Posted by:

Admin

Date:

February 25, 2026

Category:

blogs

Understanding the 40% Tax Bracket in the UK

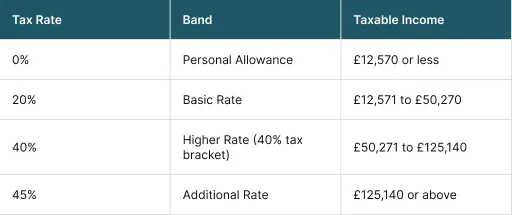

Ever looked at a pay rise and felt underwhelmed? You just encountered the 40 tax bracket. The 40% tax bracket is the income tax applied to income between £50,271 and £125,140 for the 2025/26 tax year in the UK. Due to frozen tax thresholds until 2028, more and more people are entering this bracket.

People hear “40% tax” and instantly think: ‘Do I lose 40% of all my money?’

Short answer: No.

Long answer: Keep reading and this guide will explain in simple terms..

In this article, we’ll break down:

- What the 40% tax bracket actually is.

- When the 40% tax bracket starts.

- What the 40% tax bracket 2025 looks like.

- How much is the 40% tax bracket in real, take-home terms?

What Is the 40 Tax Bracket 2025 to 2026?

The 40% tax bracket is the higher rate of income tax in the UK. It only applies to the part of income taxable under this band.

As a general rule:

- You do not pay 40% on everything you earn.

- You only pay 40% on the income above a certain threshold.

Here is how the UK’s progressive tax system works:

So the 40 income tax bracket sits in the middle, affecting higher earners but not ultra-high earners.

Related: 2025–26 Tax Year Updates: Understanding the Latest Changes.

When will the 40 Tax Bracket Elevation begin?

The starting point of 40% tax band is one of the most frequently posed questions. Under the present tax regulations:

- The 40% tax bracket starts at £50,271.

- It is imposed on top of usual tax free personal allowance and basic rate band.

Thus when your taxable income goes beyond £50,270, you will be in the 40% tax bracket.

How Much Is the 40 Tax Bracket?

To compute the amount of 40% tax bracket 2025, it is important to know that it is only applied to the portion of the income that falls in the band.

For example,

Assuming that the income is £60,000, then tax rate will be:

- 0% for the first £12,570.

- 20% for the next £37,700.

- 40% for the last £9,730.

It should be mentioned that the 40% tax rate is imposed only on the amount of income exceeding £50,270. It is not applicable to all income.

Why the 40 Tax Bracket Hits Hard

The 40% tax bracket is a progressive tax that targets the high earners to give their equitable share of tax. Nevertheless, it may be meaningful to a great number of individuals in this category.

Here is why this happens.

Nation Insurance Stacks above.

The income tax is not all.

In the 40 income tax bracket, you are also liable to:

- NI 8% £12,570 to £50,270 (rates may change depending on reforms).

- 2% NI above £50,270.

Then in the 40% tax bracket your marginal deduction is:

- 40% income tax.

- 2% NI.

- Total = 42%.

Premium on each £100 over £50,270:

You keep roughly £58.

This mix has been referred to as fiscal drag because of frozen thresholds.

Loss of Allowances Later on

This is where technical knowledge comes in play.

Between £100,000 and 1£25,140:

- For every £2 of personal allowance lost is £1.

- Any loss in allowance will increase the amount of your income that is taxable.

This creates:

- 40% tax on income.

- Add 20% additional effect lost allowance.

- Effective marginal rate of 60%.

This does not fall under the 40% tax bracket but it falls within the tax bracket of higher rate.

This is amongst the most misconstrued aspects of the UK tax system.

Once you approach £100,000:

- Your Personal Allowance begins to shrink.

- The effective tax rate may reach 60%.

That is well above the norm 40% tax bracket.

The 40 Income Tax Bracket and How It Works.

Not all of your income is subject to the 40 tax bracket. It is applicable to the portion that is above £50,000. The 40% band runs from £50,271 up to 1£25,140. Above £125,140, there is the 45% rate.

Income greater than £100,000 is charged on other income less £12,570 tax-free allowance, which then falls to zero at £ 125,140.

Taxable income may be minimised by pension contribution and charitable donations which may ensure that earnings are not over 40.

Tax Reduction in the 40 Tax bracket.

It can be overwhelming for the 40% tax bracket. Nonetheless, it can be reduced or mitigated through the law.

Pension Contributions

The taxable income is decreased by pension payments. It is a tax saving of 40% in £1 to pension. Making a contribution to a pension lowers taxable income.

