Posted by:

Admin

Date:

May 26, 2026

Category:

blogs

Year End Accounting Checklist for UK Businesses

Is your business ready for the financial year end or will last minute accounting tasks stress you out? A good year end accounting checklist helps UK businesses stay compliant, improve cash flow and prepare for smarter financial decisions.

The end of the financial year is very busy for businesses in the United Kingdom. Many teams are working hard to meet their targets. They are also working on budgets and planning for the year ahead. Finance teams ensure all the financial records are accurate and up to date. They have to do tasks like reconcile accounts and prepare financial statements. These tasks are important because they help in compliance, tax reporting and planning for the business’s future.

The process of year end accounting can be challenging for many businesses because they are missing invoices. There may be delayed approvals. They also have incorrect records and tight deadlines for filing. But if you have an organised year end accounting checklist, it can make the whole process a lot easier. It can improve accuracy and reduce the chance of making mistakes that will cost the business.

The UK has over 5 million registered limited companies as per 2025 data, all of which must file annual accounts.

When the year end comes around, the accounting process is not just about meeting the rules set by HMRC and Companies House. It also gives you an idea of cash flow, profitability and financial health of a company. If year end accounting is done properly, it helps you make decisions and you can start the new year with confidence.

Key Takeaways

- A structured year end accounting checklist helps UK businesses stay organised, avoid last minute stress and ensure full compliance with HMRC and Companies House requirements

- Completing an accounting year end checklist early, especially reconciliations, accruals and payroll reviews. It reduces errors and improves financial accuracy

- A complete year end accounts checklist UK includes bank reconciliation, accounts payable/receivable review, inventory checks, fixed asset updates and tax planning

- An end of financial year accounting checklist ensures all income, expenses and adjustments are correctly recorded before preparing statutory reports

- Accurate preparation of year end accounts supports better tax efficiency, audit readiness and improved business decision making

- Regular reconciliation and documentation throughout the year make closing accounting faster, smoother and less error prone

- Businesses that follow a disciplined year end process gain clearer financial visibility and stronger planning for the next accounting period

What Is Year End Accounting?

Year end accounting is the process of reviewing, reconciling, adjusting and finalising the financial records at the end of a company’s accounting year. The goal is to make sure all financial records are correct before preparing year end accounts and sending tax returns.

The accounting year is a 12 months period for most limited companies in the UK. At the end of the year, companies check income and expenses, assets and liabilities, payroll records, inventory and tax liabilities.

The process involves:

- Reconciling bank accounts

- Reviewing accounts payable and receivable

- Accruals and prepayments recording

- Depreciation calculation

- Financial statements preparation

- Reviewing tax liabilities

- HMRC and Companies House reports filing

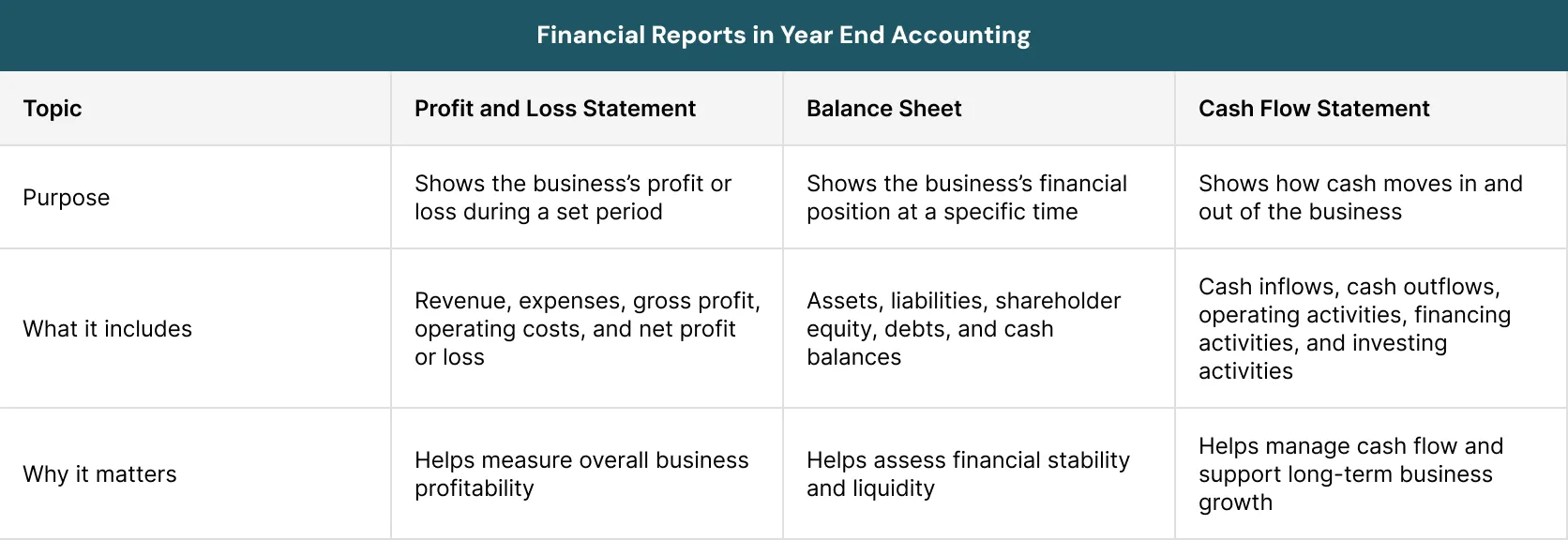

Once the process is complete, businesses can prepare accurate year end reports. These include the balance sheet, profit and loss statement and cash flow statement.

What Is the Importance of Year End Accounting in UK Businesses?

Many business owners think of year end accounting as a legal requirement but it is more than that. A good year end close helps businesses know their finances better. It also reduces risks and helps them plan for future growth. Year end accounting helps to give a picture of a business’s financial health.

1. Legal Compliance

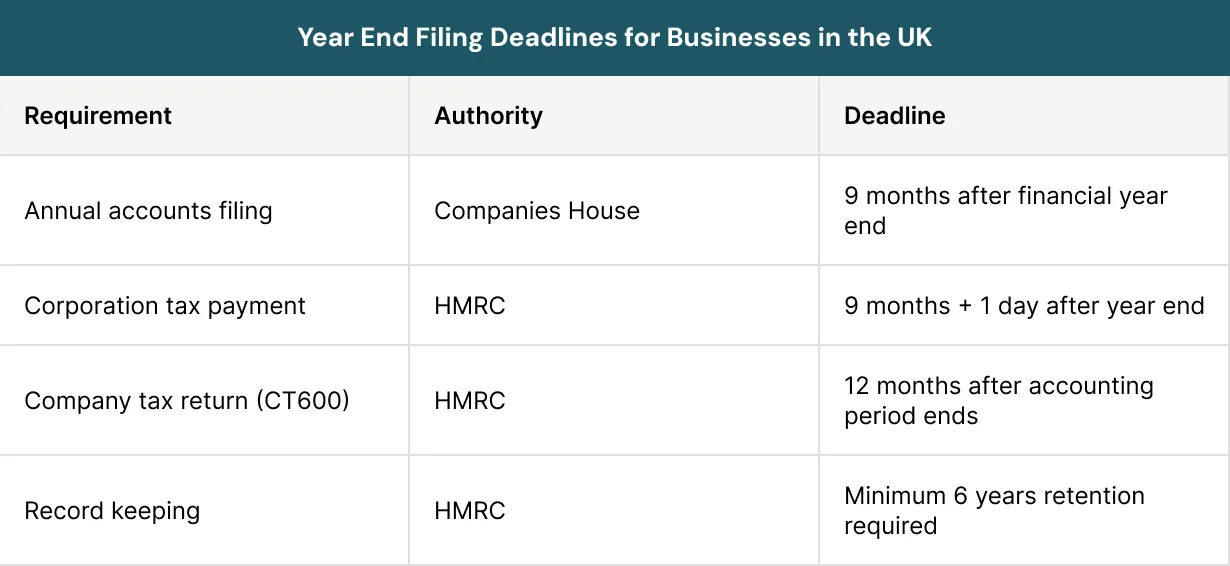

UK businesses must submit annual accounts and Corporation Tax returns before the set deadlines. There can be penalties, interest charges and other compliance issues if these deadlines are missed.

Companies House usually asks for annual accounts within nine months after the end of the financial year. HMRC requires Corporation Tax payments within nine months and one day.

Businesses can stay compliant and avoid unnecessary penalties by doing accurate year end accounting.

In the 2025, around 297,682 late filing penalties were issued by Companies House for overdue annual accounts.

