Posted by:

Admin

Date:

January 15, 2026

Category:

blogs

How Much Tax Do You Pay on a Second Home in the UK?

Buying a second home can be beneficial in multiple ways. It can contribute to additional income if you rent it out on holidays or regularly. However, you have to understand its tax implications. Tax on second homes is different from your main residence. A second home is taxed differently because it is not essential housing. So, the government charges extra to discourage speculative buying and free up homes for first-time buyers. Here is everything you need to know about it.

What qualifies as a second home?

A second home is a property you own apart from your main residence. You can have bought it or inherited it. In either case tax on second homes is levied on it. If your spouse buys a second home, then you’ll still have to pay tax on the second home. Here is what qualifies as a second home:

1. Buy-to-let properties

These homes are bought to be rented to tenants. So, even if the house is being used as someone’s main residence, it’s not yours so it counts as a second home.

2. Long-term investment properties

If you buy a property for the sake of using it as an investment, it is still considered a second home. The implication of tax on second homes does not change even if the property is empty.

3. Holiday homes

These properties are used for vacations. You may use them for residence occasionally but the tax on second homes has to be paid on them.

4. Short-term or seasonal lets (e.g., Airbnb)

If your property is rented out on a short-term basis like holiday rentals or Airbnb, it is considered a second home for tax purposes.

Christian A.L. Hilber and Olivier Schoeni

Tax on second homes:

Here are the taxes you may be liable to if you own a second home.

1. Stamp Duty Land Tax (SDLT):

This tax is a government tax on properties that are purchased in England and Northern Ireland. It applies only if the purchase price is above a certain threshold. It is paid when your property is:

- A freehold or leasehold property

- A property with a mortgage or bought outright

- Land or commercial buildings (separate rules)

Exemptions from SDLT:

You are exempted from this tax on second homes in the following cases:

- The home is inherited in a will

- You take ownership in a divorce or civil separation

- You buy a property worth under £40,000.

- You’re buying a caravan, mobile home, or houseboat

- You lease for over 7 years but pay under £40,000 and rent under £1,000/year

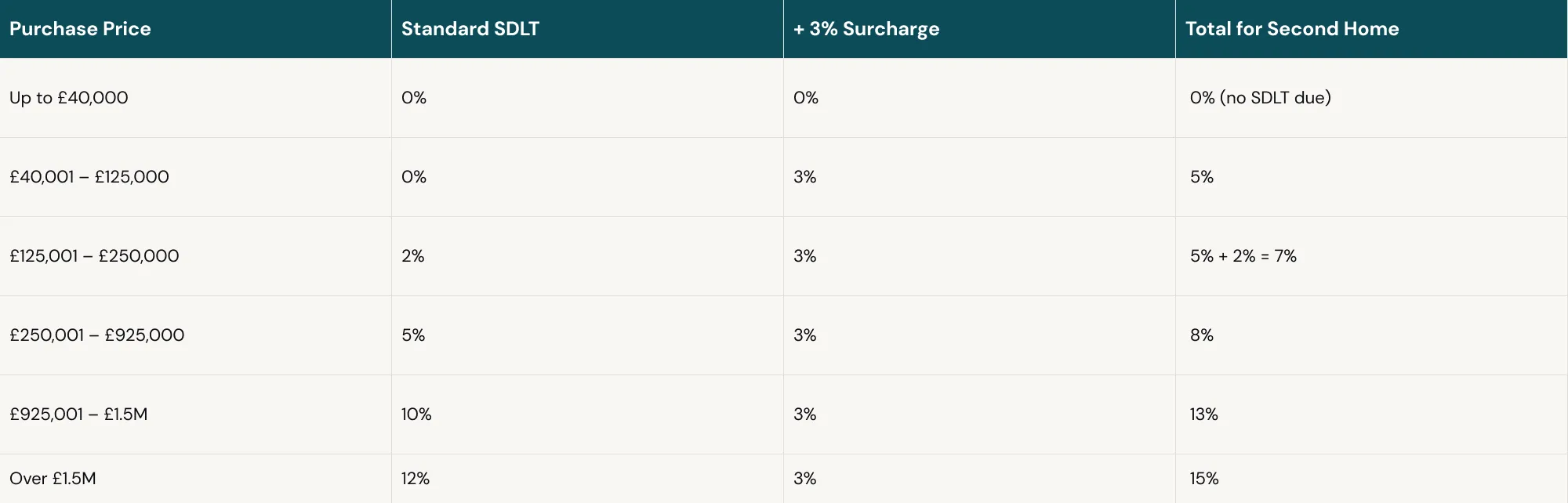

Stamp duty rates on a second home:

