Posted by:

Admin

Date:

March 30, 2026

Category:

blogs

How to Assess Your Risk Tolerance Before Investing

Do you fear losing money when thinking of investing? Investing always comes with risk. There is always a chance that your investment could lose value, whether you buy:

- Stocks

- Mutual funds

- Bonds

The higher the risks, more rewards can be obtained. But nothing is guaranteed. Risk tolerance will help you choose the right investment plan and make better decisions based on your finances.

It is a matter of your peace of mind and your goals if you assess your risk tolerance. A study in the UK shows that 21% of adults are likely to make small investments in 2026. The idea of small regular investments looks good. It helps you to build long term wealth without stress. These kinds of investments are more affordable, especially for beginners.

In this blog, you will learn:

- What is risk tolerance in investing

- Why understanding risk tolerance comes first

- Why risk tolerance matters before you invest

- What factors influence your risk capacity

- How your investment time frame affects risk

- How to measure your risk profile

What Is Risk Tolerance in Investing

The degree of financial loss and uncertainty that an investor can take is called risk tolerance. It shows how much loss you can handle and how calmly you can tolerate market changes. This involves both the financial and emotional losses. It is shaped by your:

- Financial situation

- Personality and goals

- Time frame and life experiences

Some investors enjoy taking risks, while others prefer low risk investments. Most people sit somewhere in the middle. Your investment choice depends on your comfort level. Measuring risk tolerance is not easy.

Before building a portfolio, you should be careful about your emotions, your money and your long term goals. With the right strategy, low risk investments can help you grow your money over time. It can help you in:

- Retirement

- Buying a home

- Savings for the future

- Paying for education

You should consider these questions before you choose anything to make an investment.

- Are you ready to tolerate risk?

- How much risk can you handle?

The answers depend on you, your time and money situation. It also depends on your investment plan. It is important to consider if you feel comfortable with market fluctuations.

Why Understanding Risk Tolerance Comes First

Recent data shows that around 68% of UK investors now choose a careful approach while investing. This shows the importance of understanding your level of risk comfort. It helps you shape real investment decisions in 2026.

Risk comfort level is the most important factor which shapes:

- How do you react when markets move

- What results do you get over time

If you invest too aggressively, you may panic in downturns. If you sell at the wrong time, you miss the recovery from loss. If you invest too conservatively, you may not reach long term goals. Your returns may not match with inflation. When your risk level is properly aligned, you feel more confident and stay stable. You need to make careful decisions when the market is changing.

Why Risk Tolerance Matters Before You Invest

You must understand your risk capacity before investing. It helps you make right decisions during market ups and downs. The right risk level helps match investments to your goals, time frame and real financial needs. So choices feel calmer, more stable and easier to stick with over time.

Risk Capacity vs Risk Comfort

Risk tolerance includes two main parts:

1. Risk Capacity (Financial Ability)

Risk capacity is about what you can afford financially. It shows how much you can lose easily. If you need your investment money for daily costs like rent, food or medical bills. then your risk capacity is lower. If the money is extra and losing some would be upsetting, not stressful, then your risk capacity is higher.

2. Risk Comfort (Emotional Ability)

Risk comfort involves emotions. It shows how much uncertainty you can tolerate without panic. Some people stay calm during market drops. Others panic as soon as they see losses.

If market changes make you lose sleep, you may be taking too much risk by investing aggressively. There is a difference in willing to take risks and being able to afford them.

your finances may not support that risk level even if you show some guts. You may be able to afford the risk but still worry about prices swinging.

