Posted by:

Admin

Date:

May 29, 2026

Category:

blogs

Essential Insights into Accounting Practices for Sustainable Growth

Introduction

Ever felt confused when looking at financial reports?

Accounting can be confusing for you. But once you understand the basics it feels like a helpful tool.

Understanding accounting practices is important for any business. It helps businesses to keep their financial records organised.

Whether you’re managing a small startup or handling multiple clients. Accounting practices help you have better control. When you break things into simple steps you should understand the technical issues in a better way.

Research shows that in 2025 the global accounting services market is worth over 735 billion dollars.

This guide is designed to make accounting simple and also easy to follow. In the end you will feel more confident in managing the finances.

Key Takeaways

- Accounting practices are essential for business success, they help track income, control expenses, and support better financial decisions.

- Understanding the basics simplifies complex finance, once you know the core concepts, managing money becomes much easier.

- Choosing the right accounting method matters, cash accounting suits small businesses, while accrual accounting gives a more accurate financial picture for growing companies.

- UK compliance is crucial, following GAAP, filing with HMRC, and meeting Companies House deadlines helps avoid penalties.

- Different types of accounting serve different purposes, financial, tax, management, and forensic accounting all play unique roles in business operations.

- Strong bookkeeping builds a solid foundation, accurate records, proper categorisation, and regular reviews prevent costly mistakes.

- Efficient systems save time and reduce errors, using automation, clear processes, and structured workflows improves productivity.

- Technology is transforming accounting, tools like Xero and QuickBooks help automate tasks and improve accuracy.

- Payroll and tax compliance must not be ignored, managing PAYE, VAT, and CIS correctly is essential for UK businesses.

- Avoiding common mistakes protects your business, poor record-keeping, missed deadlines, and mixing finances can lead to serious issues.

- Modern accounting goes beyond numbers, it includes advisory services, data analysis, and strategic planning.

- Outsourcing vs in-house depends on the business stage, small businesses often outsource, while larger ones may build internal teams.

- Clear communication improves client relationships, transparency builds trust and long-term partnerships.

- Data security is a growing priority, protecting financial information is essential in today’s digital world.

- The future of accounting is digital and AI-driven, automation, cloud systems, and predictive analytics are shaping the industry.

- Continuous learning keeps you competitive, staying updated with new tools and regulations ensures long-term success.

What Are Accounting Practices?

Accounting practices mean the process of organising, recording and reporting the financial records. It is helpful for businesses to track every pound they earn or spend.

Businesses will face financial loss if they do not focus on the accountancy practice. In simple words it is the system that keeps financial information clear and well structured.

It also ensures that the reports are accurate and also useful for the decision making process.