2. Financial Accuracy

The year end close helps make sure all financial records are correct and complete. Checking accounts help businesses identify missing transactions. They also help find duplicate entries, wrong journal records, unrecorded liabilities and unauthorised spending.

Accurate records help businesses make decisions and improve their financial reporting.

Good financial reporting is the backbone of sound decision making. – Sir David Tweedie, former Chairman of the International Accounting Standards Board (UK accountant)

3. Tax Efficiency

A proper year end review can help businesses find ways to save tax. Businesses may lower their corporation tax through capital allowances, pension payments, bad debt relief, stock write downs and allowed business costs.

Tax savings can be improved by reviewing these areas before year end closing.

4. Better Business Planning

Year end reports provide valuable information about the performance of a business. Management teams can check on growth of sales, profits, cash flow, customers’ payment behaviour and escalation of business expenses.

This information helps you forecast your budget and make plans for the future.

Why Complete Year End Accounting Checklist is Required for UK Businesses?

A year end accounting checklist helps businesses close their books accurately. It also helps them stay compliant and reduces last minute pressure with accounting. Preparing early with a year end accounting checklist makes the accounting process more efficient. It is also less stressful with an accounting checklist.

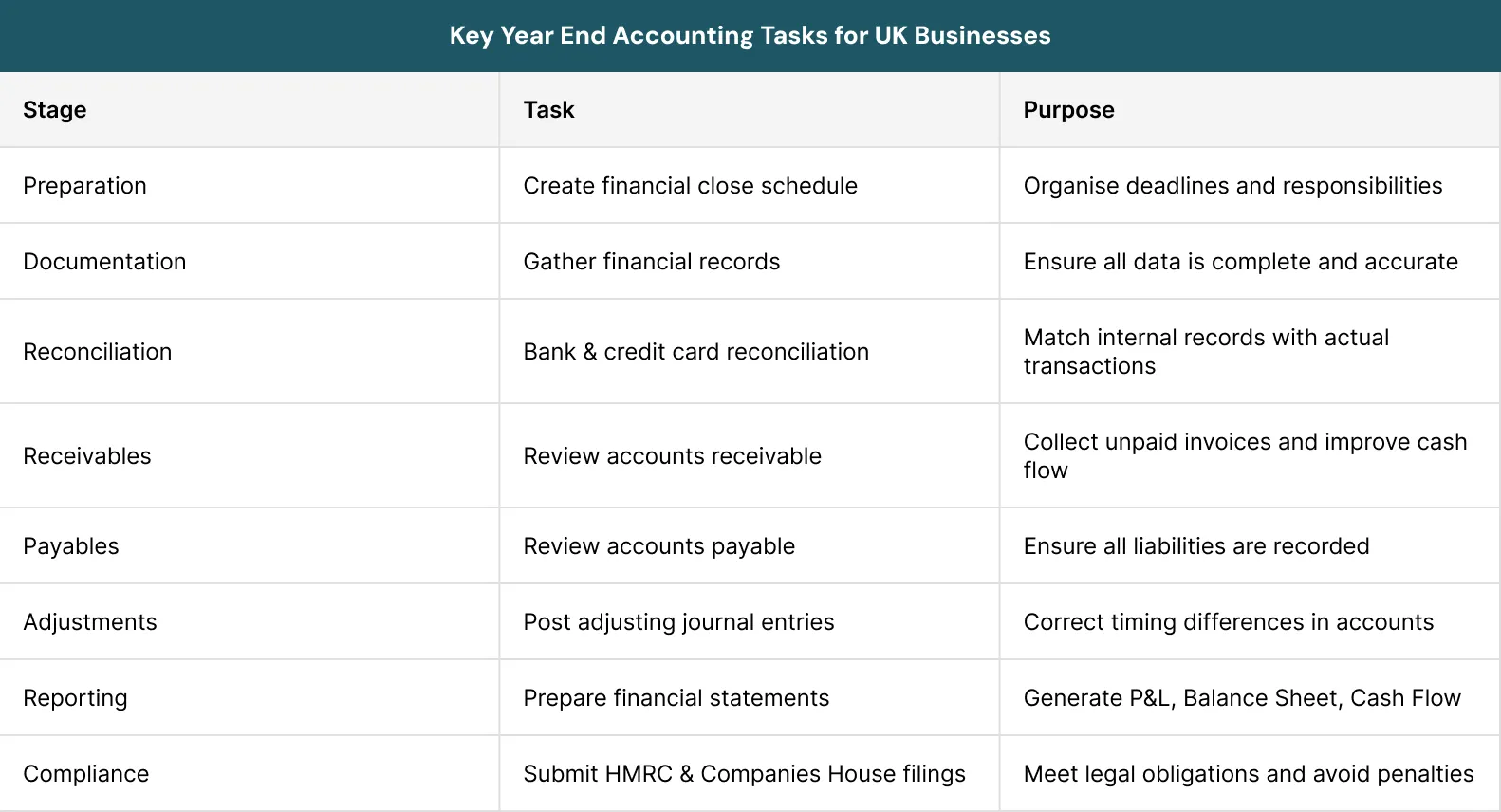

1. Preparing Early for a Smooth Year End Close