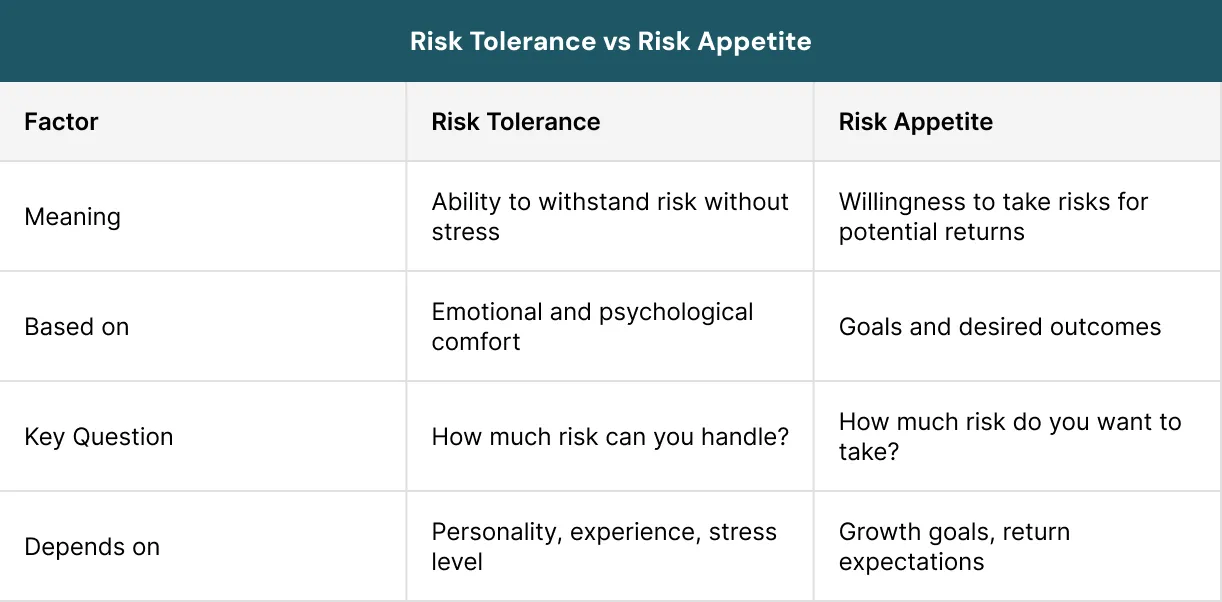

Risk Tolerance vs Risk Appetite

Risk tolerance is how much risk can be taken for a specific situation. It sets the limits and rules to handle that risk.

Risk appetite means the overall risk an organisation is willing to handle. In simple words, appetite is the bigger picture and tolerance is the boundary for each risk.

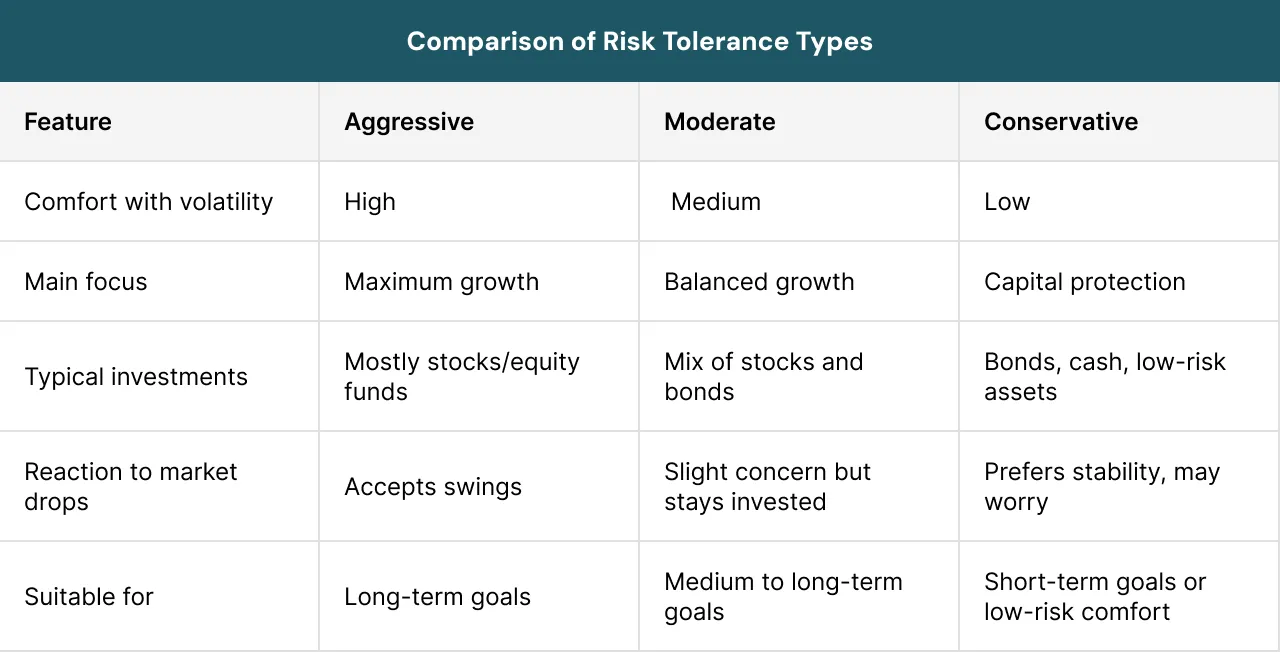

Types of Risk Tolerance in Investors

The approach to investments and risk tolerance varies for different people and organisations. Typical approaches of risk tolerance include:

Aggressive

- Comfortable with high volatility

- Willing to risk losses for higher returns

- Often invest heavily in stocks

- Aim for maximum growth

- Accept market swings

Moderate

- Prefer balance

- Mix of stocks and bonds

- Accept some risk but want stability

- Seek steady growth with controlled volatility

Conservative

- Prefer low volatility

- Focus on money preservation

- Choose safe investments

- Choose easy to access investments

- Avoid big changes in portfolio value

What Factors Influence Your Risk Tolerance

Risk tolerance involves some other factors as well. The factors that shape this are:

1. Investment Objectives

If your objective is high growth, you may need higher risk investments. If your objective is protecting assets, low risk investments may be better. Even if returns are smaller, they may be more suitable.

Your objectives must reflect your needs and your goals. They also reflect the risks you are willing to take.

2. Time Frame

Time frame means how long you plan to stay invested. In the long term goal (20–30 years), you can usually afford more risk. You also have time to recover from losses.

In the short term goal (1–5 years), lower risk may be right for you. This is important if you do not want large losses right before withdrawal.

Consider liquidity, that means how easily you can access your money when needed. Risk tolerance changes with time.

3. Reliance on Funds

Ask yourself if you depend on this money. Risk tolerance may need to be lower, if you depend on it. The important things such as:

- Retirement

- Buying a house

- Child’s education

Risk capacity should match your real financial needs too. Also consider your expenses like:

- Routine: housing, food, utilities

- Emergency: repairs, medical bills

- Long term: college, health care

4. Personality and Experience

Risk comfort level is deeply personal. It reflects:

- Your life stage

- Your investing knowledge

- Your past experiences

- Your personality traits

Some people easily handle uncertainty, while others prefer to avoid it. Your risk comfort level is shaped by your life experiences. It may change slowly over time due to:

- Family changes

- Economic shifts

- Personal events

How Your Investment Time Frame Affects Risk

Your time frame is very important for your risk tolerance. It simply means how long you can invest. If retirement is 30 years away, you have time to recover from losses. So short term drops may not affect your long term plan. You may be able to tolerate more risk.

If you need the money in two years for a home down payment, a big market fall could hit your goal. So, you may need more stability and lower risk. Cash options can make more sense.

In general, longer timelines can allow more risk. Shorter timelines often need more caution. This is not automatic. Your financial needs and your comfort should be the deciders.

Understanding Volatility and Investment Risk

There is uncertainty in investing. You might earn less than you expected or lose some or all your money. Market prices may change quickly. These ups and downs in prices are called volatility.

Successful investing is about managing risk, not avoiding it. – Benjamin Graham

Higher volatility generally comes with higher risk. It can bring higher returns, but it can also bring bigger losses. This relationship is called the risk return tradeoff.

Risk Return Trade Off

The risk return tradeoff means higher risk can bring higher returns. It can also lead to bigger losses. Higher risk investments like stocks or equity funds may grow more over time. Their prices can swing up and down.

Low risk investments like cash or some bonds usually move less. They may protect you from big losses. They often give smaller rewards. There are no high returns with zero risk. So, promises of guaranteed high returns with no risk should be a warning sign.

When assessing your risk capacity, the risk level should fit your goals and timeline. You cannot avoid risk because it always exists. It also fits your financial capacity and emotional comfort. It is important to understand how you tolerate risk.

Types of Risk Assessment Tools

Following are two main types of risk assessment tools:

1. Revealed Preference Exercises

They use made up choices to see how you react under risk. For example, they may ask if you want a guaranteed amount or a 50/50 chance to win more.

These tests can show decision patterns. They often do not feel real and do not always match how people invest in real markets.

2. Stated Preference Questionnaires

They ask how you think and feel about risk. For example, how do you react when markets fall?

Advantages:

- Easy to use

- Good for discussion

- They help people think about their feelings toward risk

Types of Investment Risk You Should Know

There are many types of risk that can affect your portfolio. Every investment comes with the following:

Company or Issuer Risk

This risk is linked to one specific company or organisation.

Asset Class Risk

The risk which is connected to types of investment like stocks, bonds or real estate.

General Market Risk

The risk which is associated with the overall market movement.

Industry Risk

The risk that affects a whole sector, like technology or healthcare.

Diversification and Low Risk Investments

Diversification is one of the best ways to manage investment risk. It does not guarantee profit and it cannot stop losses. But it helps to reduce the impact of bad investment. A simple way to diversify is to spread money across different asset classes like stocks and bonds.

