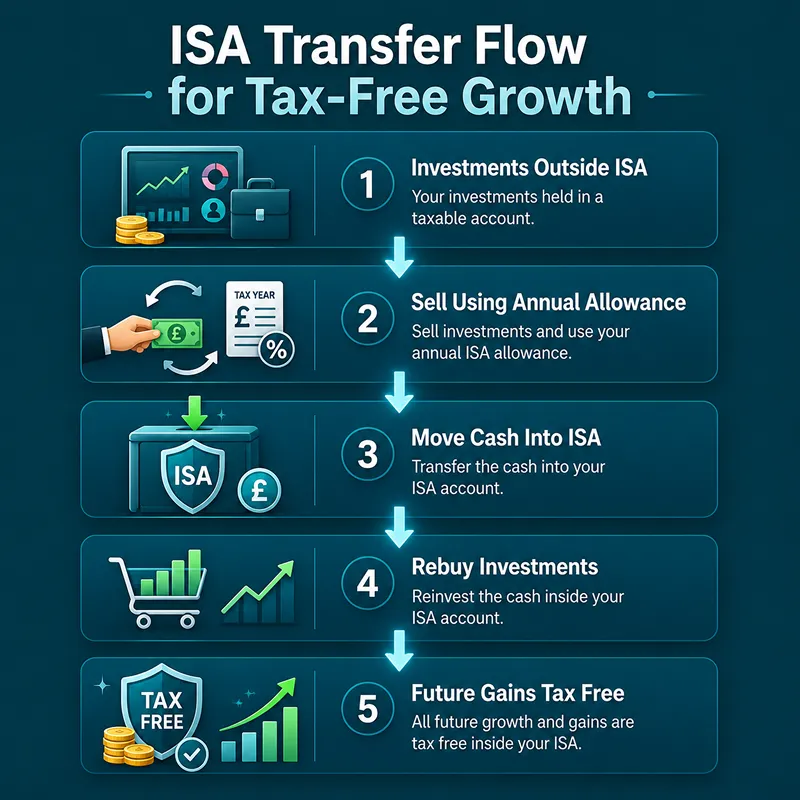

Many investors also use a Bed and ISA strategy. This involves selling investments held outside an ISA using the annual CGT allowance and then buying them back inside the ISA. Over time, this may help to move Assets into a tax-free environment.

How Pensions Help Reduce Capital Gains Tax

Pensions are one of the most tax-saving ways to grow Assets in the UK. Any Funds held within a pension are free from avoiding Capital Gains Tax allowing your money to grow without being taxed on gains. This may apply to:

- Systematic investment plan

- Workplace pensions

- Personal pensions

Pensions also offer additional benefits including income tax relief on Deposits and long-term tax-efficient growth. For the higher earners, the pension contributions may also help reduce taxable income and improve overall tax efficiency.

Helpful Hint

Pensions can provide both Capital Gains Tax benefits and income tax relief on contributions.

Claim Private Residence Relief

The Private Residence Relief (PRR) is one of the biggest CGT exemptions available. In many cases, you do not pay Capital Gains Tax when selling your main home.

Usually You Can Qualify If:

- The property was your main residence

- You did not mainly use it for business

- You did not rent large parts of it

- The property falls within HMRC rules

If the property qualifies fully, the entire gain may be exempt from CGT.

Offset Capital Losses Against Gains

Using losses correctly is one of the CGT methods that is most frequently overlooked. Gains from other assets can typically be used to offset a loss on the sale of an asset. Your taxable profit is greatly decreased as a result.

For Example

Increase in shares: £25,000, £10,000 was lost on the cryptocurrency investment. Before allowances the taxable gain is £15,000. Typically, unused losses can also be carried over to subsequent tax years. Maintaining accurate records is crucial for making loss claims.

Time Your Asset Sales Carefully

Timing plays a major role in CGT planning. Selling assets during lower income years can reduce the tax rate applied to gains.

Good Times To Sell May Include:

- Retirement

- Career breaks

- Maternity leave

- Business restructuring

Careful timing can reduce your CGT rate from 24% to 18%. Many investors and landlords plan disposals years in advance for this reason.

Use Business Asset Disposal Relief

The Enterprise Investment Scheme (EIS) and Seed Enterprise Investment Scheme (SEIS) give tax benefits to people who invest in small growing businesses.

Some possible benefits include:

- Income tax relief

- Capital Gains Tax deferral

- Tax-free profits in some cases

These investments can be higher on risk because smaller businesses may fail. Many investors use EIS and SEIS as part of their long term tax and money planning.

Consider Enterprise Investment Plans (EIS)

Enterprise Assets Plans (EIS) and Seed Enterprise Investment Plans (SEIS) offer valuable tax benefits for investors. These government-backed schemes are designed to encourage funding in smaller growing companies.

Potential benefits may include:

- Income tax relief

- Capital Gains Tax deferral

- Tax-free gains in certain cases

EIS investments are generally higher risk because they involve smaller businesses. Many experienced investors use these Plans as part of long-term tax and wealth planning strategies.

How to Use Rollover Relief

Rollover Relief lets business owners delay paying Capital Gains Tax when they sell certain business assets. The tax can be delayed if the money is used to buy new business assets. This can help businesses grow, buy property or replace equipment.

