Posted by:

Admin

Date:

March 18, 2026

Category:

blogs

What Is FRS 102? A Simple Guide for UK Businesses

Ever wondered how billionaires keep track of each penny? The financial statements are the answer. Financial statements are an important part of any business. These statements help understand how a business is performing. To keep financial reporting consistent, accounting standards are used. FRS 102 is the most widely used framework across the UK and the Republic of Ireland to prepare the financial statements.

FRS 102 is a key part of UK Generally Accepted Accounting Practice (UK GAAP). Many companies use it when preparing annual financial statements. The UK GAAP was introduced by the Financial Reporting Council (FRC). FRC is the body responsible for setting accounting standards in the UK.

The goal of the framework is simple. It ensures that statements show the true and fair position of a business. The FRC states that 3.4 million businesses use these standards to prepare their financial reporting.

For many companies, understanding the framework is important. It helps them follow the right UK accounting rules. This also provides reliable financial reports.

Moreover, it explains how businesses should record financial information. This includes items such as:

- Assets

- Liabilities

- Revenue

- Expenses

This guide explains:

- What is FRS 102

- Why it was introduced

- Which businesses use it

- Comparison with other accounting frameworks

- Key sections of FRS 102 standard

- Non compliance risks

- Common mistakes to avoid

- Tips for smaller businesses

- Common queries

- Real world example

- Glossary of common terms

What Is FRS 102?

FRS 102 stands for the Financial Reporting Standard. It is one of the main accounting standards used under UK GAAP. The standard provides guidance on how companies should prepare financial statements.

The UK accounting system included many different standards. These were often complicated and difficult to manage. This standard simplified the system. It replaced dozens of individual standards. Businesses now use one framework that covers most accounting topics.

Accounting terminologies may seem technical at first. If these terms are new to you, our guide on accounting terms explains them in simple language.

Why Was FRS 102 Introduced?

UK accounting rules were fragmented earlier. They were spread across many different standards. This made financial reports much more complex. Many businesses struggled to understand ESG reporting requirements. FRS 102 changes were introduced to ease reporting.

As a result, a modern accounting framework was put in place. Most of the UK private companies now use this system. The main objectives are to:

- Make accounting rules simpler

- Bring UK rules closer to global standards

- Make financial reports clearer

- Help businesses follow the rules more easily

FRS 102 Updates and Effective Dates

The framework first became effective on 1st January 2015. Small companies applying Section 1A have also benefited from simplified rules.

The FRC reviews the standard every 5 years. This helps to keep the rules up to date. Some changes have been applied with time. It includes updates to disclosure requirements and financial reporting.

