Posted by:

Admin

Date:

February 24, 2026

Category:

blogs

A Complete Guide to Wealth Tax in the UK

Wealth tax has become one of the most debated topics in UK fiscal and social policy. With rising inequality, a growing public finance gap, and vocal calls from politicians, many people are asking the same question: should the UK introduce a wealth tax?

Economists and policy commentators have diverse opinions. Some of them say that it will balance the economy. Did you know that only a 2% wealth tax can raise £160bn in around 30 years?

However, some economists warn that it will be complex and difficult to design, administer and apply. This guide breaks down everything you need to know about taxes in the UK.

You will learn what a UK wealth tax is, how it could work in the UK, why it’s being proposed, where it’s controversial, and what alternatives exist.

What Is a Wealth Tax?

A wealth tax is a levy on the total value of a person’s assets, minus any debts. Unlike income tax or capital gains tax, which apply to flows of money (income earned or profit realised when selling an asset), a wealth tax is charged on the stock of assets someone holds.

These assets include property, investments, bank balances, business interests, pensions, luxury goods, and other forms of wealth. These taxes are applicable to people having a threshold of around £10 million and a rate between 1-2%.

Does the UK Currently Have a Wealth Tax?

No, The UK does not have a tax that currently applies to overall net worth.

Instead of a single wealth tax UK system, the country relies on separate taxes on assets, gains, and transfers. These taxes raise substantial revenue, but they do not treat all types of wealth consistently.

How Does a Wealth Tax Work in the UK?

There is no direct tax on overall net worth. Instead, the UK has different wealth-related taxes. Following is how a wealth tax works in the UK.

Rather than reflecting an individual’s total wealth over time, these taxes apply on specific moments such as sales, transfer and death.

Wealth-Related Taxes in the UK

The following is the details of the taxes in the UK.

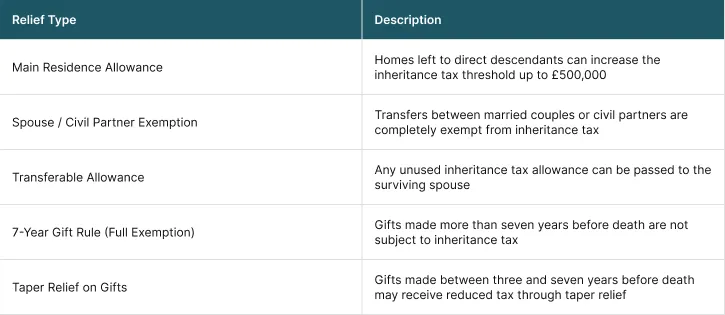

1. Inheritance Tax

The most common tax in the UK is the inheritance tax, which applies to acumulated wealth. The criteria of this tax are 40% on the estates and it should be above the value of £325,000 when a person dies.

There are some reliefs which are as follows:

In the 2024 budget, the government of the UK announced amendments regarding agricultural and business property reliefs. Businesses and farms are now taxed at 20% above a higher threshold of £1 million.

2. Capital Gains Tax

Capital Gains tax applies when you sell an asset for more than its cost. Gains above an annual allowance of £3,000 are taxable.

Losses can be balanced against gains, and no CGT is payable on the sale of a main residence.

Tax rates depend on income level and also asset type:

- 18% for basic-rate taxpayers

- 24% for higher and additional-rate taxpayers

- 32% on carried interest

Historically, capital gains were taxed at similar rates to income tax. Today, even after recent increases, CGT rates remain lower than income tax rates.

3. Council Tax

An annual property-based tax is the Council tax in the UK. It is charged on properties in England, Scotland and Wales. This tax is used for the public services such as street lighting, libraries, youth clubs, parks and care services.

In the year 2024-25, council tax raised an estimated £47.7 billion. Making it one of the largest property-related taxes.

4. Property Transactions Tax

Property transactions are heavily taxed in the UK, mainly through stamp duty land tax.

Stamp duty applies when you are purchasing property, especially for higher-value homes and additional properties. In recent years, it has raised around £15 billion annually.

While these taxes raise large sums, they only apply at specific moments. Such as when a property is bought, sold, or transferred, rather than reflecting ongoing wealth.

Why Does the UK Need a Wealth Tax?

Introducing UK wealth tax is a widely debated topic nowadays. It is not like the headline news, but there are some structural factors behind it.

The following are the factors:

- The wealth inequality gap between the rich and the poor.

- After years of spending, the government’s got a huge bill to pay, especially during the pandemic.

- Because of frozen thresholds, people are getting into higher tax brackets.

- Money made from wealth gets off easier than money from work.

One of the main reasons behind this tax thought is COVID-19. The government spent a lot to keep jobs and businesses afloat, and now the debt just sits there.

As a result, formal proposals for a wealth tax in the UK are now being discussed.

What Does a UK Wealth Tax Achieve?

Taxing wealth is not filling government reserves. It is twisted up with ideas about equality, democracy, and who really holds power. But whether it’s actually a good idea or not depends on what it actually gets, not what it says.

There are different proposals by the proponents regarding this tax:

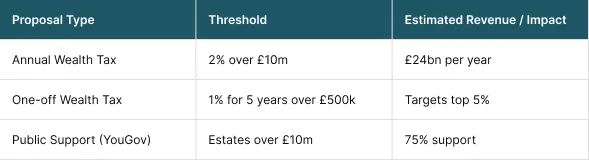

- The plan of an annual tax of 2% on net worth above £10 million is a popular one. Researchers at the University of Warwick estimate it could raise £24 billion a year.

- The Wealth Tax Commission suggests a plan called a one-off tax. The criteria are 1% a year, for five years, with over £500,000 in assets. It will hit above the 5% threshold.

