Posted by:

Admin

Date:

June 29, 2026

Category:

blogs

Monthly Management Accounts Checklist: Everything Your Business Needs to Stay on Track

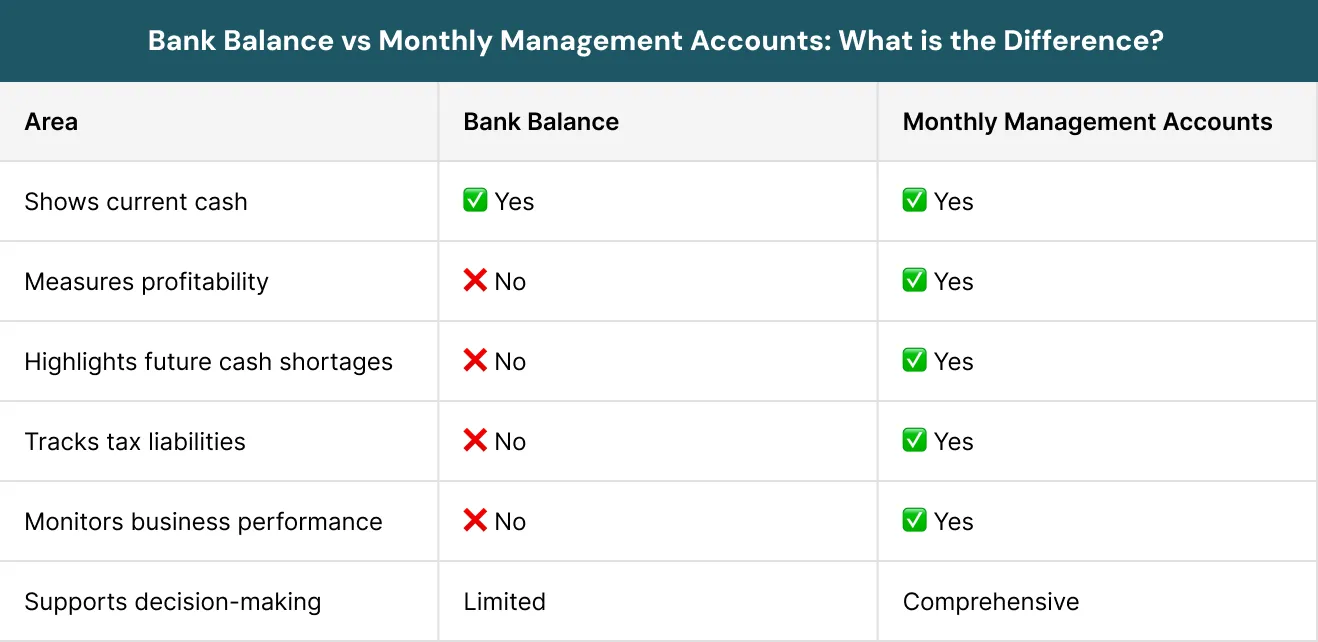

Many business owners rely on the bank balance as their measure of financial health, but it is one of the least reliable ways to measure how a business is truly doing. The bank balance tells you what cash is sitting in your account right now. It says nothing about whether you are profitable, whether a big tax bill is coming or whether a supplier is quietly squeezing your margins.

In fact, three in five UK small businesses have experienced cash flow problems yet most only review their finances once a year at filing time. By then, it is too late to act. Monthly management accounts change that by giving you a clear, structured view of how your business is truly performing, not just a snapshot of today’s cash.

If you have ever wondered what management accounts are and why so many growing businesses rely on them, the short answer is this: they help you make better decisions, avoid nasty surprises and stay in control of your finances throughout the year.

Key Takeaways

- Monthly management accounts provide a clear view of profitability, cash flow and business performance, helping you make informed decisions throughout the year rather than relying on year-end accounts alone

- If you have ever wondered what management accounts are, they are regular financial reports that typically include a Profit and Loss statement, Balance Sheet and key performance indicators (KPIs) used to monitor business health

- Effective accounts management helps identify risks early, including cash flow shortages, declining margins, tax liabilities and overtrading before they become serious problems

- Understanding how to do monthly management accounts starts with a structured process that includes bank reconciliations, financial reporting, cash flow forecasting and KPI tracking

- Knowing how to prepare monthly management accounts also means reviewing aged debtors and creditors, monitoring tax obligations and documenting key financial movements and variances

- Tracking a small number of meaningful KPIs, such as gross margin, debtor days and payroll as a percentage of revenue, often provides more value than measuring dozens of metrics with no clear action plan

- Consistent monthly reporting enables stronger budgeting, forecasting and business planning while giving lenders, investors and stakeholders greater confidence in your financial management

What Are Management Accounts and Why Are They Important?