Successful year end accounting with a year end accounting checklist starts well before the closing date.

Businesses that keep records organised during the year often have a smoother and less stressful year end process.

Important steps include:

- Monthly reconciliations

- Tracking expenses regularly

- Using cloud accounting software

- Keeping digital records organised

- Reviewing unpaid invoices during the year

- Setting internal deadlines

Creating a financial close schedule as part of a year end accounting checklist can also help teams manage tasks and avoid last minute problems.

2. Create a Financial Close Schedule

A well planned and easy to follow schedule really helps businesses keep track of important dates and avoid last minute stress. This schedule includes:

- Important reporting deadlines

- Filing deadlines of HMRC and Companies House

- Internal review dates

- Assigned responsibilities

- Reconciliation timelines

When it is time to complete the year end accounting, it becomes a lot easier if you break it down into smaller tasks.

3. Gather and Organise Financial Documents

Businesses following a year end accounting checklist should have all of their financial records and supporting documents in one place before starting reconciliation. Important records include:

- Bank statements

- Credit card statements

- Payroll reports

- Supplier invoices

- Expense receipts

- Loan documents

- Tax records

- Sales reports

- Inventory reports

The digital copies of invoices should be kept safe and provided when needed. This is important for audit readiness and compliance. Businesses are required to keep records for at least six years as per HMRC.

What Are the Common Challenges During Year End Accounting?