These are not policies, just suggestions. No UK government said that we are doing this.

Who Will Pay Wealth Tax in the UK?

The wealthiest community is the target. Individuals with net assets of £10 million or more are liable. Taxable assets include property, investments, jewelry, businesses and cash. Debts are not included.

What Is the Public Opinion on Wealth Taxes?

It might be a huge surprise for you that the public isn’t against it. Inheritance tax is hated for sure, but recent polling suggests favor on taxes on extreme wealth.

Here is a current YouGov poll regarding wealth taxes (July 2025):

- 49% of voters strongly support a 2% tax on estates over £10 million,

- 26% backing it,

- Only 13% are not in favor.

Research shows that the majority of people are in favor of this tax system. They want to see higher taxes on extreme wealth.

International Experiences With Wealth Tax

This tax is very rare and many countries still do not have it.

Back in 1990, twelve developed countries had annual wealth taxes. By 2017, only four were left: France, Spain, Norway, and Switzerland. France has since cut its wealth tax down to just real estate.

Many countries dropped these taxes because they were complicated and didn’t bring in as much money as expected. The cost of making people pay often ate up a big amount of the revenue.

The global club of rich countries generally prefers broad taxes on capital income and transfers rather than wealth taxes. Still, policymakers admit that if you can’t tax capital income properly, a wealth tax might make sense.

Administrative Challenges of the Wealth tax

Running it is a whole different beast from visualising. There are major challenges that would be faced by the administration.

Legislators have to figure out the following:

- What counts as taxable wealth?

- How do you actually value things like private businesses, art, or land?

- Where do you set the threshold? What rates?

- Do you tax individuals or households?

- What about people who own a lot on paper but don’t have much cash?

Some assets are easy to value, shares, bank accounts, but others not. Private businesses, jewelry, farmland, art, even a house that hasn’t sold in years, these are complicated. Arguments over value would be endless, expensive, and time-consuming.

And a major concern is tax evasion. The higher the tax, the more incentive for the wealthy to shuffle their assets around. HMRC would be dumped a huge load and it would take years to get the system running efficiently.

How Quickly Could a Wealth Tax Be Introduced?

According to the UK think tank Institute for Government, it could take over four years to set up a proper wealth tax in the UK

There’s a lot to do:

- Draft the rules

- Hold consultations

- Build political support

- Write the laws

- Set up the admin

You could rush it, but then you risk legal challenges, endless arguments over valuations, and a mass of unintended problems.

Are There Better Alternatives Than a Wealth Tax?

Most of the experts say the wealth tax UK should start by fixing the taxes it already has on wealth. Right now, there are loopholes: capital gains, income from assets, and inheritance are all taxed differently, often benefiting the wealthiest.

Following suggestions should be the possible fixes:

- Making capital gains tax rates match income tax rates more closely

- Reducing or removing some inheritance tax breaks

- Updating council tax

- Doing a better job, taxing investment income

These measures could increase revenue and improve fairness without introducing a new tax system.

How Should the UK Tax Wealth Work?

The real challenge is designing policies that actually work, not just ones that sound big and exciting. This whole argument isn’t just about making more money. Wealth shapes who get ahead, who have power, who can afford a home, and who actually get a shot at opportunity.

If we overlook it, wealth can chip away at trust in government and even cause chaos with democracy.

The UK needs to tax wealth better. The real fight is over how to do it. For sure, a new wealth tax is possible. But in reality, it’s complicated, slow to roll out, and no one can guarantee it’ll actually work as planned.

Changing the taxes we already have on income, gains, and transfers might get us to fairer results faster. This could make the whole system more open and easier to follow.

Conclusion

A wealth tax UK is not easy to implement because of the challenges. It could increase revenue, reduce inequality, and align public policy with what people want, but there are some significant obstacles.

Recent polls show political support because it hits the wealthiest public. But when you turn the page, messy reality is how to keep people honest, how to value the asset and the economic reactions.

If the UK government and parliament want to implement this tax system, then complete measures should be taken. The tax system should be clear, well-designed and smooth to implement.

Sterlingcooperconsultants understands the importance of a perfect proposal for the wealth tax. If you want a well-designed and easy-to-implement wealth stability tax proposal, contact us today.

If you are exploring policy options, assessing impact, or seeking clarity on wealth taxation, our team can help you navigate the complexity with clear, evidence-based insight.

Get expert insights, policy updates, and practical guidance by connecting with us today.

FAQs

A wealth tax is a tax levied on an individual’s net wealth rather than on income or spending. Net wealth usually includes assets such as property, savings, investments, shares, and valuable possessions, minus any debts or liabilities. Unlike income tax, which is paid on what you earn each year, a wealth tax focuses on what you own.

Most proposals suggest it would only apply to very wealthy individuals, typically those with assets above a high threshold, such as £1 million or more.

If introduced, a UK wealth tax would likely apply to individuals whose total net wealth exceeds a set threshold. Taxpayers would be required to declare the value of their assets, including property and financial holdings, regularly. The tax would then be charged as a percentage of that net wealth, either annually or as a one-off levy.

Supporters argue that a wealth tax could help address growing inequality by asking those with the greatest financial resources to contribute more. Wealth in the UK is far more unevenly distributed than income, and much of it is concentrated in property and investments that benefit from long-term economic growth.

International experience shows that wealth taxes are challenging to implement. Several European countries, including France and Germany, have either abolished or scaled back their wealth taxes due to high administrative costs, valuation difficulties, and capital flight concerns. The global trend suggests that while wealth taxes are politically appealing, their success depends heavily on careful design, transparency, and public trust.

Recent Posts

What Are the Benefits of Automated Payroll Processing?

February 16, 2026

What Is a Payroll Report and Why Is It Essential for Every Business?

February 12, 2026