Management accounts are financial reports produced for business owners, directors and senior managers. They are usually prepared quarterly or monthly and typically include a Profit and Loss report and a Balance Sheet. Unlike your statutory year end accounts which look backwards and are primarily for HMRC and Companies House, accounts management is designed to help you steer the business right now.

Did You Know?

A profitable business can still run out of cash if customers pay late.

Think of it like driving a car. Your statutory accounts tell you where you have been. Your monthly management accounts tell you where you are going, how fast and whether there is something in the road ahead.

Done well, they reduce surprises. They improve conversations about pricing, costs, cash and tax. They help you catch problems early before a small dip in margin turns into a serious cash crisis. Many small business owners only look at their numbers once a year at filing time. By then, it is too late to change anything. Monthly management accounts put you ahead of problems and give you time to act.

Who Should Be Using Monthly Management Accounts?

There is a common misconception that accounts management is only for large companies with finance teams. That is not true. Businesses of all sizes benefit from them.

Small business owners use them to stay in control of their numbers. Accountants use them to give real time advice rather than reflecting on what happened twelve months ago. Banks and investors ask for them because they show that a business is well run and financially healthy. Freelancers and sole traders can also benefit from monthly management accounts. A simple monthly management accounts summary helps you see which clients or services are most profitable and which ones are not worth the effort.

In the UK, 98% of businesses have 20 or fewer staff members, yet only a small fraction of these have any form of regular accounts management in place. That is a significant gap. If you want to know where you stand financially and make decisions based on facts rather than intuition, monthly management accounts are worth the effort irrespective of your size.

What Are the Benefits of Monthly Management Accounts?

Before diving into the checklist itself, it is worth understanding what you actually get from putting this process in place. The benefits go well beyond simply knowing your numbers.

1. Better Decision-Making

When you face an important business decision like hiring someone new, dropping a product line or investing in equipment then you need an accurate and recent snapshot of your financial position. Making major decisions without that information is risky. Monthly management accounts give you the data to back your choices with confidence rather than hope.

A good example is of an estate agency with three offices asking the owners to rank the branches by profitability. They gave their best guess. When there is proper accounts management, the ranking was completely different from what they had assumed. They had been making resourcing decisions based on entirely wrong information.

2. Future Planning

Robust monthly figures are invaluable for planning. Whether you are seeking investment, applying for a bank loan, budgeting for the year ahead or forecasting future performance, accounts management provides the foundation. Banks and investors would like to see an accurate financial overview before they commit. Internally, your monthly management accounts help you plan hiring, capital expenditure and operational activities with realistic expectations rather than wishful thinking.

3. Cost Control

Monthly management accounts give you clear visibility into both income and outgoings. You can see exactly where the company’s money is going and whether it is being spent wisely. This level of detail helps you identify areas where costs are creeping up, challenge spending that is not delivering value and make more informed choices about where to allocate your resources.

4. Stronger Year-End Position

When you track your monthly management accounts throughout the year, year-end holds no surprises. You will not receive an unexpected tax bill you cannot cover, nor will you celebrate a good year while quietly panicking about what it means for your tax position. Your records will be up to date, your accountant will have better information to work with and the whole year-end process will be faster, smoother and less expensive.

5. VAT and Compliance Protection

Monthly management accounts help you keep track of your rolling VATable sales, VAT threshold and registration requirements. If your taxable turnover is approaching the VAT registration threshold, you will know well in advance rather than discovering you should have registered months ago and now face penalties. The same applies to PAYE and other compliance obligations. Staying on top of these monthly management accounts removes the risk of costly surprises.

6. Avoiding Overtrading

One of the less obvious but very serious risks for growing businesses is overtrading and expanding sales so quickly that the business runs out of money before customers pay. Suppliers and staff demand payment on time, but customers may not have settled their invoices yet. This is a common cause of business failure and almost always comes as a shock to the owner. Monthly management accounts highlight the risk early so that corrective action can be taken before it is too late.