Broad index funds can help with wider exposure too. Your investment portfolio should reflect the ease of risk involved.

Aggressive investors usually keep more stocks, while conservative investors prefer bonds or cash. Moderate investors choose a mix of both.

The guide on annual accounts will help you better understand plans and investments.

How to Measure Your Risk Tolerance

Measuring risk tolerance means looking at your emotions and your finances. How much can you lose before it gets stressful? A lot of people overestimate their toughness when things are calm. Online questionnaires are handy but can miss the mark. The better tools ask lots of detailed questions which can be handy.

Why Measuring Risk Tolerance Is Difficult

Risk tolerance is not just one type. It ranges from very careful to very risk taking. It also cannot be measured with a simple yes or no. Many websites offer free risk tolerance questionnaires. Some even suggest a portfolio mix based on your responses.

They can be helpful when you start, but they are not perfect. Some may promote the company’s own products. Many are not tested and quick quizzes can miss real emotions about risk. A more reliable result requires many detailed questions. So, it is not a quick process if done seriously.

Investing Is Not Gambling

Gambling style questions can feel off. Real investing affects your family, your future and your peace of mind which is totally emotional.

That is why good risk tools should feel relatable and reliable. They should also support meaningful conversations. They should help investors explain how comfortable they are with uncertainty. The goal is real understanding.

Aligning Risk Tolerance With Your Investment Plan

Your risk tolerance shapes your entire plan. It guides what assets you pick, how you diversify, how often you rebalance. High risk capacity is more stocks and low risk capacity equates to more protection.

Comfort is not enough. You also need risk capacity, which is what you can afford to lose. The right strategy matches your real life situation and supports your long term goals.

To learn more about managing your goals and income, check out our guide on budgeting strategies.

Important:

Your risk tolerance is not fixed. It evolves with your income, responsibilities, life stage and financial goals.

UK Case Study

The collapse of the café chain Patisserie Valerie highlights the importance of correct reporting. For years, the business appeared stable on the surface. Its financial reports showed the company was performing well and meeting its obligations.

However, a gap of around £40 million was later discovered in the company’s accounts. This gap had not been visible in earlier reports. It later became clear that the financial records were not accurate and the true level of debt had not been properly shown.

As a result, the published accounts created a misleading picture. Once the issue became public, the impact was immediate including:

- Investor confidence dropped sharply

- Banks became more cautious in their support

- The company faced severe cash flow pressure

The business eventually went into administration. This led to store closures and job losses across the UK.

Financial reports must be both accurate and honest. Filing on time is not enough if the information itself is not correct. For directors, the risks go beyond financial loss. Poor reporting can lead to:

- Loss of trust from lenders and investors

- Damage to the company’s reputation

- Impact on more business opportunities

Conclusion

Your annual report in 2026 is more than an item on your list. It’s about creating your company’s reputation and knowing where you’re headed. A good, plain-language report builds trust, keeps you on the right side of the law and gives you a better sense of where your business stands.

But don’t stop there and get to the bottom of things. Understand and see what the numbers mean. Figuring out what’s working and what needs to change to make your future plans solid. Your report speaks for your business, showing others how you’re doing and what you stand for.

If you start early, everything will be easier. You won’t be scrambling at the last minute and things will be neater overall. Over time, it will become a routine that can give your business stability and set it up for growth. Once reporting is a second nature, you’ll build a company that people can trust, one that is clear and trustworthy.

Sterling Cooper helps you understand what annual reporting data is and how to present it in the best possible light.

Get in touch today to improve your annual reports and stay compliant with ever evolving standards.

Take control of your investment decisions by understanding your true risk tolerance.

A well aligned strategy can help you stay consistent, reduce emotional stress and work steadily toward your financial goals.

Speak to a specialist today to invest with confidence and make balanced decisions.

FAQs

Yes, risk tolerance can change due to life events, income changes or financial responsibilities. As your situation evolves, your comfort with risk may also increase or decrease, so regular review is important.

It is generally recommended to review your risk tolerance at least once a year. You should also reassess it after major life events such as a job change, marriage or significant financial change.

Yes, age often influences risk tolerance. Younger investors usually take more risk due to longer time horizons, while older investors prefer lower risk to protect accumulated wealth.

Investing beyond your comfort level can lead to stress and emotional decisions. You may panic during market drops and sell at the wrong time, which can negatively impact returns.

No, risk tolerance should be considered along with goals, time horizon, income stability and liquidity needs. A balanced approach helps build a more effective and sustainable investment strategy.

Recent Posts