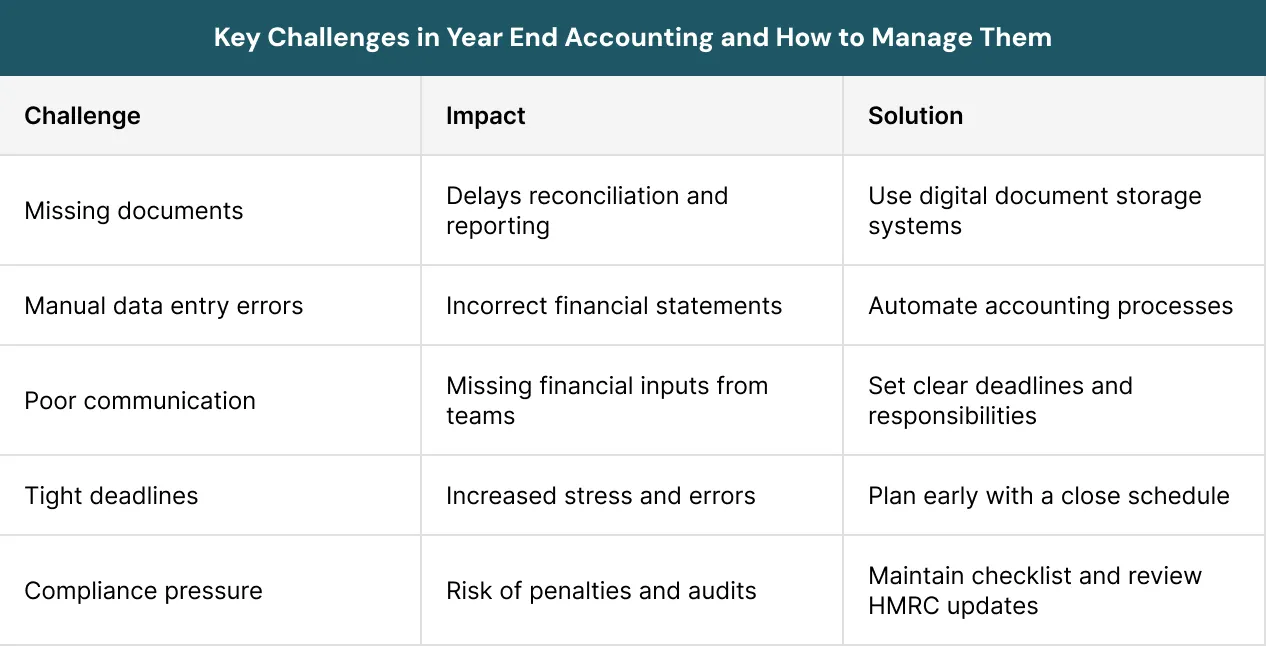

Even organised businesses can struggle during year end close. Understanding common problems helps companies prepare more effectively.

1. Manual Processes and Human Error

Businesses that still use spreadsheets and enter data by hand often have problems with entries, mistakes in calculations, missing transactions and taking a long time to reconcile things.

Small mistakes can cause problems when you are getting ready to make your financial statements and tax returns.

2. Missing Documentation

Finance teams often waste time looking for receipts, invoices from suppliers, expense claims and payroll details. This is usually because they do not have a system for managing documents. This slows down the closing accounting process and increases compliance risks.

3. Tight Deadlines

Year end accounting usually happens along with month end reports, tax work and other operational tasks. This can make it tough for finance teams to complete all the reconciliations and reviews on time.

4. Poor Communication Between Departments

Year end accounting requires input from HR, payroll teams, operations, procurement and department managers. Delays in receiving information can slow down the entire close process.

5. High Transaction Volumes

Businesses may handle thousands of transactions during the year. Checking every invoice, payment and expense can take a lot of time and attention.

6. Audit and Compliance Pressure

Businesses are required to keep their records organised and audit ready. They also meet the deadlines set by HMRC and Companies House.

Quick Tip:

Keeping digital receipts in real time can eliminate most year end document chasing.

4. Reconcile Bank Accounts and Credit Cards

A big part of any year end accounting checklist is bank reconciliation. Businesses should compare:

- Bank statements

- Credit card records

- Accounting software balances

- General ledger transactions

The goal is to make sure that every transaction recorded internally matches actual financial activity. Some of the common issues are incorrect amounts, duplicate entries, unauthorised transactions, missing payments and timing differences.

You Should Know:

Even small mismatches in bank reconciliation can signal fraud or hidden expenses.

You need to investigate any mistakes and fix them before finishing up your accounts. If you check your accounts regularly, it will make the year end process a lot easier.

5. Review Accounts Receivable

The money that customers have not paid yet is called accounts receivable. You must check the invoices that are still unpaid, the amounts that are overdue, payment history of a customer, aged debtors report and potential bad debts as part of year end accounting checklist.

If you collect unpaid invoices before the year ends, you will have improved cash flow and financial reports will be more accurate. If you think some payments cannot be received, you need to record them as bad debts. This is all part of managing accounts receivable.

6. Review Accounts Payable

Accounts payable is the money that you have not paid yet to vendors and suppliers. Finance teams following a year end accounting checklist must:

- Verify supplier invoices

- Review unpaid bills

- Record accrued expenses

- Check for duplicate payments

- Confirm liabilities are complete

You have to record all the expenses for the accounting period even if you do not have the invoices yet. The accounts payable review is very important for businesses to avoid understating liabilities or overstating profits.