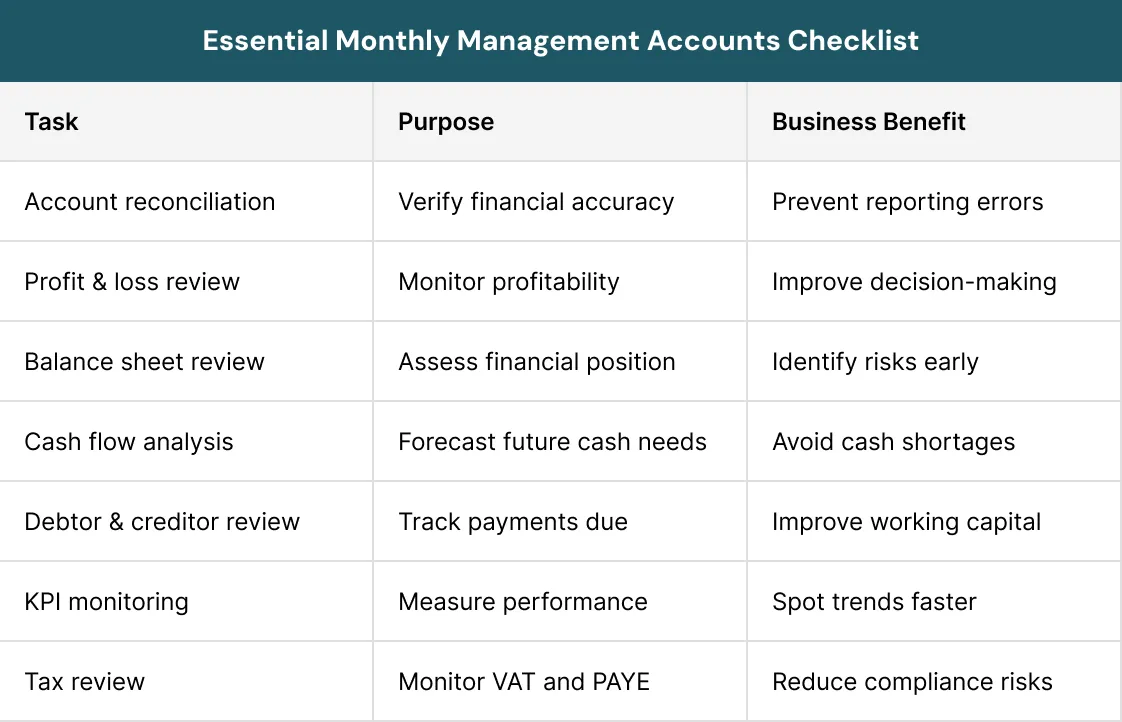

What Does a Monthly Management Accounts Checklist Include?

A good monthly management accounts checklist brings structure to your month end process. It ensures nothing is missed, your records are accurate and your reports are ready in time to be useful. Here is what a thorough checklist should cover.

1. Account Reconciliation

This is the starting point. Compare your bank and credit card statements to your internal records and identify any discrepancies. A bank reconciliation is absolutely essential and you must be able to prove that the numbers match. Without it, every report you produce could be based on incorrect data, which means every decision you make from those reports could be wrong.

Also reconcile your VAT and PAYE accounts. These are often skipped, but they matter. Using VAT or PAYE funds to cover day to day trading is one of the clearest warning signs that a business is in financial difficulty.

2. Profit and Loss Statement

Prepare a Profit and Loss (P&L) statement for the month and for the year to date. Comparisons should be made on the basis of budgets and actuals of the previous year. This allows you to to identify the variances and raise the relevant questions, like:

- What caused the increase in expenses?

- What caused the short-fall in revenues?

- What must change next month?

The P&L tells you whether the business is making money and where that money is going. It is not the same as a cash report. Profit and cash are different things and confusing the two is one of the most common financial mistakes small business owners make.

3. Balance Sheet Review

The balance sheet shows what your business owns and owes at a point in time. Review your assets, liabilities and equity each month. Pay particular attention to movements on key accounts such as debtors, creditors and any director loan accounts.

The balance sheet is a health check for your overall financial position. It tells you whether you are solvent, whether liabilities are growing and whether the business has the financial stability to keep trading and investing.