Second homes are charged with normal SDLT. The following surcharge is applied based on your location:

- 3% extra in England & NI

- 6% extra in Scotland

- Higher base rates in Wales

Here is how it is applied based on different purchase prices.

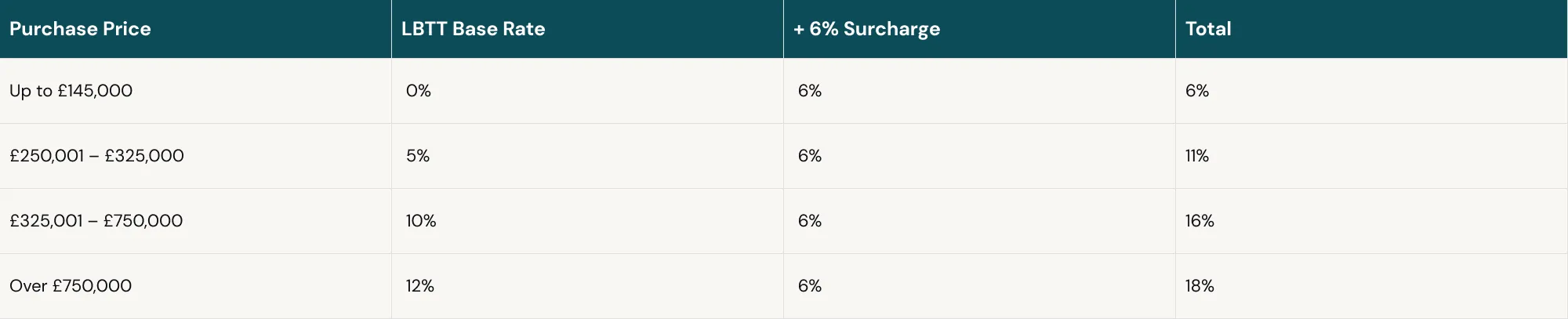

In Scotland, it is called Land and Buildings Transaction Tax – LBTT and is applied in the following way:

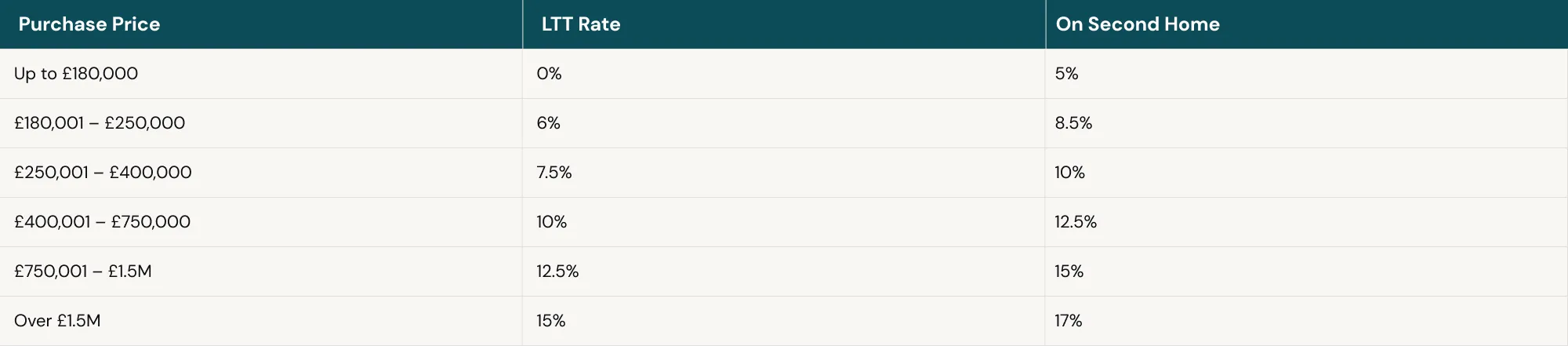

In Wales, it is called Land Transaction Tax – LTT and applied as follows

Refund of SDLT:

In England and Northern Ireland, you can get a refund of the 3 % surcharge in the following cases:

- You buy a second property before selling your main home.