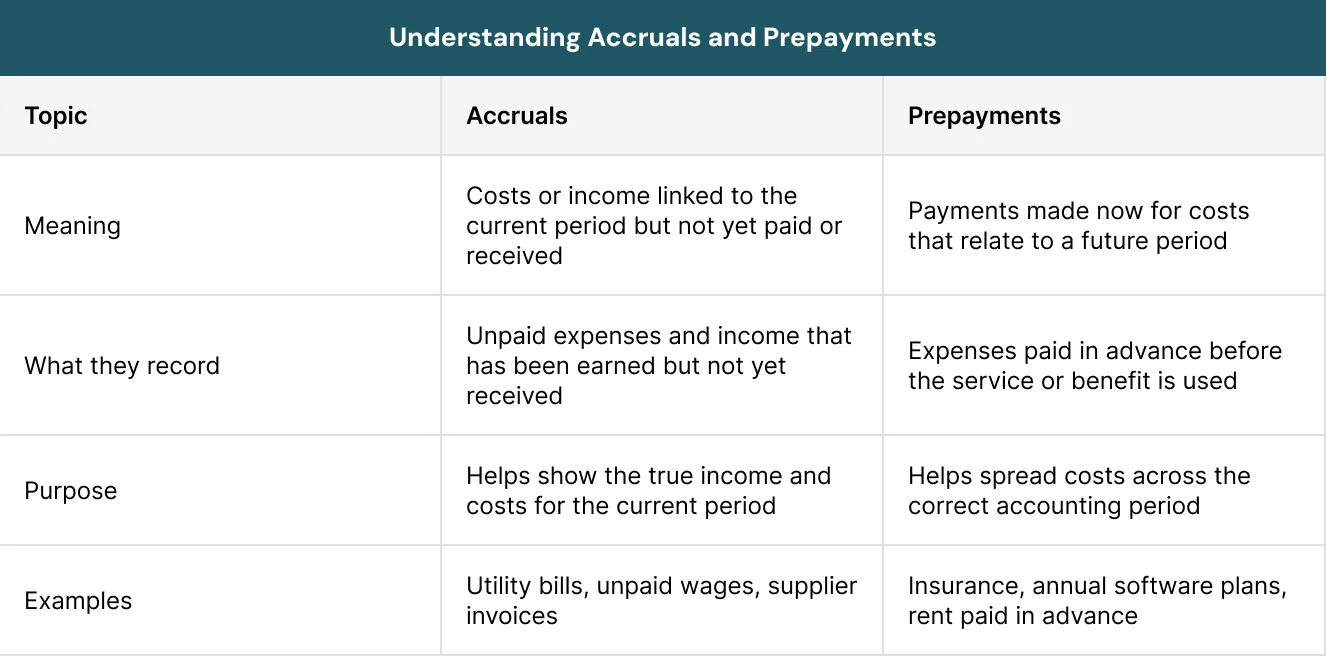

7. Record Accruals and Prepayments

Accruals and prepayments are an important part of a year end accounting checklist for making sure that you have recorded income and expenses in the right time frame.

8. Conduct Inventory Reviews

Businesses holding stock should complete a physical inventory count as part of their year end accounting checklist before closing the books. The process should include:

- Counting physical stock

- Identifying damaged inventory

- Reviewing obsolete stock

- Comparing stock records with accounting records

The cost of goods sold (COGS), gross profit and tax calculations are directly affected by inventory. You should identify the mistakes in inventory, if any and make the necessary changes.

The valuation methods of inventory should remain consistent throughout accounting periods.

9. Review Fixed Assets and Depreciation

Vehicles, equipment, computers, furniture and machinery that a business owns are called fixed assets. A year end accounting checklist should include reviewing the list of fixed assets and make sure:

- New purchases are recorded correctly

- Disposals are removed

- Depreciation calculations are accurate

Most companies use the straight line depreciation method. This method spreads the cost of assets evenly over the years that the asset is expected to be useful, which is the useful life of the asset. Depreciation adjustments affect:

- Profitability

- Balance sheet values

- Corporation Tax calculations

Businesses should also check their eligibility to claim capital allowances and the Annual Investment Allowance (AIA).

10. Review Payroll and Employee Records

Payroll is one of the most regulated areas in a year end accounting checklist. Businesses should review:

- PAYE records

- National Insurance contributions

- Pension contributions

- Bonuses and commissions

- Holiday accruals

- Employee benefits

Payroll reports should match accounting records, HMRC RTI submissions and payroll journals. Any discrepancies should be corrected before finalising year end accounts.

Important Insight:

Payroll errors are one of the most common triggers for HMRC investigations in the UK.

11. Categorise and Review Business Expenses

A year end accounting checklist should include reviewing business expenses carefully to ensure accurate categorisation, consistent treatment and HMRC compliance. Finance teams should review:

- Travel costs

- Office expenses

- Training costs

- Professional fees

- Home office expenses

- Client entertainment

Incorrect expense coding can distort profitability and increase tax risks.

12. Post Adjusting Journal Entries

A year end accounting checklist should include adjusting journal entries to ensure financial statements accurately reflect the company’s financial position. Common year end adjustments include:

- Accrued expenses

- Prepaid expenses

- Depreciation

- Inventory adjustments

- Payroll liabilities

- Bad debt write offs

These entries help make sure that your income and expenses are written down in the right time period. You need to make journal entries so that your financial reports are accurate and ready for an audit.