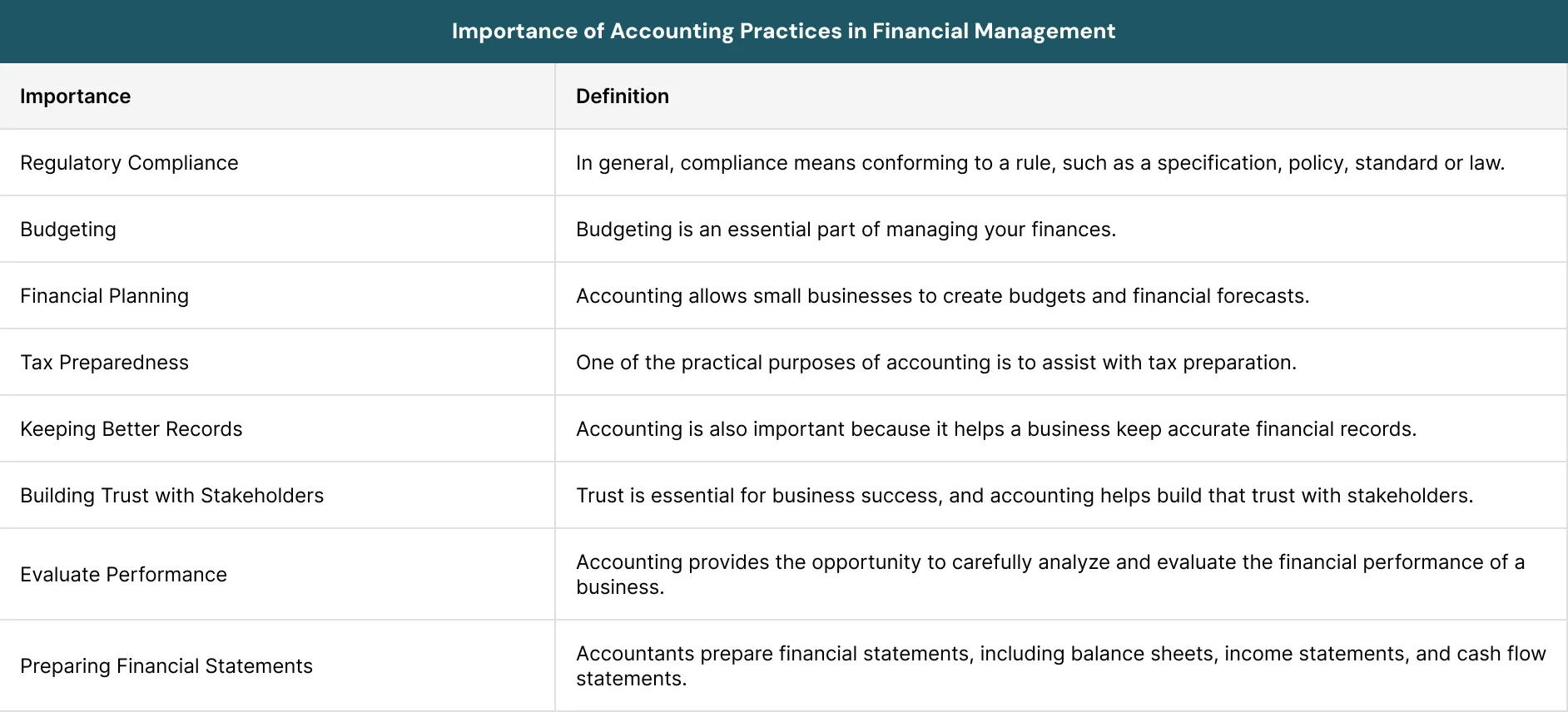

Importance of Accounting Practices

Good accounting practices can help businesses to understand their real financial position. This includes losses, profits and also cash flow.

Well structured financial data will reduce the risk of loss. It also improves the stability in business. It is helpful for business owners that they have to plan ahead instead of guessing.

Proper accounting is also required for tax and legal compliance in the UK.

GAAP and Its Role in Accounting

GAAP stands for Generally Accepted Accounting Principles. The main role of GAAP is to ensure that a company’s financial statements are complete and consistent. It can allow the investors to analyze and extract useful information from financial statements.

“Accounting is the language of business.”

— Warren Buffett

Accounting Practices Matter for Businesses and Accountants

Accounting practices are the backbone of every successful business. Even profitable businesses can face losses without proper accounting.

It helps to keep everything well organised and legally compliant. It builds trust and also helps to explain the financial health clearly for the accountants.

It is also helpful for business owners that they can make better decisions every day.

Methods of Accounting Practices

Accounting methods are the rules which business uses to maintain the record of the revenue and expenses.