- Then sell your old home within 3 years.

- You make a claim to HMRC within 12 months of selling the old home, or 12 months after filing the SDLT return (whichever is later).

Here is how you do it:

- Go to GOV. UK SDLT refund form.

- Create a Government Gateway ID.

- Fill in the online SDLT repayment form.

- Include details of both properties (first and second home), purchase and sale dates and tax amounts paid and requested.

2. Council tax

Council tax is a local tax that councils collect for domestic property. In exchange for this tax, councils provide you with services such as road maintenance, social services, waste collection, etc.. You have to pay council tax according to the following rules on a second home:

- You’ll usually have to pay full Council Tax on second homes.

- Some councils may offer a discount (e.g., 10%-50%), but this is entirely up to the local authority.

- Some councils charge more, applying a “second homes premium” — up to 2x the normal Council Tax.

For an empty home, it depends on your council how much they charge you. Some councils can offer a discount from 0% to 100% spending on their policy.

Second and empty homes premium:

Local authorities can now charge up to 100% extra (i.e., double the standard Council Tax) on properties classed as second homes. There is no grace period as the premium can apply as soon as the property meets the criteria. The authority must have given 12 months’ public notice of its intention to apply the premium. It can also be applied to empty homes that have been unoccupied and unfurnished for more than 12 months. The increase in charges is dependent on how much time has passed since they have been empty. Here is the increase after time:

- 100% extra after 1 year (i.e., 2× bill)

- 200% extra after 5 years

- 300% extra after 10 years

Second and empty home premiums are applied to council tax bills. There is no requirement for the council to notify individual taxpayers beyond public notice.

Exemption from Council tax:

There are exemptions to this tax on second homes. These exemptions can be temporary and permanent. Here is how they are applied:

Temporary 12-month Exemptions:

The following exemptions can be given for 12 months each:

Probate Exemption

This is given the property’s owner has died. It is granted from the date of the owner’s death.

Marketing Exemption

This exemption is applied if the property is being actively marketed for sale or let.

These exemptions can apply in succession i.e., 12 months for probate and 12 months for sale, a total 24 months exemption.

Other than these, you can apply for removal from the council tax list if your property:

- Is undergoing major structural work

- Is derelict, meaning not wind or watertight, unsafe for inhabitation or requiring extra repairs

You will have to apply to the council and inform them when the repairs are done. You’ll have to pay backdated tax if there is a delay.

Permanent Exemptions:

You can be given a permanent exemption from this tax on second homes if any of the following is true for you:

- Annexes used as part of the main home

- Armed forces accommodation requirement

- Caravan pitches and boat moorings

- Planning restrictions preventing full-time use. The following conditions should also be followed in this case.

- Cannot be occupied for more than 28 continuous days

- Must be used only as a holiday let

- Prohibited from use as a sole/main residence

These exemptions do not remove the standard Council Tax liability, only the premium.

Here is a summary of council tax on second homes being applicable in different situations:

| Situation | Second Home Premium? | Empty Home Premium? | Exemptions? |

|---|---|---|---|

| Holiday home | Possible | No | Depends on use/planning |

| Probate (12 months) | No | No | Yes |

| Renovating | Maybe | Maybe | If derelict or uninhabitable |

| Armed Forces home | No | No | Yes |

| For sale/let | Maybe | Maybe | 12 months |

| Planning use restricted | No | Maybe | Yes |

| Annex | No | No | Yes |

3. Income tax:

If you rent out your second home, you will have to pay tax on rental income. The amount of tax depends on your total income which includes your salary, rental income, and any other business or investment income. Here is how the tax rate is applied.

| Income | Tax Rate | |

|---|---|---|

| Personal Allowance | Up to £12,570 | 0% |

| Basic Rate | £12,571 – £50,270 | 20% |

| Higher Rate | £50,271 – £125,140 | 40% |

| Additional Rate | Over £125,141 | 45% |

For instance, you earn £35,000 from your job and £10,000 net rental income from your second home. Your total income is £45,000. You fall under the basic rate so you’ll pay 20% tax on your income over your personal allowance.

