Posted by:

Admin

Date:

February 27, 2026

Category:

blogs

Understanding s455 Tax: When HMRC Taxes Your Company Loans

Did you ever consider borrowing money from your own company, hoping to pay it off without any trouble? In case you borrow as a private business, and you fail to pay it within nine months, your company will be liable to S455 tax.

The S455 tax, as of 2026, is 33.75% of the remaining loan balance. The company is liable to payment of this tax to the HMRC. This tax aims to prevent company owners from avoiding personal tax through company loans. It is the reason it has this tax and every director must know how it operates before withdrawing money in their business.

What Is S455 Tax?

S455 tax is a transitional tax that an individual is charged in case a director or shareholder obtains money borrowed out of his company and fails to repay it within the required time. The charge is not charged on an individual but on the company in the case of the loan taken by the director.

The tax is applicable in case loans are extended to the participators. A participator is normally a shareholder or a person who possesses control of the firm. This normally translates into directors who are also shareholders in the business.

When you are a director and shareholder, and you borrow money out of your company, S455 corporate tax may take effect. Whether it was a formal or informal loan does not matter. Even personal bank money obtained casually and not in the form of salary or dividends can be considered a director loan.

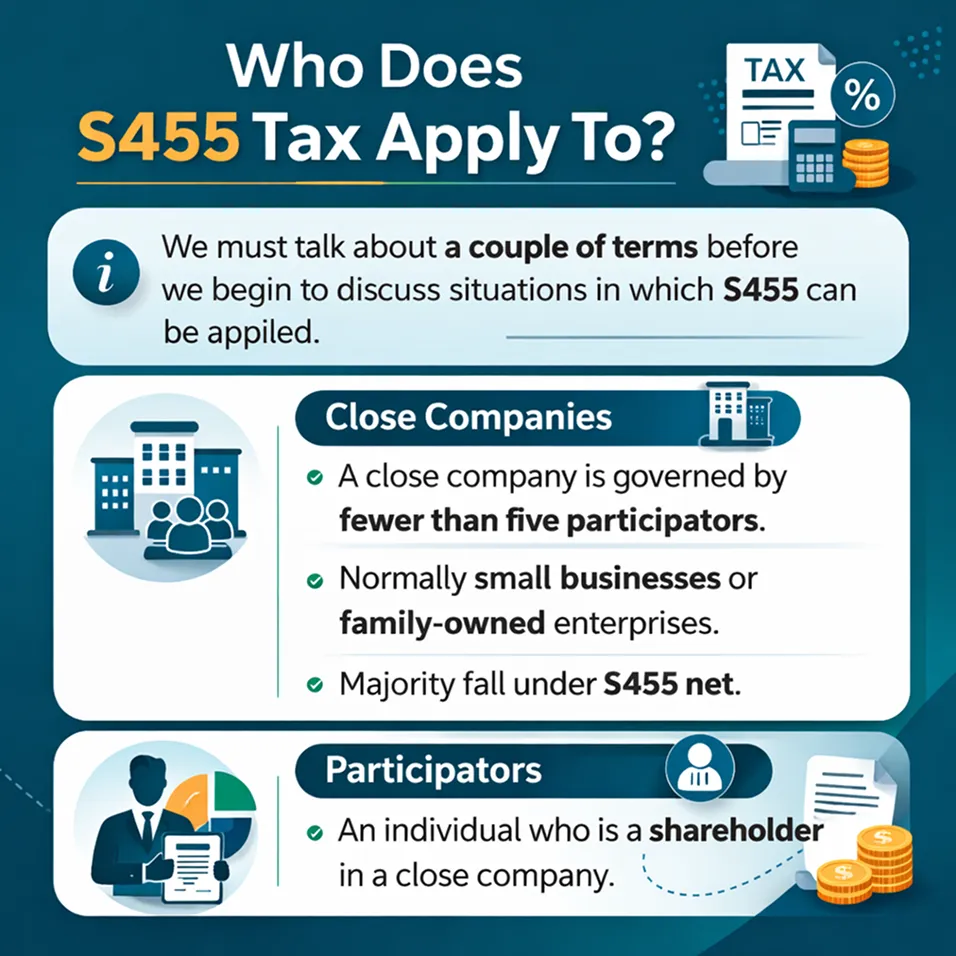

Who Does S455 Tax Apply To?

We must talk about a couple of terms before we begin to discuss situations in which S455 can be applied.

- Close companies: A close company according to the Corporation Tax Act 2010 is a company that is governed by fewer than five participators. These are normally small businesses or family owned enterprises. The majority of these corporations fall under S455 net.

