Posted by:

Admin

Date:

March 19, 2026

Category:

blogs

Step-by-Step Guide to Managing Small Business Accounts

Is it hard to monitor your small business’s money?

Many small business owners feel exhausted by money coming in, going out and paying taxes. According to Forbes, 99.05% of UK businesses are small to medium sized enterprises.

Accounting of small business helps you save time, cut errors and grow your business. Keeping your accounts in order helps you see your money clearly and keep cash flow steady.

The benefits of small business accounting do more than maintain records; they help you make better business growth decisions.

In this blog, you will find out:

- How to start and manage your business accounts

- The difference between bookkeeping and accounting

- How to track costs, bills and wages

- How to choose the right tools

- How to manage VAT, taxes and cash flow

What Is Small Business Accounting and Why Is It Needed?

Accounting for a small business means keeping track of your money. It tracks your money coming in, going out and your profit or loss.

It also shows what you own, what you owe and your share of the business. What you own is called assets and what you need to pay is called liabilities.

A good accounting of small business provides benefits, including helping you plan budgets, track cash flow and see how your business is doing. This helps you pay tax easily and find ways to grow.

How to Start Managing a Small Business Account?

To manage your small business account, you must keep your personal and business money apart. It is a good practice to open a separate bank account for your business.

Limited companies must have one by law. On the other hand, it’s not necessary for self-employed workers to open another account by law.

If you keep your money separate from your personal finances, this approach has many benefits. It helps you track spending, income and taxes easily.

It’s a smart move to open a savings account to manage your taxes. This prevents you from spending money needed for Income Tax, Corporation Tax or VAT.

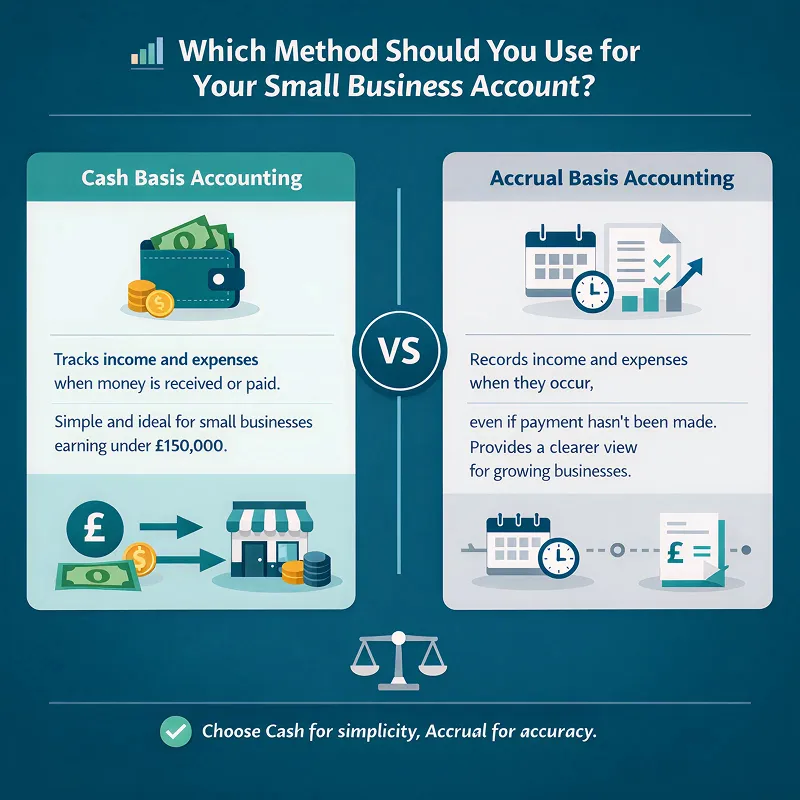

Which Method Should You Use for Your Small Business Account?

You can utilise two accounting techniques. Pick one of these:

Cash Basis Accounting

Cash-basis accounting tracks money when it comes in or goes out. It is simple and works well for small businesses earning under £150,000.

Accrual Basis Accounting

Accrual accounting records income and costs when they happen, even if money hasn’t moved. With the help of this, you can get a clearer view of bigger or growing businesses.

The correct method helps you track money, see profit and control taxes; the key benefits of small business accounting.