13. Prepare Financial Statements

Once reconciliations and adjustments are complete, businesses can prepare year end accounts and financial reports.

14. Conduct Financial Analysis

A year end accounting checklist also provides an opportunity to review business performance in detail. Businesses should compare:

- Current and previous year performance

- Revenue trends

- Profit margins

- Expense growth

- Cash flow changes

- Debt levels

Financial analysis is important for businesses and helps them identify operational inefficiencies. They can identify rising costs, weak cash flows and late customer payments.

Financial analysis gives businesses these insights so they can plan effectively for the next financial year.

15. Carry Out Tax Planning

A year end accounting checklist should include reviewing the tax position carefully before finalising accounts. There are several ways businesses can reduce tax liabilities. These things include:

- Bringing forward allowable expenses

- Increasing pension contributions

- Claiming capital allowances

- Writing off obsolete inventory

- Reviewing bad debts

- Purchasing qualifying assets

The eligibility of businesses should also be checked for:

- Annual Investment Allowance (AIA)

- Research and Development relief

- Other available deductions

Proper tax planning is essential for companies to reduce their Corporation Tax liabilities while following the rules set by HMRC.

16. Backup and Secure Financial Records

Once the year end accounting checklist is complete, businesses should securely store all financial records.

Important records include:

- Invoices

- Receipts

- Payroll reports

- Tax returns

- Financial statements

- Supplier agreements

- Bank statements

Cloud backups help:

- Protect against data loss

- Improve accessibility

- Support audit readiness

- Enhance cybersecurity

Having recordkeeping practices is a good idea because it makes future audits and financial reviews much easier to do.

Case Study

A UK telecom company called Lycamobile had financial troubles. They were unable to get their accounts approved because of tax and VAT problems. This led to an argument with HMRC about £51 million in VAT. Their year end accounts and financial statements were delayed. Auditors were worried about their records being accurate.

The problem showed how not having clear yearly accounts can cause compliance issues. These issues include tax investigations and damage to a company’s reputation.

Conclusion

Year end accounting is crucial for all UK businesses, no matter how big or small they are. It is not just about closing your accounts or meeting HMRC and Companies House deadlines; it is about getting a clear and correct picture of your business finances.

If you do year end bookkeeping properly, it can help keep your business compliant, reduce penalties, increase tax efficiency and help you make smarter decisions for the next year. When it comes to tasks such as bank reconciliation, payroll, inventory and accruals, each one is crucial for keeping your records accurate and complete.

The best businesses do not leave year end accounting until the last minute. They keep records organised during the year, use clear checklists and work with digital accounting tools. This makes the closing accounting process easier and reduces stress during the closing period.

Finally, a seamless year end close provides you with not only compliant year end accounts, but clarity, confidence and a solid base for future growth.

Sterling Cooper understands how stressful year end accounting can be for UK businesses, especially when deadlines, reconciliations and compliance requirements all come together at once. Contact us for expert support to ensure accurate, compliant and stress free financial close.

Struggling to manage year end accounting deadlines and compliance stress?

Sterling Cooper helps UK businesses streamline bookkeeping, reconciliations and year end reporting with expert accounting support. Contact us today to simplify your year end accounts.

FAQs

To prepare year end accounts, businesses must reconcile bank accounts, review income and expenses, adjust accruals and prepayments and finalise payroll and tax records.

They then prepare financial statements like the P&L, balance sheet and cash flow statement for HMRC and Companies House filing.

The 7 pillars of accounting refer to key principles: prudence, consistency, accruals, going concern, materiality, relevance and reliability. These ensure financial statements are accurate, consistent and useful for decision making.

The UK follows accounting standards known as UK GAAP (Generally Accepted Accounting Practice), mainly FRS 102 and FRS 105 for small entities. Some businesses may also use IFRS if they are listed or internationally active.

UK businesses mainly use accrual accounting, where income and expenses are recorded when earned or incurred, not when cash is received or paid. Smaller businesses may sometimes use cash accounting for simpler tax reporting.

The four main types are financial accounting, management accounting, cost accounting and tax accounting.

Each focuses on reporting, internal decision making, cost control and tax compliance respectively.

Recent Posts