4. Cash Flow Analysis

Even profitable businesses can run into serious trouble if cash flow is tight. Review cash inflows and outflows for the month and update your rolling cash flow forecast. Ideally, this forecast should look at least 12 months ahead, with 24 months considered good practice. Ask yourself:

- What will cash look like over the next 30 to 90 days if nothing changes?

- Are there large payments coming up like VAT, payroll, loan repayments that need to be planned for?

Spotting a potential shortfall two months in advance gives you time to act. Spotting it when the account is empty does not. 90% of UK businesses faced late payments in 2025, with the average payment delay standing at 32 days.

Quick Tip:

One late-paying customer can create a cash flow problem for an otherwise healthy business.

5. Aged Debtor and Creditor Reports

Pull an aged debtor report and review any invoices that are outside your payment terms. Slow paying customers are a major cause of cash flow problems and the longer you leave a debt, the harder it becomes to collect.

Similarly, review your creditor position. If you are stretching supplier payments to manage cash, this is a risk that needs to be visible and monitored. Where any assumptions are made about stretching creditors, note them clearly in your accounts.

6. Key Performance Indicators (KPIs)

KPIs give you a quick view of how the business is performing without needing to dig through every line of the accounts. The right KPIs depend on your business, but the most commonly useful ones include:

- Gross margin percentage and trends by product or service line

- Debtor days and the proportion of invoices outside terms

- Payroll as a percentage of revenue

- Revenue per employee

- Overheads run rate

- Order book, pipeline coverage and conversion rates

- EBITDA

The goal is not to track everything. The goal is to track the signals that make you act. Agree which KPIs matter for your business and keep them consistent for at least six months so that trends become visible.

7. Tax Obligations Review

Check that all tax liabilities like VAT, PAYE and Corporation Tax are accurately calculated and scheduled for payment. One practical step is to create a dedicated tax reserve line in your accounts so that these funds are not accidentally spent on day to day operations.

If your business has loan covenants, review compliance as part of this step. Report on both actual and forecast covenant compliance. A breach can have serious consequences, including the lender demanding full repayment, so early visibility is critical.

8. Document Revisions

Update all financial documents and records with the latest information. This keeps your records audit ready and ensures that anyone reviewing the accounts, whether internally or externally is working from accurate and current data. If your accounting treatment differs in any way from your year end policies, the document explains this clearly.

9. Management Review and Action Planning

The numbers alone do not run your business. What matters is what you do with them. Bring key stakeholders together to review the management accounts each month. Use the session to ask the right questions:

- What changed this month and what is driving it?

- Which customers or products are most and least profitable?

- Where are we exposed to a single point of failure; one customer, one supplier or one key person?

- What is the one decision we should make this month to reduce risk or improve results?

Add a one page action log with named owners and due dates. Without accountability, reviews become a talking shop.

Which KPIs Should You Be Tracking?

Different sectors have different drivers, but some KPIs repeatedly predict problems or opportunities across most business types. Gross margin is one of the most important. Most businesses do not track it closely, but it deserves serious attention.

On annual sales of £500,000, a 1% improvement in gross margin adds £5,000 to net profit. A 10% improvement in margin delivers the same profit impact as a 10% increase in sales often with far less effort. Tracking margin trends month by month, broken down by product or service line where possible, gives you the insight to take action before profitability erodes.

Interesting Fact:

A small increase in gross margin often boosts profit more than a similar increase in sales.

How Do You Know If Your Margins Are Healthy?

Here is a simple example. Suppose you sell a product for £10 with a gross margin of 25%. If you cut your price by 10% to win more sales, you need to sell 66% more units just to make the same profit. If instead you raise the price by £1, you can sell almost 30% fewer units and still come out ahead. Many business owners instinctively reach for price cuts when sales slow down. Monthly management accounts help you see whether that is actually the right move or whether a price increase would serve you better.

What Should the Monthly Commentary Include?

Numbers tell part of the story. Commentary tells the rest. A good management accounts commentary does not need to be long, but it does need to be clear. Avoid lengthy blocks of text, unexplained jargon and relying entirely on graphs without explanation.

A useful commentary explains what changed and why, highlights key variances against budget and prior year and sets out any risks or issues that need attention. Where there is significant uncertainty about the year end position, set out a range of scenarios, best case, worst case and base case so that decision makers can plan accordingly.

