Posted by:

Admin

Date:

January 12, 2026

Category:

blogs

Late Tax Return Penalties: What to Expect and How to Avoid Them

According to the summary of the Self Assessment filing update from HMRC, 10.89 million filers submitted their tax returns on time. This is 90.53% of the expected 12.03 million Self Assessment returns. 0.7 million of the total returns were filed on the last day. The Director General Customer’s Service urged the public to file their tax returns at earliest to avoid late tax return penalties. These penalties may vary in amount based on circumstances and the time period they have been delayed for. Here is a detailed guide on penalties for late tax returns that covers types, amounts, and appeals.

To learn more about the changes and updates in taxation world, check out our guide for 2025-26 tax year updates.

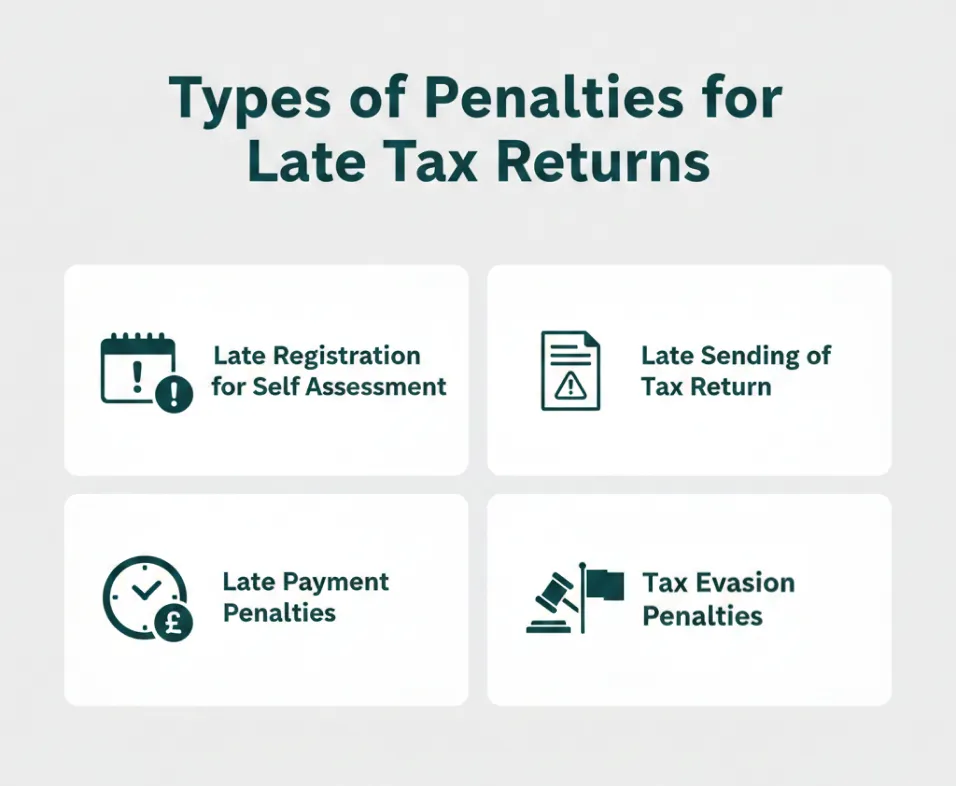

Types for penalties

Following are the types of late tax return penalty.

Late registration for self assessment

You have to register for your Self Assessment by 5th October and pay the tax bill by 31st January. If you do not comply, you’ll receive a late tax return penalty. It is called ‘failure to notify’ penalty.

HMRC tax filing deadline penalty is based on the amount you still owe. In 12 months of HMRC receiving your Self Assessment tax return, this penalty will be issued.

Late sending of tax return

Following are the late tax return penalties on late sending.

| Time | Amount |

|---|---|

| Initial time | £100 |

| 3 months | Additional to £100, £10 per day up to £900 |

| 6 months | A penalty of £300 or 5% of the due tax |

| 12 months | Additional £300 or 5% whichever is greater |

Late Payment

If you pay your tax late, you’ll get penalties. It will be equal to 5% of the unpaid tax and you’ll get it after 30 days, 6 months and 12 months.Tax Evasion Penalties:

HMRC might investigate you for tax evasion if they find you deliberately hiding the tax returns. Tax evasion penalty can be £5,000 or 6 months of jail time.