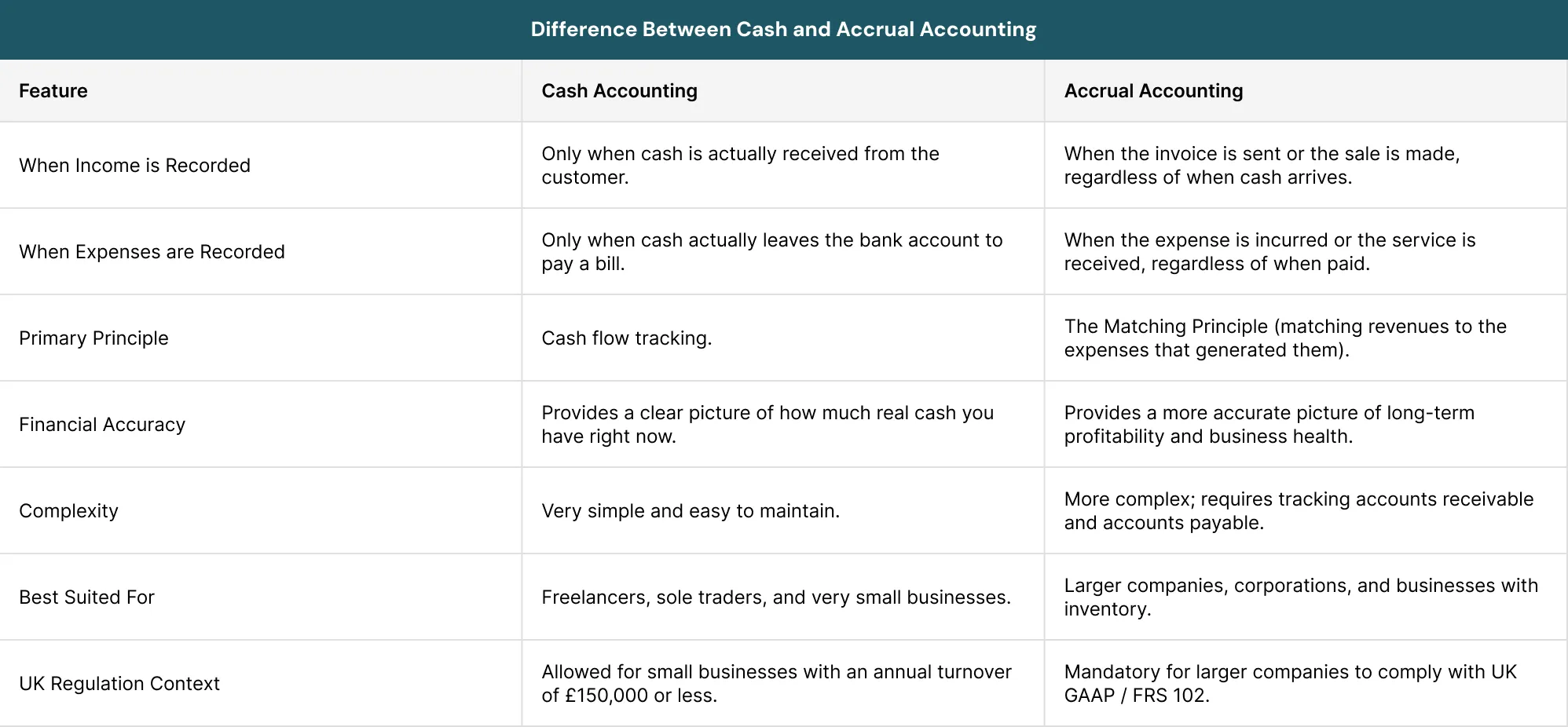

1. Cash Accounting

It helps to record the income and expenses when money is actually received or paid. Small businesses and freelancers use this method in the UK. Because it helps them to track real cash flow.

2. Accrual Accounting

Under accrual accounting, revenue is recorded when it is earned, not when it is received. This method follows the matching principle, which links to the income with related costs.

Larger businesses in the UK use this method. It helps in long-term financial planning.

What is the Difference Between Cash and Accrual Accounting?

The right method depends on your business size and its complexity. Small businesses often prefer cash accounting for simplicity. But on the other hand larger companies usually choose accrual accounting for accuracy. Because it provides better results for performance.

The right choice can help in the process of reporting and decision-making. It also ensures compliance with UK financial rules.