- Participators: A participator is a person who is a shareholder in a close company.

S455 may apply in case a participator is borrowing the loan from the close company. Whether the loan was a formal or an informal loan is irrelevant. Even the money exchanged casually with your personal bank account can be considered as a director loan unless it is salary or a dividend.

When Is S455 Tax Due?

The question that many directors ask is when does S455 corporate tax become due. Rules of timing are quite strict and have to be followed. The loan should be repaid within a period of nine months and one day once the accounting period of the company is over.

In case the loan remains unpaid after the deadline, the tax is due. It is paid along with Corporation Tax of the company. This implies that it has to be paid between nine months and one day since the accounting year is complete. You may be subject to penalties if you fail to do so.

To learn more, check out our guide on late tax penalties and how to avoid them.

As an illustration, assume that your firm has an end of year date of 31 March 2025. The last date of repayment would be 1 January 2026. At the end of that date, when the loan is not cleared, S455 is imposed, and must be paid to HMRC.

S455 Tax Rates Explained

The rates of S455 corporate tax will have to be understood since the percentage will be substantial. The prevailing rate is 33.75 percent of the outstanding balance on the loan. This rate is equivalent to the increased rate of dividend tax which eliminates the tax benefit of borrowing rather than making dividend declaration.

In the instance below, when a director owes such sum to the company as £30,000 at the deadline, the charge on s455 would be 33.75% of such sum. That is equal to £10,125, which the company will be paying to HMRC. This is a huge sum of money that may have an effect on the cash flow of the business.

The regular rates are very high and hence the advice of most accountants is that directors need to repay the loans way ahead of the due time. The tax is technically a temporary one but the money can be locked away for years before it is returned.

Why S455 Tax Exists

To deter tax avoidance, the government came up with the S455 tax. In its absence, directors are likely to borrow big amounts of money within their company rather than dividend. They would be able to postpone the payment of personal tax over a long period of time and this would lower the government taxes.

HMRC erases that benefit by levying S455 corporate tax. In the case you do not pay the loan, the company pays a tax which is like the tax you would have paid on a dividend had you paid the loan. This makes the tax system just to all.

Simply put, S455 tax prevents individuals from using company loans in order to avoid or defer tax. It promotes the right practices of paying like salary using PAYE or reported dividends.

How Director’s Loans Work

A loan between a company and its director occurs when funds are transferred between the company and the director other than as payroll or dividend. In case the company owes you money, no tax is applied. But when you are owed money to the company, then that gives a director a loan balance.

Any company is supposed to have a Director Loan Account (DLA). It is an account that documents the amount of money borrowed or paid. It is similar to running total in that it indicates whether the director is in debt to the company or vice versa.

One of the key reasons why S455 tax issues occur is because of poor record-keeping. Unless accounts are regularly updated, the directors might not be aware of having such a large outstanding balance.

What Happens After Repayment of the Loan?

The positive thing is that the S455 tax is short-lived. In case the loan is finally re-paid, the company is able to claim tax paid. This is referred to as reclaiming the S455 corporate tax.

Nonetheless, the refund is not immediate. The guidelines have waiting times that might postpone the refund of the money. This implies that the funds of the company may take a long time before being refunded to HMRC.

Even though the reclaiming is feasible, it is much more preferable not to avoid the charge at all. It is always better said than done.

Reclaiming S455 Tax: How It Works

The question many directors will pose is how it is possible to recover S455 tax after payment of it. Once the loan has been repaid, the company will be entitled to receive the S455 corporate tax refund. Nevertheless, this assertion cannot be done immediately after repaying.

You should wait a period of nine months and one day following the date that the accounting period of repayment of the loan ended. This is when it can reclaim tax on a formal basis. The delay is usually unexpected by the directors who are eager to get back their money fast.

To illustrate, when the firm paid S455 corporate tax in the year 2026, and the loan was repaid in 2027, the tax refund claim may not be filed until 2028. That implies that the cash may be tied up for several years.

How to Reclaim S455 Tax Stepwise.

When reclaiming S455 tax, a number of steps are used. First, you should make sure that the loan is completely paid and that it is duly carried in the books of the company. To have a successful claim, there must be clear documentation.

Then draw revised financial statements of the repayment. The amended Corporation Tax return or a given form of claim may have to be offered to HMRC by the firm itself. This part will be normally performed by your accountant.

Last but not least, file the claim and await HMRC to make the tax refund. It is the company, and not the director himself, that is paid a refund. Good record keeping simplifies the process of reclaiming the tax.