This constitutes one of the strongest tools to individuals in 40 income tax bracket.

Salary Sacrifice

You are able to trade in part of your salary with non-tax benefits.

Common for:

- Pensions.

- Electric cars.

- Childcare.

- Pre-taxes taxable compensation.

- Gift Aid Donations

Gifts increase your fundamental band. It assists you to reclaim a higher tax relief. Donations to charity are subject to Gift Aid, which means that the charity receives a refund of taxes on the gift and you are subject to less taxation.

Marriage Allowance (limited cases)

You can transfer certain of your assets to a spouse who is in a lower tax bracket. Only when one of the partners makes a low income than the allowance. Not always helpful in earners in 40% tax bracket but worth considering.

Individual Savings Accounts.

Money invested in individual savings accounts or ISAs could ensure that the money earned is not subjected to net income tax and capital gains tax.

Tax Credits

You can also invest in mutual funds or pensions which can help you to cut your tax bill.

Child Benefit and the 40 Tax Bracket.

You also pay the high-income child benefit charge in case you have a yearly income of above £50,000, plus receive child benefit.

Example:

Assuming that you earn £55,000 and have child benefit. You have to pay some of it back with self-judging. The benefit is recovered by £60,000.

When this charge is added to £50,000-£60,000, your effective marginal rate can be more than 50%.

This cross ring with the 40 tax bracket 2025 gives even more importance to tax planning.

Dividend Income and 40 Tax Bracket.

The taxation on dividend income is different as compared to salary. Under 40 income tax bracket, the after dividend allowance dividend tax is 33.75%.

Example:

When you earn £5,000 in dividends and you are already on the 40 tax bracket, a big percentage of your dividend will be taxed at 33.75%.

This is one of the factors that business owners have to take into account when making the choice between the dividends and the salary.

The Higher Rate Taxpayers and Capital Gains Taxpayers.

Capital Gains Tax is also dependent on your income band.

Assuming that you are in the 40% tax bracket:

- Property gains are taxed at 28%.

- Other gains are taxed at 20%.

Example:

Assuming that you are a higher-rate taxpayer and sell shares of a £20,000 gain, you can pay tax on the excess of the allowance at 20%.

Does Everyone Pay the same 40 Tax-Bracket 2025?

In the UK, not all people are subjected to the same tax bracket of 40%. The taxes depend on the total income, deductions, and personal allowances. They also rely on the regional regulations. The 40 tax bracket is 2025-2026 and is applicable to England, Wales and Northern Ireland according to HMRC rules.

Scotland and the Higher Rate

Scotland has various rates and levels. They possess less regressive 6 bands of taxation.

Example:

A Scottish taxpayer may enter their higher rate tax band at a lower income level than someone in England.

While the structure is still progressive, the specific figures differ. Always check the regional rules.

Conclusion

The 40% tax bracket is a progressive tax measure aimed at bringing high earners under a fair tax system. For many, it may seem intimidating, but once you know how it works, it becomes easy to deal with.

The key things to remember:

- You only pay 40% on the portion above the threshold.

- The 40 tax bracket 2025 still begins at £50,271.

- Smart planning can significantly reduce your real tax bill.

Pension contributions, salary sacrifice schemes, dividend planning, and proper structuring can all make a major difference. Small adjustments can legally save thousands over time.

That’s where we come in. At Sterling Cooper, we help individuals and business owners navigate the 40 income tax bracket with clarity and precision. Contact us now to turn your tax planning from a burden into an advantage.

Want to reduce what you pay in the 40 tax bracket and keep more of what you earn?

Speak to our taxation services today and get a clear, practical tax plan tailored to your income.

FAQs

The 40 tax bracket is the higher rate of income tax in the UK. You pay 40% tax on income between £50,271 and £125,140 (based on the 40 tax bracket 2025 rules).

The 40 tax bracket starts once your taxable income goes above £50,270. Only the portion above that threshold is taxed at 40%.

You pay 40% only on the income within the higher rate band. It does not apply to your full salary, just the part above the basic rate limit.

Yes. Pension Contributions, Salary Sacrifice Schemes, and Gift Aid Donations can reduce your taxable income and lower how much falls into the 40 tax bracket.

It applies in England, Wales, and Northern Ireland. Scotland has different income tax bands and rates.

Recent Posts

What Are the Best Budgeting Strategies for Young Professionals?

February 17, 2026

What Are the Benefits of Automated Payroll Processing?

February 16, 2026