A short one to two page summary at the front of the pack, covering the main points in plain English, is often the most effective approach.

How Often Should You Produce Management Accounts?

Monthly management accounts are the standard for most businesses. Quarterly reporting may work for very small or straightforward operations, but it reduces your ability to catch problems early. Management accounts should be available within 15 working days of the month end. The longer you wait, the less useful they become. Stale information does not help you make timely decisions.

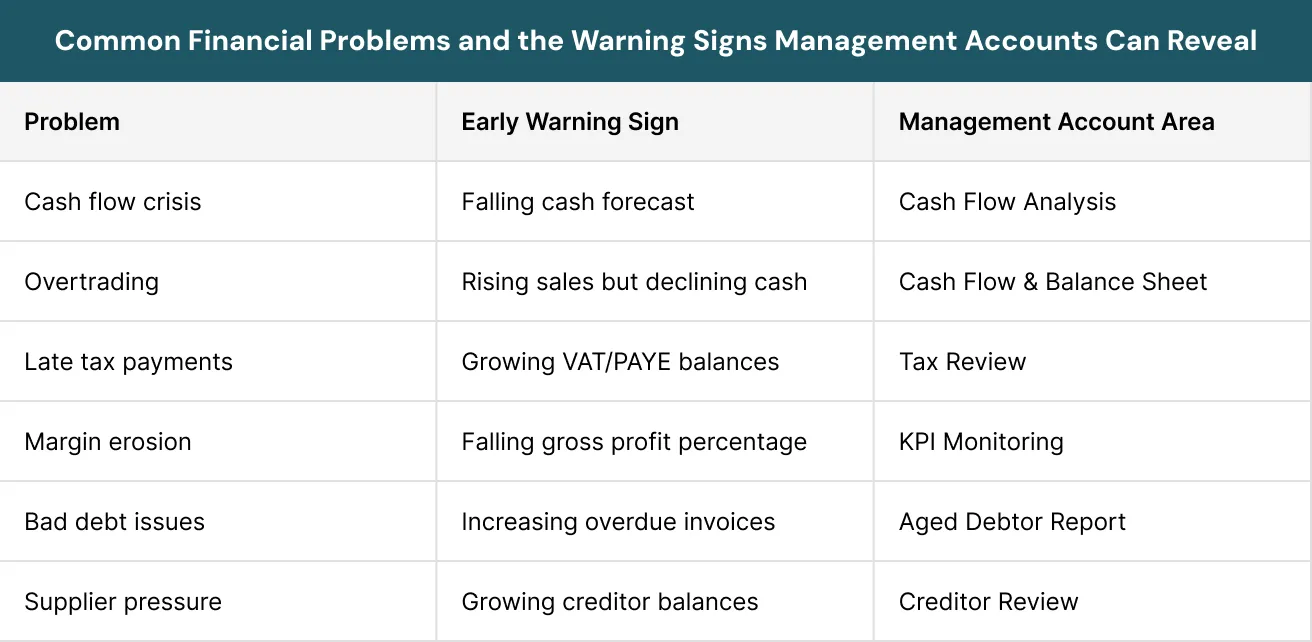

What Happens When You Skip the Checklist?

Without a structured monthly process, businesses end up making financial decisions in the dark. They do not know their true profitability, which parts of the business are performing or what cash will look like in six weeks.

One particularly dangerous outcome is overtrading where a business expands sales too quickly and runs out of money before customers pay. This is a common cause of business failure and almost always comes as a shock to the owner. Regular accounts management would have flagged the risk early enough to act.

How Does Accounts Management Help You Plan for the Future?

Regular accounts management supports every aspect of business planning. Banks and investors will ask for management accounts before agreeing to fund or invest. Having up to date, professional reports demonstrates that your business is well managed and financially credible.

Internally, your monthly figures provide a reliable basis for budgeting, forecasting and operational decisions such as hiring or capital investment. They also put you in a stronger position at year end.

When you have been tracking your finances throughout the year, there are no surprises. Tax planning is easier, your accountant has better information to work with and the year end process costs less time and money.

What are the Practical Steps to Get Your Monthly Reporting Right?