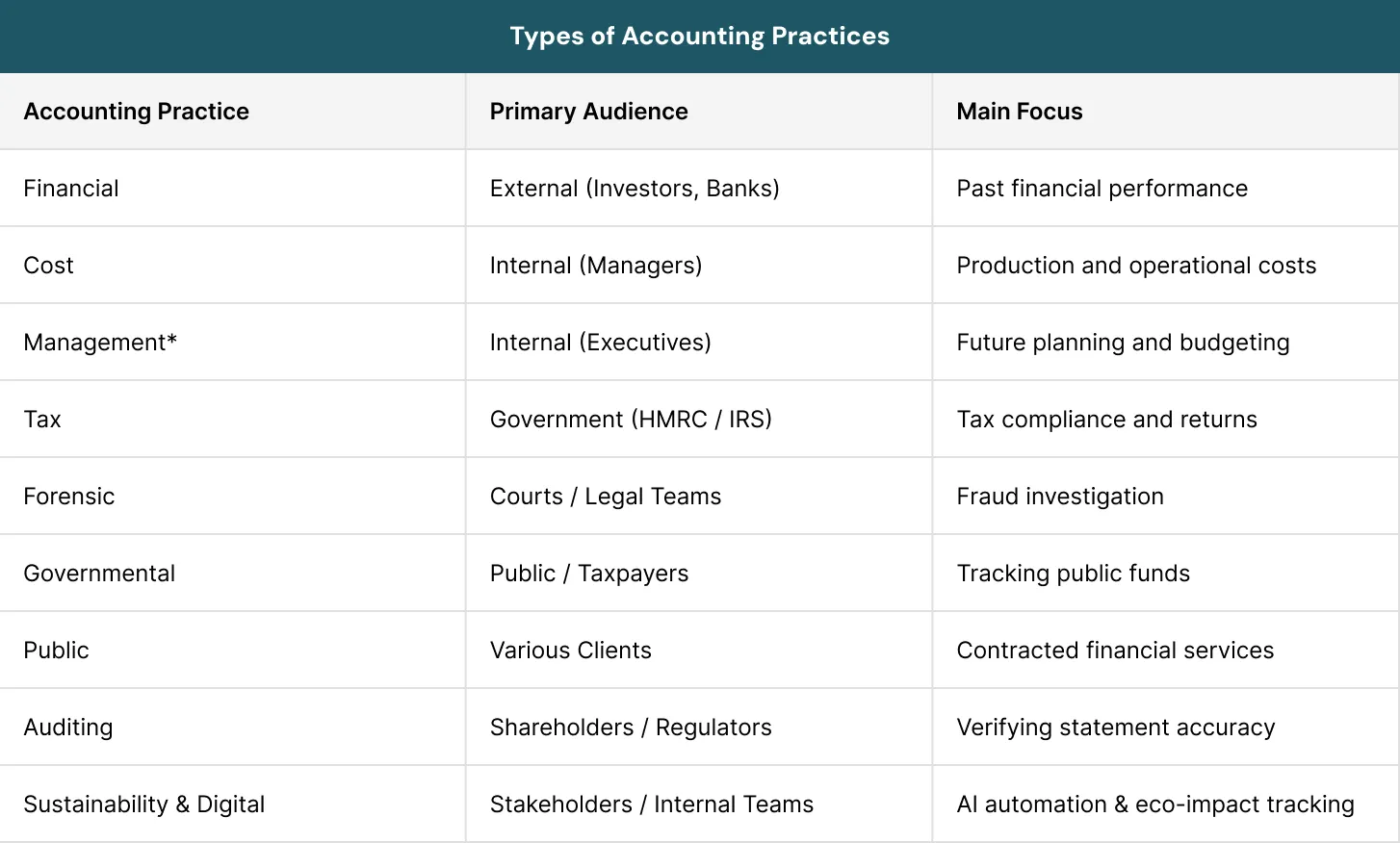

Types of Accounting Practices

There are 9 types of accounting practices which can help to improve your business.

- Financial Accounting

- Cost Accounting

- Management Accounting

- Tax Accounting

- Forensic Accounting

- Governmental Accounting

- Public Accounting

- Auditing

- Sustainability and Digital Accounting

Accounting Practices in the UK Context

Accounting practices in the UK are governed by a robust framework. It is designed to ensure transparency and consistency of financial positions.