Learn more: Cash-Basis vs. Accrual Basis Accounting

Checking Profits and Turnover

Profit is the money left after payment of costs. On the other hand, turnover is all the cash your business gets. Look at the following points:

- Is your profit going up or down

- Which clients or products make the most money

- Are you spending too much

Tracking profit and turnover helps you plan taxes, pay yourself and grow your business.

Which Bookkeeping System Should You Use?

Bookkeeping means tracking money going in and out each day. It covers:

- Bills for sales and purchases

- Employee pay

- Bank records

- Receipts and bills

You can use spreadsheets at first, but cloud software like Xero, QuickBooks or Sage is simple and more reliable. These tools track money automatically, sort payments and make reports. This is another benefit of small business accounting.

Learn more related to bookkeeping system: 5 Ways Cloud Accounting Saves You Time and Money

Understanding Financial Statements

Financial statements tell you how your business is working. You can match and see the differences and similarities from one month to another. You will see what costs more or earns less. This way, you can make your business successful and make better decisions. The key types are:

Balance Sheet

A balance sheet tells you your assets, which means what you own. It also shows your liabilities, which means what you owe. Furthermore, it shows your net worth.

Profit and Loss Statement

It shows money earned, money spent and profit or loss.

Cash Flow Statement

It shows money coming in and going out each month. This helps you plan ahead and make better decisions.

Hiring a Professional for Bookkeeping

If you use bookkeeping software, it can do most tasks for you. But it’s necessary to update it often. It’s important to update your bookkeeping so that mistakes can’t happen.

Hiring a bookkeeper or accountant will help you in reducing stress and fix mistakes. Even getting occasional assistance from a professional can help you:

- Check and file tax returns correctly

- Follow VAT rules

- Plan your finances

- Keep your accounts in order

You don’t need a full-time accountant. Part-time or freelance help is often enough.

Which Costs Can You Claim for Your Small Business Account?

You can save your money and reduce your taxes by tracking your expenses. You can claim these common expenses:

- Contractors, freelancers and staff pay

- Rent, bills and office stock

- Travel and transport costs for business

- Staff coaching and perks

- Entertainment (£150 per employee each year; not for self employed workers)

You cannot claim penalties, political donations or hobby expenses. If you maintain good records, you can prove claims to HMRC.

How to Establish Invoices for Your Small Business Account?

Invoices are needed for timely payments and clear records.

Each bill should have:

- A unique ID number and date

- Bank details and procedure to pay

- List of expenses, total amount and VAT

- What you sold or the service you offer

- Name, address and email of client

Online billing software has many benefits. It can send reminders to clients if they forget to pay. This helps improve cash flow.

Payment Terms Used for Small Business Accounts

Payment terms teach customers when and how to pay. Common choices are:

Payment terms teach customers when and how to pay. Common choices are:If you are late in paying, you can prepare for it with payment plans or small fees. This way, you can keep your cash flow safe.

Handling Employees in Your Small Business

If you have staff, salaries must be accurate and on time. It covers:

- Staff pay

- Tax and National Insurance

- Staff benefits

Cloud accounting software can find out deductions automatically. It makes payroll easier by reminding you of deadlines.

Calculation of Tax and VAT for Your Business

To keep your business legal and get rid of penalties, you must do your taxes and VAT accurately. It’s your business type that decides how you pay:

- Sole traders pay income tax using self assessment

- Limited companies have to pay tax on their yields

You must register for VAT if your yearly income is over £85,000. You can select a VAT scheme:

With an accountant’s help, you can meet deadlines and claim all allowed deductions.

Calculate VAT for your business using the work out your flat rate guide.

Choosing the Right VAT Scheme

There are different ways to manage VAT. Select one of the following according to your business:

Standard

Big businesses pay VAT every three months and get back VAT on their purchase.

Flat Rate

Small businesses under £150,000 pay fixed charges and reclaim large purchases.

Annual Accounting

Send returns once a year, pay every three months.

Cash Accounting

Pay VAT only after the payment of customers.

With the help of the right scheme, you can avoid mistakes and save money.

Aid of Accounting Software for Your Small Business

Software makes managing accounts faster and simpler. It helps by:

- Automatically recording bank dealings

- Showing cash flow in real time

- Controlling payroll and VAT

- Making financial reports easier

For mobile devices, popular softwares are used, including Xero, QuickBooks, Sage. This is another benefit of small business accounting.