The 30-Day Rule and Anti-Avoidance Rules.

HMRC has also provided regulations to ensure that the directors are not able to repay loans on a temporary basis and take a loan very soon. This is referred to as bed and breakfasting. This was previously used to evade the S455 corporate tax.

HMRC may disregard repayment of the amount £5,000 or more repaid by a director, and re-borrowed within a period of 30 days. That is where tax is applicable. This regulation avoids the manipulation of the time of repayment.

These anti avoidance measures demonstrate that HMRC is extremely attentive to directors’ loans. Attempting to fool the system will mostly result in reprimand and further investigation.

Common Mistakes Made by the Directors.

There are numerous directors who activate S455 corporate tax unintentionally. This is an easy mistake to make because the Director does not check the Account of Loan to him regularly. Small withdrawals will accumulate to big balances in the long run.

The other error will be the confusion between dividends and loans. Without appropriate declaration of dividends by way of board minutes and paperwork, withdrawals will be considered as loans by HMRC. This may suddenly cause taxation.

Lastly, there are directors who lose sight of the 9 month deadline. The failure to make the date puts an automatic charge on the tax although the repayment can be made later.

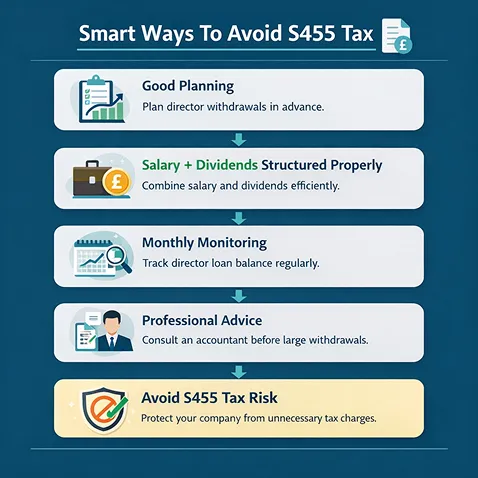

Smart Ways To Avoid S455 Tax

Maximising the way to evade the S455 corporate tax is through planning. Automatically paying yourself a structured salary under the PAYE will take care of taxes. Dividends should be declared in the right way, official paperwork will also help avoid confusion.

It is necessary to have regular bookkeeping and review of the Director Loan Account on a monthly basis. Balancing at all times will ensure that you work to meet deadlines. There is less risk of errors because of clear communication with your accountant.

When there is a lack of cash flow, then consult an expert before borrowing huge amounts. Several minutes of a conversation will save many years of delayed refunds and unnecessary stress.

Related: Top Tax Saving Tips.

Conclusion

S455 tax is paid in cases where directors leave loans beyond the limits without any payment. The existing tax rates are at 33.75 and that may be a big source of cash flow strain. The waiting time of tax refund can be quite frustrating, though it can be recovered.

The knowledge of what S455 tax is, when it is due and how to reclaim it gives you the control of business finances in your hands. At Sterling Cooper Consultants, we understand that rules can be perceived to be strict but they are meant to ensure that there is fairness in the tax system. S455 corporate tax could be avoided with due planning and awareness.

Knowing tax rules secures the cash flow. Contact us now to make better decisions for the future of your company.

Worried about triggering S455 tax or waiting years for an S455 tax refund?

Our tax specialists can review your Director’s Loan Account, calculate exposure, and help you stay compliant before deadlines hit.

Get in touch with our taxation services today and protect your company’s cash flow before S455 tax becomes an expensive surprise.

FAQs

s455 tax is a temporary Corporation Tax charge applied when a director or shareholder owes money to their company and does not repay it within nine months and one day after the accounting year end. It exists to prevent tax avoidance by discouraging long-term company loans instead of dividends.

s455 tax is due nine months and one day after the end of the company’s accounting period if the loan remains unpaid. It is paid alongside the company’s Corporation Tax bill.

The current s455 tax rates are 33.75% of the outstanding loan balance. This rate aligns with the higher dividend tax rate to remove any financial advantage from borrowing instead of taking dividends.

Reclaiming s455 tax is possible once the loan has been fully repaid. However, the company must wait nine months and one day after the end of the accounting period in which repayment occurred before claiming the s455 tax refund from HMRC.

The s455 tax refund is paid back to the company, not the individual director. The company must submit the appropriate claim to HMRC to recover the amount previously paid.

Recent Posts

Understanding the 40% Tax Bracket in the UK

February 25, 2026

A Complete Guide to Wealth Tax in the UK

February 24, 2026