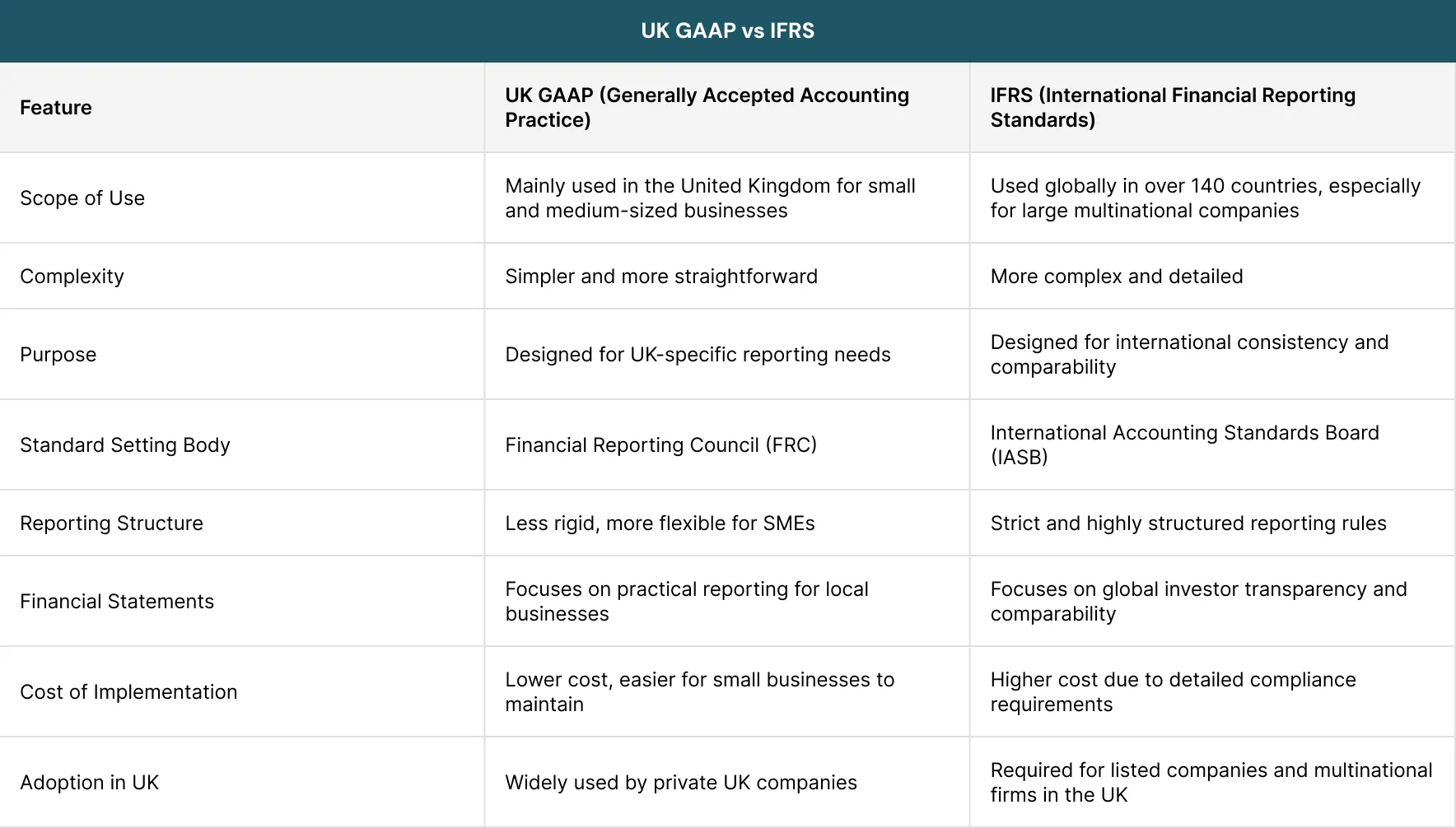

What Does UK GAAP Mean?

UK GAAP (Generally Accepted Accounting Practices) is a set of accounting rules which are used by the businesses in the UK.

It helps to ensure that financial reports are consistent. Small businesses use this process to keep accounting simple.

What are Key Financial Reporting Standards?