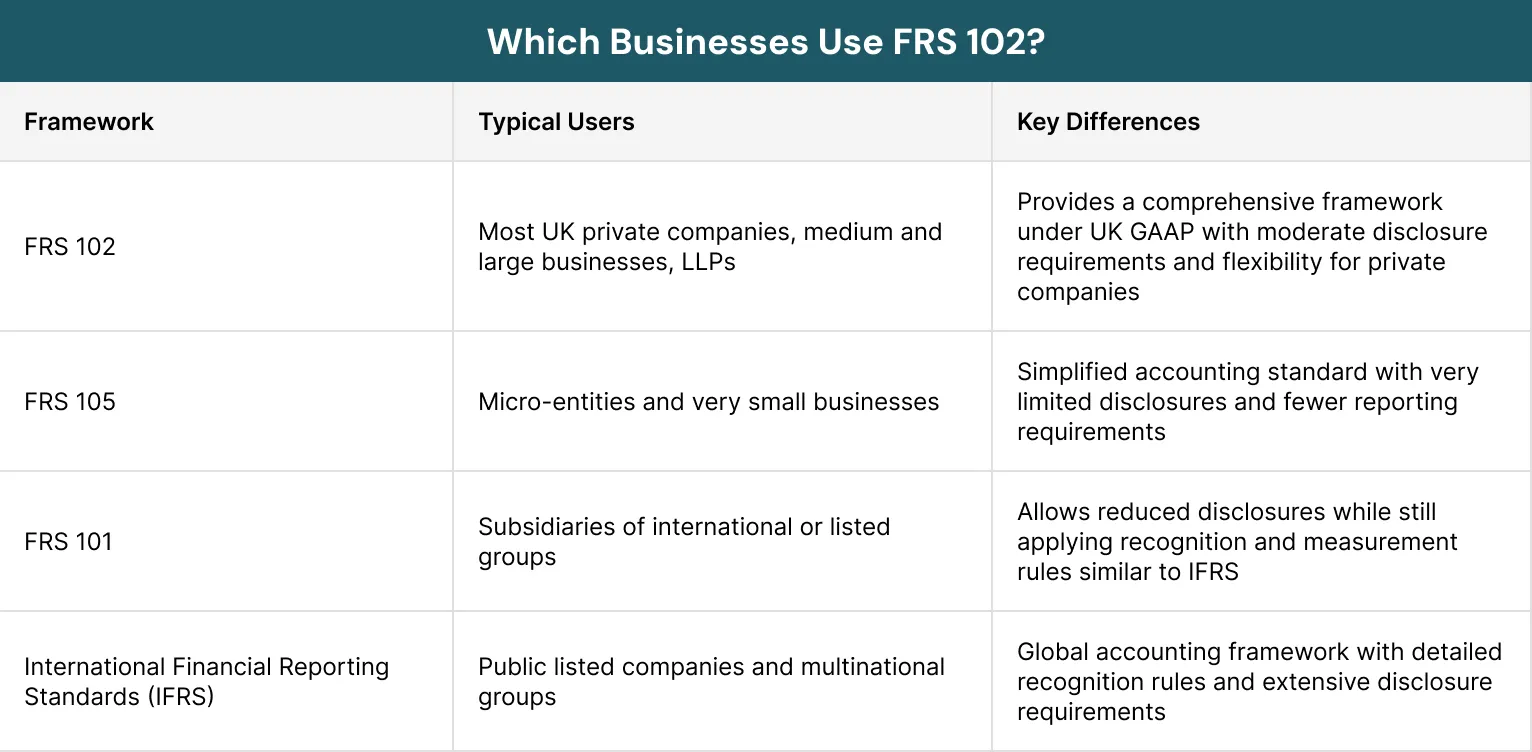

Which Businesses Use FRS 102?

Many firms ask which reporting rules they should use and who they apply to. One common set of rules is used by many groups that prepare reports under UK GAAP. These rules are often used by:

- Private limited firms

- Medium sized firms

- Large private firms

- Limited liability partnerships

- Some parts of global groups

A company’s size and its duty to report helps decide which set of rules it should use. They set clear rules but still allow businesses some flexibility.

The table below shows the main standards and who usually uses them:

Smaller businesses often use FRS 105. Large multinational and listed companies usually follow IFRS, as it is recognised across the world.