If your current reporting is inconsistent or late, start simple and build from there. The key is consistency. Here is how to set yourself up properly:

- Agree a monthly management accounts closing date and stick to it

- Document your month end process clearly so nothing is missed

- Agree which KPIs matter and keep them stable for at least six months

- Create a tax reserve line so VAT, PAYE and Corporation Tax are never accidentally spent

- Add a one page action log with owners and deadlines to every monthly management accounts review

- Use accounting software such as Xero or QuickBooks to automate as much as possible

- Work with an accountant who can fine tune your reports, highlight what matters and explain what the numbers actually mean

Monthly management accounts are not a luxury reserved for large businesses. They are a practical tool that any business can use to understand its finances, make smarter decisions and plan for sustainable growth. The businesses that use them consistently are the ones that spot problems early, seize opportunities quickly and build on solid financial foundations.

Read more about sustainable growth: Accounting Practices for Sustainable Growth

Real Life Example

A UK-based construction firm managed to increase its annual sales turnover from £700,000 to £5 million within a short time period. From an accounting perspective, the company seemed to be extremely successful. But it faced a very serious cash flow problem due to the considerable period between project completion and customer payments.

During this time, the firm continued to incur liabilities in the form of outstanding supplier invoices, wages to its own workers and subcontractor invoices. Finally, it ran out of overdraft facilities and found it hard to cover its financial commitments. It turned out that overtrading was the reason for all the problems that the company encountered. Although the contracts were profitable, the firm did not have enough working capital for further expansion.

This particular case shows precisely how monthly cash flow forecasting and balance sheets could detect the arising problems. Companies can take appropriate measures well before they get into serious trouble.

Never take your eye off the cash flow because it’s the lifeblood of business. – Sir Richard Branson, Founder of Virgin Group.

Conclusion

Running a business without monthly management accounts is like flying blind. You might feel like things are going well based on what is in the bank or how busy the team seems, but without the full picture, you leave the business exposed to risks that could have been spotted and addressed far sooner.

A structured monthly management accounts checklist gives you control. It ensures:

- Your records are accurate

- Your cash flow is visible

- Your margins are tracked

- Your decisions are based on real information rather than assumptions.

It keeps tax obligations in check, flags problems early and puts you in a strong position whether you are seeking funding from your bank, planning next year’s budget or simply trying to understand where your profit is going.

The businesses that thrive are not always the ones with the highest sales. They are the ones that understand their numbers, act on them quickly and build good financial habits from the start. Whether you are a sole trader reviewing a simple monthly management accounts summary or a growing company producing a detailed management pack for your board, the principle is the same; if you can measure it, you can improve it.

Always start with the basics, maintain consistency and consult a good accountant that will be able to interpret all these figures for your next step. Once you have developed a reliable process every month, you will never know how you were running the business before.

Sterling Cooper knows that most business owners do not need financial reports. They need insights that help them make better choices. Our management accounting and business advisory services give you financial information on time including cash flow prediction and performance analysis. Contact us today to keep your business on track and support long term growth.

Are you making business decisions with a full picture of your finances?

Sterling Cooper helps businesses improve cash flow visibility, profitability and financial control through expert management accounting and advisory support. Contact us today to find out how we can help your business grow with confidence.

FAQs

A monthly management account is a set of financial reports prepared each month to help business owners monitor performance, profitability, cash flow and financial health. It typically includes a Profit and Loss statement, Balance Sheet and key performance indicators (KPIs).

Present monthly management accounts in a clear, structured format with a summary of key findings, financial statements, KPI trends and actionable insights. Include comparisons against budgets, previous periods and forecasts to highlight important changes.

Examples of management accounts include Profit and Loss statements, Balance Sheets, cash flow forecasts, aged debtor reports, aged creditor reports, budget variance reports and KPI dashboards.

Account management is the process of monitoring, maintaining and improving financial records, customer accounts or business relationships to support informed decision-making, operational efficiency and long-term growth.

Management accounts are prepared regularly for internal decision-making and business planning, while financial accounts are annual statutory reports prepared primarily for regulators, tax authorities and external stakeholders.

Monthly management accounts should include a Profit and Loss statement, Balance Sheet, cash flow analysis, KPI reporting, aged debtor and creditor reports, tax liabilities review and management commentary explaining key financial trends.

Monthly management accounts help businesses identify financial issues early, improve cash flow management, monitor profitability and make informed decisions based on up-to-date financial data rather than assumptions.