As for rental income, you are only charged tax on your profit, not the entirety of your income. Your rental profits can be reduced by using allowable expenses such as accountant fees, letting agent fees, service charges, maintenance and repair, etc.

4. Capital Gains Tax

Capital gains tax on second homes is the tax that you pay on profit when you sell your second home at a higher price than it was bought for. Capital gains tax on second homes is higher than on other assets. Therefore you should ask how to avoid capital gains tax on second homes.

| Taxpayer Status | Residential Property CGT Rate |

|---|---|

| Basic Rate (20% income tax) | 18% on the gain |

| Higher or Additional Rate | 24% on the gain |

For non-property assets like shares,it ranges from 10-20%.

Capital gains tax on second homes is to be reported immediately. From April 2020 it is to be reported in 60 days. So as soon as you sell your property, you have to calculate the gain. After that you have to report it to the HMRC online using the ‘Capital Gains Tax on UK Property’ service. Then, you have to pay this tax on second homes. All of this should be within 60 days of sale completion, or else there will be penalties.

How to calculate capital gains tax on second home

The formula for calculating capital gains tax on a second home is as follows:

Capital Gain = Sale Price – (Purchase Price + Allowable Costs)

Allowable costs include:

- Buying costs (legal fees, stamp duty, survey costs)

- Selling costs (estate agent fees, solicitor fees)

- Improvements (e.g., extension, loft conversion — but not repairs like repainting or replacing broken appliances)

How to avoid capital gains tax on second homes UK

You can’t avoid paying this tax on second homes altogether. We still must find ways on how to avoid capital gains tax on second homes uk. You can reduce it using the following ways:

1. Use Your Annual Capital Gains Tax (CGT) Allowance

Every individual gets a tax-free CGT allowance (£3,000 for the 2025/2026 tax year). You don’t have to pay any CGT if the gain is below this amount. Married couples can combine their allowances. This helps them shield £6,000 from this kind of tax on second homes.

2. Offset Allowable Costs

Another way of reducing the tax on second homes is to incorporate allowable costs. The allowable costs that you can offset include legal, professional, and estate agent fees. You can also offset improvements to the property but not the repairs and maintenance.

3. Transfer Ownership to Spouse

You can transfer a part of your property to your spouse or civil partner with no CGT. In this way, you’ll probably be in the lower CGT band, i.e., 18% tax on the gain.

4. Letting Relief:

If you have lived in your property as your main residence before renting it out, you are eligible for letting relief. However, it only applies if you share occupancy with your tenants. This relief on tax on second homes is not widely available anymore unless the second home was your actual residence before letting.

5. Plan the timing:

Spread property or asset sales over multiple tax years to use CGT allowances in both years and stay within a lower tax bracket.

Whether it be a job or a second home. Tax situation differs with each type of income. To learn more about taxes on your second job, check out our blog on how much taxes you pay on your second job.

Conclusion:

Owning a second home can be a good investment as well as a source of income. However, the myriad of taxes that are applied to it can be a hassle to calculate. Therefore, you should use professional services for tax calculations. At Sterling Cooper Consultants, we not only understand your tax liability, but we also make sure to claim every available allowance. With our taxation services, we make the most of tax reliefs and strategies and do your taxes on time to avoid penalties.

Taxes can be hectic, especially with a second home or a job.

For you it don’t have to be. Contact us now to get hassle free taxation done.

FAQs

No, you cannot have two main residences. Married couples and civil partners can also have only one main residence.

Coastal hotspots such as Padstow in Cornwall and Blakeney in Norfolk have 1 in 10 homes designated as holiday homes.

Day-to-day costs include utility bills, cleaning and gardening costs, admin costs and taxes.

According to data provided by the UK parliament, the number of second homes has not decreased because of the second home premium. It may be because the empty home premium is only applied after a year of the house remaining vacant.

No stamp duty does not apply to caravans or motorhomes.