How to Manage Your Cash Flow?

Cash flow is the amount your business gets and spends. These are the ways to control your cash flow:

- Check the money often coming in and going out

- Use tools to get accurate cash flow reports

- Plan future money coming in and going out

- Reduce spending on things you don’t need

If your cash flow is positive, your business can pay bills, staff salaries and taxes on time.

How to Be Organised With Your Small Business Accounts?

You can keep your account free of stress with the help of staying organised. The key steps include:

- Combine all receipts, bills and bank papers and keep them together

- Use online accounting software

- Make monthly reports to watch Key Performance Indicators (KPIs) and growth

- Keep your accounts up to date often

Make clear objectives and budgets to see chances or risks early.

What Are KPIs and Why Watch Them?

You can imagine KPIs like simple numbers that help in viewing how your business is doing. For example these numbers include:

- Monthly money coming in and going out

- How many new clients do you get

- Profit rate

- How much money do you keep from sales

You can diagnose issues, see opportunities and examine growth if you monitor KPIs.

Hiring an Accountant for Your Small Business

It is not necessary to hire an accountant but they can benefit you in many ways. If you choose to hire an accountant, this can benefit you in the following ways:

- Save time and avoid mistakes

- Help plan and file taxes

- Make sure you follow HMRC and companies house regulations

- Make cash flow and reports better

If it is expensive for you to hire a full-time accountant, freelancers or outside services can help you.

Insignia Technologies Case Study: How Outsourcing Improved Financial Management

Insignia Technologies developed quickly but found it difficult to manage its money. To track money and make good business choices, they needed a simple system. Check out this example.

The Client

Insignia Technologies had rapid growth but its accounting got slower. They needed a system to look at money clearly and make good decisions.

The Challenge

Even with correct accountants, Insignia had trouble getting the information it needed. They wanted a procedure to keep finances simple, cut costs and show investors they were strong.

The Solution

Approved Accounting provided them with a complete outside finance team to track all their accounting. They helped Insignia in the following way:

- Manage cash flow

- Streamline accounts

- Save time and cut costs

- Get real time insights

Why It Worked

Insignia got professional help without hiring a full team by outsourcing. It worked in the following ways:

- A system that grows with a business

- Investor ready accounts

- Simple financial reports

- Costs under control

This tells us how the benefits of small business accounting help businesses develop with confidence.

Final Words

Handling your small business money can be easy. First, establish a separate business account, select a simple method and record your expenses daily.

Utilise accounting software to make bills, payroll and VAT simple. It is very beneficial to save time and avoid mistakes.

Hiring an accountant or a bookkeeper will give you additional help. If you can’t afford them, part-time or freelance help is also beneficial.

Good accounting of a small business helps you pick smart options, keep cash flow steady and grow confidently.

At Sterling Cooper, we know how important organised accounts are for small businesses. Contact us today to see how we can help you control your business money easily.

Struggling to keep your small business accounts in order?

We have helped hundreds of UK businesses simplify bookkeeping and accounting. Our team can manage your finances, improve cash flow and reduce errors. Contact us today to get started.

FAQs

Small company bookkeeping is the process of recording and organising all financial transactions in a small business. It includes tracking income, expenses, invoices and payroll. Good bookkeeping helps business owners monitor cash flow, stay tax-compliant and make better decisions for growth.

To do accounting in a small business, you need to track all income and expenses, reconcile bank accounts and prepare financial statements like profit and loss and balance sheets. Using accounting software like Xero or QuickBooks can make this easier. You may also hire an accountant for guidance and tax compliance.

Steps to managing your business accounting:

- Record your transactions

- Document your receipts and invoices

- Regularly conduct a cash flow analysis

- Oversee payroll

- Make projections

- Understand professional tax requirements

- Manage profit and loss

- Review inventory

There are two main methods:

- Cash basis accounting

- Accrual accounting

Cash basis means you record money when it changes hands, while accrual accounting means you track income and expenses when they're earned or incurred, even if cash hasn't moved yet.

Business structures such as 'sole trader' are not required to have a separate bank account, but it could be a good idea to consider getting one.

Recent Posts