How to Estimate Your Penalties for Late Filing

The government of the UK, on its website, provides a calculator for estimating your late tax return penalties. This calculator does not consider the following:

- What you’ve paid towards your tax bill

- Any left over penalties or interests from former tax years

- Any credit that you might have from these years

How to pay a Penalty

You can choose from a number of methods. It depends upon the number of days passed after you have received the late tax return penalty.

The day you receive and the next day

On these two days, you can pay via:

- Online banking

- Bank transfer. You can use the Clearing House Automated Payments System (CHAPS) or Faster Payments.

- Debit card or credit card (corporate) online

- Building society or bank

Within 3 working days

In these days, you can pay via:

- Using BACS for Bank transfer

- Sending the Cheque by post

- Direct debit which should have been collaborated with HMRC.

Within 5 working days

You’ll have to pay your late tax return penalties via Direct Debit.

Disagreement with the Penalty

If you disagree with a late tax return penalty, you can file for a review. HMRC will respond to your grievance. They will either amend your penalty or they will uphold the original one. You will have to explain why you disagree with HMRC with a valid excuse.

Which excuses are considered reasonable?

Here are some of the reasons that are classified reasonable.

- Death of someone close (partner or relative) before payment/deadline

- Admission in hospital causing delay of tax affairs

- Any illness that can be life threatening

- Failure of computer/software

- Problems with HMRC online services

- An event of fire, robbery or flooding, causing prevention or delay in filing taxes.

- Delays in postal services beyond your control

- Your disability or mental illness causing delays

- Someone else was supposed to file tax on your behalf but they failed to do so.

- You didn’t understand your legal obligation regarding taxes.

Which excuses are not reasonable?

The following excuses are not considered reasonable by the HMRC:

- Cheque bouncing due to insufficient balance

- Making a mistake

- Getting a reminder from HMRC.

Time period

An appeal to the HMRC can be made within a designated time period, i.e., 30 days. If you do it after that, you’ll have to provide a reason for delay.

Appeal

To appeal the late tax return penalty, you need an appeal form. These are available on the Government of the UK website. If you do not have appeal forms, you have to send a signed letter to HMRC office. This letter to, appeal the tax penalty, should contain:

- Your name

- Your unique taxpayer’s number (UTR) or any other applicable reference number

- Reason for delay

- Relevant dates

Review

If you do not reach an agreement with the HMRC, you can get a review. You can ask for review anytime even when you appeal the tax penalty and it is in process.

For this, write to the HMRC, the same office you sent your appeal to.

How to avoid Late Filing Penalties

To avoid late filing penalties, here are some tips:

Dates to remember

To avoid filing late penalties, here are some of the important dates that you should remember.

1. Online Filing Dates

The deadline is 31st January after the end of the tax year. The tax is also due on the same dates.

2. Filing a paper return Dates

Even though the tax is due on 31st January, the paper return must be filed by 31st October.

3. HMRC Notice

If HMRC sends you a notice to file after 31st October, you have to file and pay tax in 3 months after the notice.