FRS standards help to guide the companies on how they prepare their financial statements in the UK. Each standard applies to different types of business. For example, FRS 102 is mostly used by medium-sized companies.

How to Ensure Compliance with UK GAAP?

Compliance starts with keeping the record accurate because every transaction must be recorded properly.

Regular reviews ensure that nothing is missed. This helps to reduce the errors. Many businesses also use software tools for compliance because this makes the process easier.

Filing Requirements

UK businesses must file the financial reports with HMRC and Companies House because these filings are legally required.

To avoid fines you must have to follow the deadlines because late submissions lead to penalties.

Proper filing helps to keep businesses in good standing. It also supports the accuracy of tax.

Read more: 5 Ways Cloud Accounting Can Save You Time and Money

Setting Up an Efficient Accounting Process

Efficient accounting helps you to save time and reduce stress. It also improves the financial process.

Efficiency also helps businesses to grow faster because it provides clear insights of finance.

Key Components of an Efficient System

A strong accounting system includes several key elements. These can help to maintain the accuracy.

- Separate the personal and business finances.

- Use a structured chart of accounts.

- Perform regular reconciliations.

- Use automation tools where possible.

- Track all expenses consistently.

Good Bookkeeping for Best Accounting Practices

Good bookkeeping ensures that every financial transaction is recorded properly. It also helps businesses to stay organised and compliant with the rules of tax.

1. Categorising the Income and Expenses

This practice improves the overall financial process. Best categorisation makes the financial reports useful. It is also helpful for tax preparation.

2. Managing Invoices and Receipts

Invoices and receipts must be stored in a proper way. Because they are proof of every transaction. Proper management helps to avoid the missing documents during audits.

3. Monitoring Cash Flow

Cash flow shows how money is used in the business whether its expenses or profit. Regular monitoring helps to avoid the shortage of cash. Good cash flow helps to ensure the stability of business.

4. Using Accounting Software

Accounting software helps to reduce your manual work and errors. It also helps you to easily track the income, expenses and reports.

In the present era software improves the accuracy and efficiency of the business.

5. Management of Payroll

Effective payroll management and compliance help to calculate the employee earnings and withholding taxes to prevent the penalties.

Automated software for tax deductions and maintaining the detailed records are the key components of management of payroll.

6. Payroll Software

Payroll software helps to simplify the salary calculations. It reduces the risk of manual mistakes. It also helps to save time and improve the accuracy of your business.

7. Registering with HMRC

Businesses must have to register with HM Revenue and Customs (HMRC) to run payroll legally. In this process employers deduct the tax and National Insurance from the employees salaries.

It is mandatory in the UK because it ensures that the employees pay correct taxes.

8. National Insurance and Pensions

National insurance and pensions are the legal requirements in the UK. In simple words it is the process where employers must have to contribute with National Insurance and pensions.

How to Prepare Year-End Accounts?

The end of the financial year is a time for any business or startups where they go through their financial performance.

1. Closing the Books

Closing the book is an important step for compliance. Because it finalises all the financial records of the year. It also ensures that all transactions must be recorded in the right way.

2. Financial Statements

Once the books are closed, now you can prepare the financial statements which show the health of business. It includes the profit, losses and assets.

3. Filing Accounts with Companies House and HMRC

Businesses must file their accounts with Companies House. They also file their Corporation Tax Return with HMRC.

Companies House: Accounts must be filed within nine months after the company’s financial year ends.

HMRC: The Corporation Tax Return is due for twelve months after the end of the accounting period. But the tax must be paid within nine months.

What is VAT Registration?

Value-Added Tax (VAT) is mandatory in the UK. It is a consumption tax which is placed on a product. Whenever value is added at each stage of the supply chain from production to sale.

It is crucial for startups because it impacts the pricing, cash flow and tax compliance.

1. How to File VAT Returns?

Every three months, startups are required to submit their VAT returns to HMRC.

This process involves reporting the amount of VAT charged to customers, the amount of VAT that has been paid while purchases and the net VAT payable to HMRC.