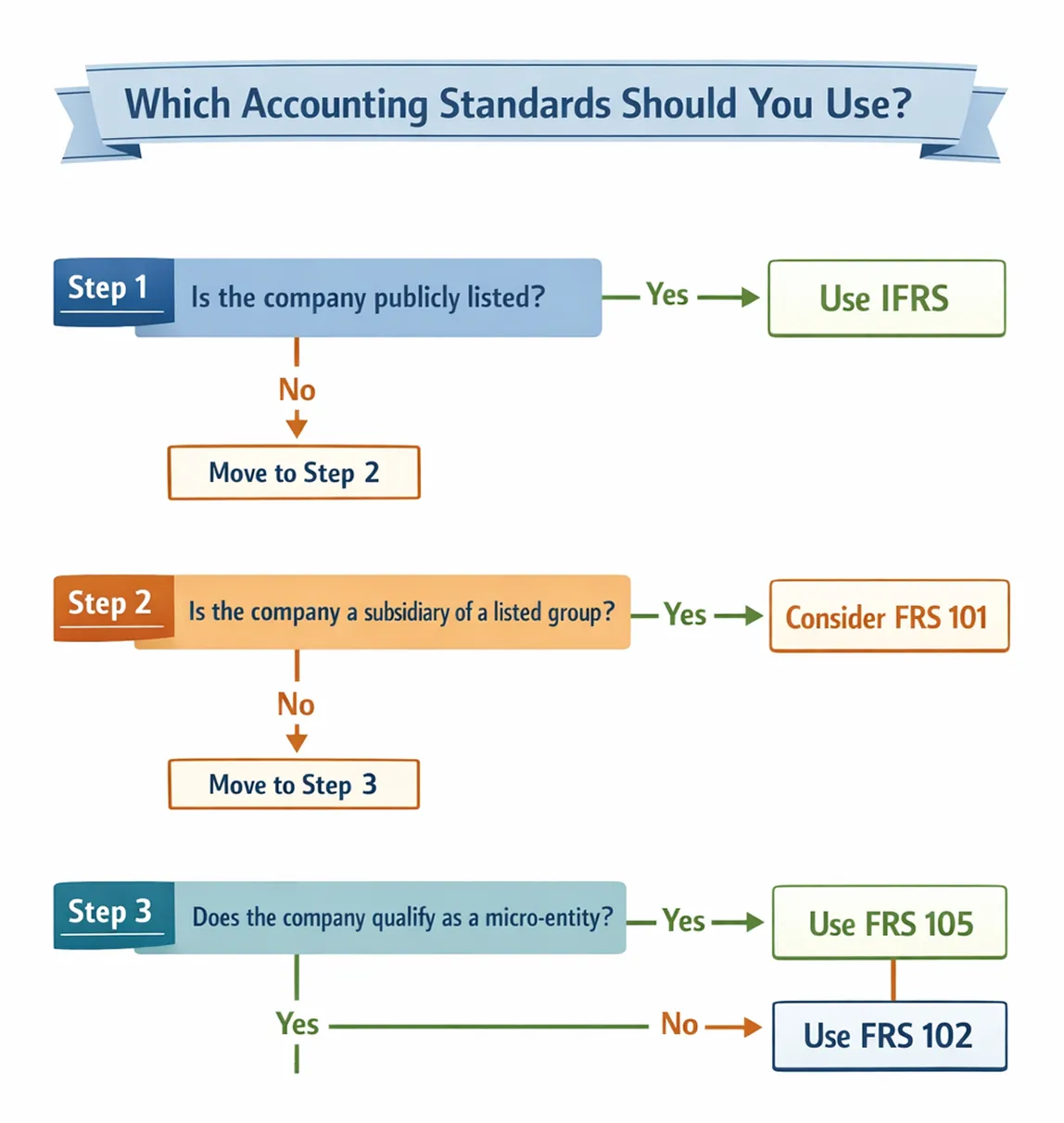

The steps below explain how the main UK accounting standards relate to each other.

Key Sections of FRS 102

Multiple sections are organised in this framework. Each section covers a different accounting topic. Some of the important sections are:

Section 1 – Scope

This section explains which entities must apply the standard. It also requires financial statements to present a true and fair view of the business.

Section 2 – Concepts and Principles

Section 2 describes the basic concepts of financial reporting. Key ideas that form the basis of accounting under this framework include:

- The purpose of financial statements

- Recognition and measurement principles

- Definitions of assets and liabilities

Section 4 – Statement of Financial Position

This explains how companies should present their balance sheet. Items must normally be classified as current or non current. The balance sheet should show:

- Assets

- Liabilities

- Equity

Section 17 – Property, Plant and Equipment

This section explains how companies record physical assets. These assets are recorded at cost and their value is reduced over time. Examples include:

- Buildings

- Machinery

- Vehicles

- Equipment

Section 18 – Intangible Assets

This section deals with non-physical assets. These assets reduce in value over their useful life. For example:

- Software

- Patents

- Trademarks

Section 23 – Revenue

This section tells when revenue should be recorded. These standard changes allow use of simple methods to understand when income should be recorded. The goal is to ensure revenue reflects the value delivered to customers.

Financial Statements Required Under FRS 102

Businesses using this standard usually prepare a few financial reports. These reports show the financial position of a business. These financial statements must include:

Statement of Financial Position

Mostly referred to as the balance sheet, it shows assets, liabilities and equity of a business.

Profit and Loss Account

This report shows income, expenses and profits of a business.

Statement of Changes in Equity

This statement explains how shareholders’ equity changed during the year.

Statement of Cash Flows

This report tracks cash movement from different business affairs like:

- Operating activities

- Investing activities

- Financing activities

Notes to the Financial Statements

The notes provide extra details about the figures shown in the accounts. Small companies using Section 1A may qualify for reduced disclosures.

Businesses use this system to make their financial reports. If you want to understand how these reports work in practice, read our guide which explains annual accounts in detail.

Benefits of FRS 102 for Businesses

These new rules bring clear gains for many businesses. They help make reports easy to read and simple to follow. key benefits include:

Standardised Reporting

This framework gives clear rules that help firms prepare the reports in the same way each year.

Clearer Financial Reports

Using the same methods makes accounts easier to read and easier to trust.

Closer to Global Standards

Many parts of this framework match global accounting rules. This helps UK reports to stay close to world standards.

Flexible for Smaller Businesses

Smaller firms can use simpler disclosure rules. This helps make the reporting process less complex.

Challenges When Applying FRS 102

FRS makes many parts of accounting easier to manage. Still many firms still work with skilled accountants to stay within the rules. Some firms may face issues such as:

- Valuing financial assets

- Working out deferred tax

- Keeping up with rule changes

- Dealing with company mergers or buyouts

- Handling complex finance tools

- Preparing audited financial reports

Why FRS 102 Matters for UK Businesses

Knowing what FRS 102 is matters because it plays a key role in the UK business reporting. It helps make sure financial reports are:

- Accurate

- Consistent

- Clear

- Prepared in line with rules

When reports are clear and easy to trust, investors and lenders can see how a business is doing. Using the framework the right way also builds trust and helps reduce the risk of problems later.