Other tips

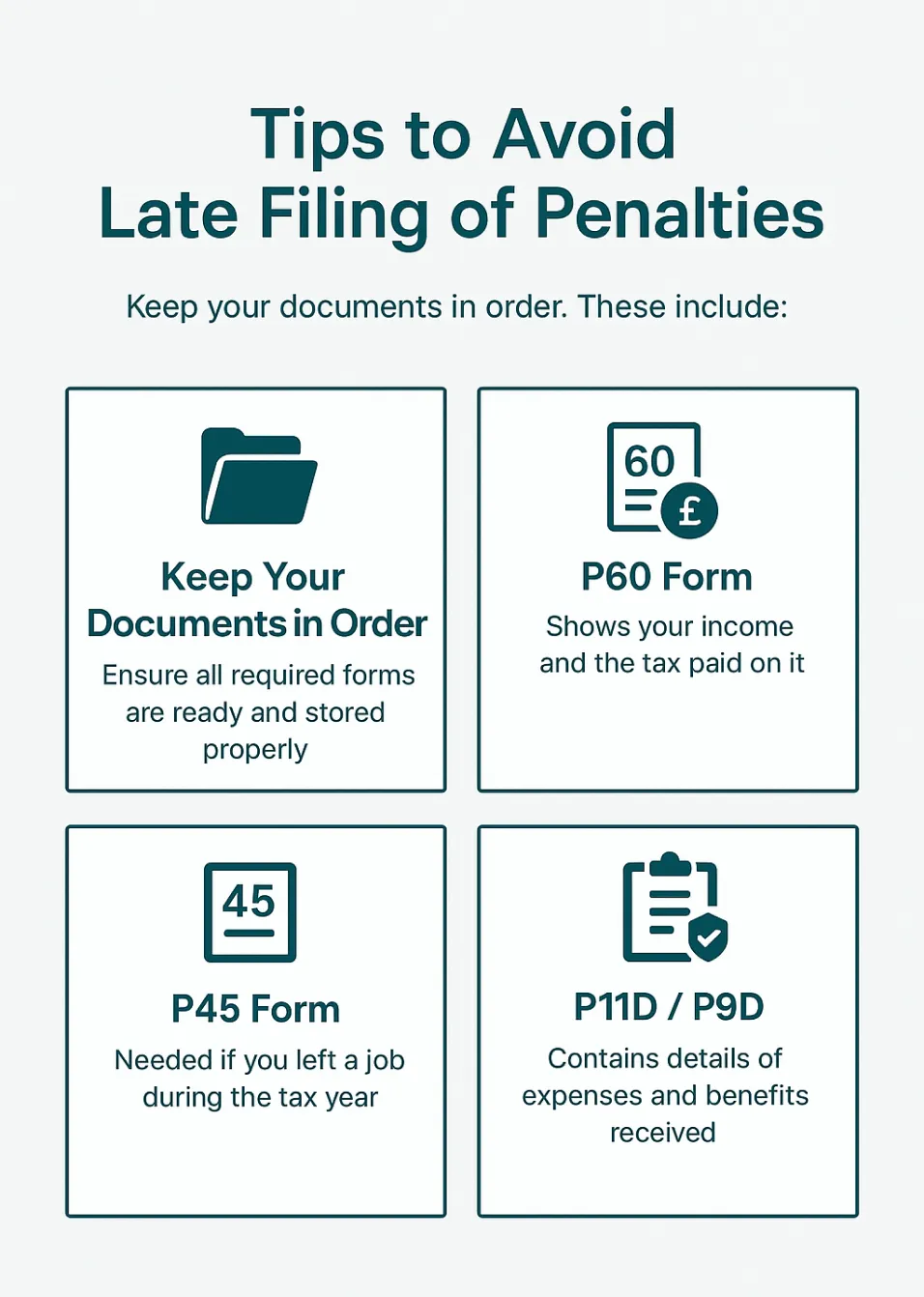

- To avoid late filing of penalties you need to take the following steps:

- Keep your documents in order. These include:

- P60 form: to display income and tax that is paid on it

- P45: if you stopped working your job within tax year, this is applicable

- P11D/P9D: Details of expenses and benefits are contained in this.

- Other receipts, invoices, bank statements

- Keep a record of deadlines.

Get help from a financial advisor. We at Sterling Cooper Consultants, ensure that your taxes are filed and paid correctly and in time.

Our taxation services will ensure that you never receive a late tax return penalty ever again. With us your taxes get done on time, making your finances stress free.

Taxes can be hectic, for you it doesn't have to be.

Contact us now and make sure that you never have to worry about tax penalty ever again.

FAQs

Contact HMRC. They’ll help you choose either of the following options. They can set up a payment plan. Another option is appealing the penalty. You can also request a Time to Pay arrangement.

They’ll assess all your financial documents. All your documents, thus, should comply with regulations. HMRC may also request additional interviews, investigations, etc. Likely outcomes can range from no relief to your penalties to fines and legal action.

Determination is a document containing an estimate of tax you owe. It is made by HMRC if you fail to file a return by the deadlines. The tax shown on this is payable immediately.

Yes they can charge interest on late payments to compensate for the delay you have caused.

Yes, HMRC can agree to withdraw the return. This is possible in case it was issued in error and you did not have the income that should be reported on the return.

BACS stands for Bankers' Automated Clearing Services. It is a UK-based electronic payment system that facilitates direct bank-to-bank transfers. It facilitates important financial transactions such as bill payments, salary transfers, refunds, pension payments, etc.

Recent Posts