Filing the VAT returns has become simple. Now they are filed digitally in the UK and this system is called Making Tax Digital.

2. CIS Overview

The Construction Industry Scheme (CIS) is a set of special tax rules for the construction sector of the UK. It involves deductions of tax from payments related to construction work which can affect the contractors and subcontractors.

Accounting Practices That Damage Businesses

In the accounting practices, common mistakes include mixing the personal and business finances.

Another issue is that many businesses fail to keep their records organised. These mistakes can affect the finance of your business.

How to Avoid Mistakes?

Regular reviews of the balance sheet help to identify the problems early. This can help to prevent bigger issues.

Once you identify the problems the next step is to correct those mistakes because it increases the accuracy of your business.

Read more: Accounting Terms Made Easy: A Simple Guide for Non-Financial People

Best Accounting Practices Every Small Business Should Follow

Small businesses should always keep their personal and business finances separate. It helps to avoid confusion during the tax filing.

Track the income, expenses and cash flow on a daily basis is also important. For this you can use accounting software which can help to save time, reduce errors and also improve the financial accuracy.

1. Automation and AI

Automation and AI help businesses to complete their tasks faster.They help to reduce the manual work and improve the overall efficiency of the business.

These tools also help to track the expenses of the business and also organise financial data. This allows the accountants to focus on the planning and growth of the business.

2. Data Security

The modern accounting system helps to store important financial information. You can protect this information from cyber threats with the help of strong data security.

If you want to reduce the security risks you should use secure passwords.

3. Cloud-Based and Hybrid Accounting Software

Cloud-based accounting software allows businesses to access the data from anywhere.

While the Hybrid accounting software combines the cloud features with local storage for added security.

Popular Tools

To simplify the accounting tasks there are some popular tools which include Xero, QuickBooks and Silverfin.

How to Scale Your Accounting Practices?

If you want to scale your accounting practice then you have to start with improving efficiency and use the best technology. Regular training helps your practice to stay competitive.

1. Select the Niche

Select the niche which helps you stand out in a market because a clear niche builds trust. It also allows you to focus on a specific industry.

2. Building a Strong Online Branding

A strong online presence is very important in today’s digital world. It helps clients to find and trust you.

Your website, social media accounts and content should be well organised. Because it attracts the right audience.

3. Build the Networking

Build your strong network. It helps you to connect with other professionals. Building strong relationships leads to long-term business growth.

What is the Future of Accounting Practices?

The future of accounting practices is becoming more digital. AI will handle tasks like data entry and reporting. It makes accounting faster and more efficient.

Cloud systems will become more common in accounting, making processes easier in the future.

How Firms Can Stay Agile?

Firms can stay agile by understanding the customer needs and market trends. Regular training can help the employees to improve their skills.

Using modern tools also helps businesses to solve the challenges. Strong planning allows firms to stay competitive.

Conclusion

In the UK accounting practices are important for any business. From basic to advanced reporting every step plays a key role in your business.

By following best accounting practices and using the modern tools businesses can improve their performance.

At Sterling Cooper we know how important is accounting for your business. Our team is here to help you throughout the process.

Don't let confusing financial reports hold your business back.

Contact us today to simplify your accounting, tax filings, and cash flow management so you can scale with confidence.

FAQs

The 4 main practices of accounting are financial accounting, management accounting, cost accounting, and tax accounting. Each practice helps businesses manage finances, track performance, control costs, and stay compliant with tax regulations.

Accounting plays an important role in sustainability by helping businesses track environmental, social, and financial performance. It supports better decision-making, improves transparency, and helps companies meet sustainability and ESG reporting goals.

The 3 golden rules of accounting are: debit the receiver and credit the giver, debit what comes in and credit what goes out, and debit all expenses and losses while crediting all incomes and gains. These rules help businesses record financial transactions accurately.

The five main importances of accounting are tracking business income and expenses, helping with financial decision-making, ensuring legal and tax compliance.

The 5 main objectives of accounting are recording financial transactions, determining profit or loss, showing the financial position of a business, helping management make informed decisions, and ensuring compliance with legal and tax requirements.

Recent Posts