Non Compliance Risks

If accounting standards are not applied correctly, businesses may face several problems. Keeping records accurate helps reduce risks which may include:

- Financial statement corrections

- Audit problems

- Loss of investors or lenders

- Regulatory questions from authorities

Common Mistakes to Avoid

The errors can result in incorrect financial statements. They also require the accounts to be revised later. Some errors businesses make include:

- Incorrectly capitalising costs related to assets

- Misclassifying current and non current liabilities

- Recording revenue before it is earned

- Incorrect treatment of deferred tax

- Not applying Section 1A disclosure rules correctly

Tips for Smaller Businesses

For small businesses, a few simple steps can help them follow accounting standards more easily. Good record keeping and organised reporting can also lower the risk of compliance issues.

- Use accounting software that supports UK GAAP reporting

- Keep records of assets when purchased or sold

- Check depreciation regularly

- Maintain clear documentation for financial transactions

Is UK GAAP the Same as FRS 102?

It is not the same as UK GAAP. It is a part of the UK GAAP. UK GAAP is an overall system of accounting rules. Different standards exist in this system which include:

- FRS 102

- FRS 101

- FRS 105

Each standard is designed for different types of businesses such as:

- Most private companies use FRS 102

- Micro entities often use FRS 105

Can I Change From FRS 102 to FRS 105?

A business can switch from FRS 102 to FRS 105 in some cases. Companies should review the eligibility rules carefully before switching. This is only possible if the company qualifies as a micro-entity. To qualify, the business must meet certain limits. These limits usually relate to:

- Annual turnover

- Balance sheet total

- Number of employees

FRS 105 is a simpler standard. It includes fewer disclosure requirements. This makes it easier for very small businesses to prepare their financial statements. It also provides fewer accounting options than FRS 102.

Can You Capitalise Stamp Duty Under FRS 102?

Stamp Duty can be capitalised in many cases. It can be included as a cost of an asset when property is purchased.

For instance, if a company buys a building, the total cost may include:

- Purchase price

- Legal fees

- Stamp duty

These costs can all be added to the value of the asset on the balance sheet. The asset is then written down over time through depreciation. But the correct accounting treatment may vary depending on the transaction.

Real Example of an Accounting Mistake Under FRS 102

A small company called Jasper Ltd prepared its accounts using this framework. The finance director did not record deferred tax on an investment property gain.

It was later found that the company should have recognised this tax under FRS 102. Since, the tax had been left out of the accounts, the financial statements had to be corrected.

This example shows an important lesson. Even small mistakes in financial reporting can lead to corrections later. That is why many businesses rely on accountants when applying the standards.

Accounting for Software Development in a Technology Company

A small technology company develops its own business software. During development, the company spends money on programmer salaries, testing, and system design.

Under this framework, some development costs can be recorded as an intangible asset if certain conditions are met. This means the cost is not treated as an immediate expense.

Instead, the company records the software as an asset on the balance sheet. The software is then written down over the years it will be used. This process is known as amortisation.

For example, if a business spends £100,000 to develop software and plans to use it for five years. Then the cost can be spread over those five years. This helps show how the software adds value to the business over time.

Definition of Common Terms

Asset: A resource owned by a business that has economic value.

Liability: A financial obligation or debt owed by a company.

Equity: The value of ownership in a business after liabilities are deducted.

Deferred Tax: Tax that will be payable or recoverable in the future due to accounting timing differences.

Amortisation: The gradual reduction in value of intangible assets over time.

Final Thoughts

FRS 102 is not just a technical accounting standard. It provides a framework that helps businesses present financial information in a clear and consistent way. By following UK GAAP rules, companies can make sure their financial statements show a true and fair picture of their position.

Understanding the standard can help businesses avoid reporting errors and follow accounting rules correctly. Reviewing records regularly and keeping clear documents can also make the reporting process easier.

Sterling Cooper ensures your accounts follow the correct standards and reduces the risk of compliance issues later.

Get in touch today to ensure your financial reporting is accurate, compliant, and prepared according to the correct accounting standards.

FRS 102 compliance helps businesses produce accurate financial statements and avoid reporting mistakes.

Speak to a specialist today to review your financial reporting and ensure your accounts are prepared in line with the standards.

FAQs

FRS 102 is issued by the Financial Reporting Council (FRC). The FRC is the organisation responsible for setting and maintaining accounting and auditing standards in the UK. It updates these standards when financial reporting rules change or need improvement.

FRS 102 is reviewed and updated from time to time by the Financial Reporting Council. Updates are made to keep UK accounting rules aligned with international practices and modern business needs. Companies must check whether any new amendments apply to their financial statements.

Not always. Small companies can apply Section 1A of FRS 102, which allows reduced disclosure requirements. This means they can prepare simpler financial statements while still following the main accounting principles of the standard.

Yes, many charities and non-profit organisations in the UK also prepare their accounts using FRS 102. However, they usually apply it together with the Charities Statement of Recommended Practice (SORP), which provides additional guidance for charity reporting.

If a company applies the standard incorrectly, its financial statements may not give a true and fair view. This could lead to corrections, audit issues, or questions from regulators. In some cases, the company may need to restate its financial statements.

Recent Posts