Incorporation Relief For Businesses And Landlords

Some of the Property owners and business owners move operations into limited companies. The Incorporation Relief may allow Capital Gains Tax to be deferred when transferring qualifying business assets into a company structure. This strategy can help the:

- Property investors

- Growing businesses

- Long term tax planning

However, incorporation also creates other tax considerations including:

- Corporation tax

- Dividend tax

- Stamp Duty Land Tax

- Additional compliance costs

Gift Assets to Charity

Donating the assets to charity can reduce or eliminate Capital Gains Tax (CGT). If you give qualifying assets to a registered charity, the CGT may not apply and Income Tax relief may also be available.

Common gifted assets include:

- Shares

- Property

- Land

- Artwork

How to Avoid Common Property Transfer Mistakes

Many people incorrectly assume that family property transfers are always tax-free. In reality, gifting the property can trigger avoidance of Capital Gains Tax (CGT) because HM Revenue and Customs often treats the transfer as a disposal at market value.

Property Transfers That May Trigger CGT

Certain property transfers can trigger avoided Capital Gains Tax, even if the property is not sold for profit.

- Gifting buy-to-let properties

- Adding co-owners

- Removing co-owners

- Transferring second homes

Why Record-Keeping Matters for Avoiding Capital Gains Tax

Good record-keeping is essential for effectively avoiding Capital Gains Tax planning(CGT). You should keep records of:

- Purchase pricesLegal fees

- Improvement costs

- Estate agent fees

- Transaction expenses

- Previous tax returns

Report Property Gains on Time

If you sell UK residential property and owe CGT, HM Revenue and Customs normally requires reporting and payment within 60 days of completion. Many landlords face penalties because they miss this deadline. Even if little or no tax is due, reporting obligations may still apply.

Should You Use a Limited Company?

Holding property or assets through a limited company can offer tax benefits such as corporation tax treatment and flexible profit extraction. However, most companies can also create additional costs, tax obligations and compliance requirements. The right structure depends on your income investment goals and long-term plans, so professional advice is often recommended.

Cryptocurrency And Capital Gains Tax

Cryptocurrency is also subject to Capital Gains Tax in the UK. HMRC treats crypto assets similarly to investments. Avoided capital gain tax may apply when:

- Selling cryptocurrency

- Swapping coins

- Using crypto to buy goods

- Gifting crypto assets

Many investors wrongly assume crypto profits are tax-free. Careful record keeping is essential because HMRC increasingly monitors digital asset transactions.

How Wealthy Investors avoid Capital Gains Tax

Investors rarely focus only on investment returns. They focus on after-tax returns. According to investor discussions and financial planning communities, some common plans include:

- Using ISAs regularly

- Using spouse allowances

- Holding assets longer

- Using tax-efficient accounts

Mistakes That Increase Capital Gains Tax

Many people accidentally increase their CGT bill through poor planning.

Common Mistakes Include:

- Selling assets in one tax year

- Ignoring spouse exemptions

- Missing loss claims

- Missing reporting deadlines

- Not using ISAs or pensions.

- Assuming family transfers are tax free

- Keeping poor records

When Should You Speak To A Tax Adviser?

Some CGT situations are straightforward but professional advice becomes important when dealing with:

- Property portfolios

- Business sales

- Trusts

- International assets

- Cryptocurrency

- Large investment gains

- Inheritance planning

A qualified tax adviser can help structure transactions legally and efficiently. In many cases, the tax savings achieved far exceed the adviser’s fee.

Final Thoughts

Capital Gains Tax can reduce a large part of your profits if you do not plan ahead. In many cases, UK tax rules provide several legal and effective ways to reduce or avoid capital gain tax. Careful planning before selling assets can help lower your overall tax liability and protect more of your wealth. Some of the most effective ways to avoid Capital Gains Tax include:

- Using annual CGT allowances

- Investing through ISAs and pensions

- Transferring assets to spouses

- Claiming Private Residence Relief

- Offsetting capital losses

- Timing asset sales carefully

- Keeping accurate records

- Seeking professional tax advice

As HMRC continues increasing compliance checks and CGT allowances remain lower. Tax-efficient planning is becoming more important for investors, landlords and business owners. At Sterling Cooper, we help individuals and businesses to avoid Capital Gains Tax through smart and compliant tax planning strategies. Contact us today to discuss the right solution for your situation.

Worried about paying too much Capital Gains Tax on your investment property or business sale?

We have helped individuals, investors and business owners reduce CGT through smart tax planning and compliant strategies. For Capital Gains Tax planning, reach out to us today to discuss the right solution for your situation and learn more about our professional tax planning services.

FAQs

You can reduce CGT legally through ISAs pensions annual allowances, spouse transfers and capital loss offsets. Early tax planning can significantly lower your tax bill.

Leaving the UK does not always remove CGT obligations because HMRC temporary non residence rules may still apply if you return.

The “Bed and ISA” strategy involves selling investments using your CGT allowance and rebuying them inside an ISA for future tax free growth.

Private Residence Relief spouse transfers annual allowances and careful sale timing can help reduce property related CGT.

The 6 year rule may allow some homeowners to keep Private Residence Relief after moving out of their property in certain situations.

Recent Posts