Posted by:

Admin

Date:

March 3, 2026

Category:

blogs

What is Capital Allowance? A Simple Guide for UK Businesses

Who knows better than businesses that tax decreases their profit? But many UK firms do not claim the reliefs that could lessen it.

UK businesses claimed £7,000 in tax relief in 2024-25. This shows the extent of capital investment claims made. But many small firms do not take advantage of it.

Capital allowances are a kind of tax reliefs that allow businesses to deduct the cost of business assets from their taxable profit.

In this blog, you’ll learn:

- How do allowances work in Uk?

- What is the capital gains tax allowance?

- What can businesses claim?

- How do capital allowances UK rules apply for the 2025-26 tax year?

- How do they differ from the capital gains tax allowance 2025/26?

What Are Capital Allowances?

These are a type of tax relief. They allow firms to claim back some of the cost of assets they buy for business. This could include tools, kits, vans, or a plant. Instead of cutting the full cost as a normal expense, they claim it over time.

It helps firms invest and grow. When people talk about any type of allowances in the UK, they say how the system works under tax law.

“Our new Constitution is now established, everything seems to promise it will be durable; but, in this world, nothing is certain except death and taxes.”

Benjamin Franklin, Founding Father of the United States

Why Do They Matter for UK Businesses?

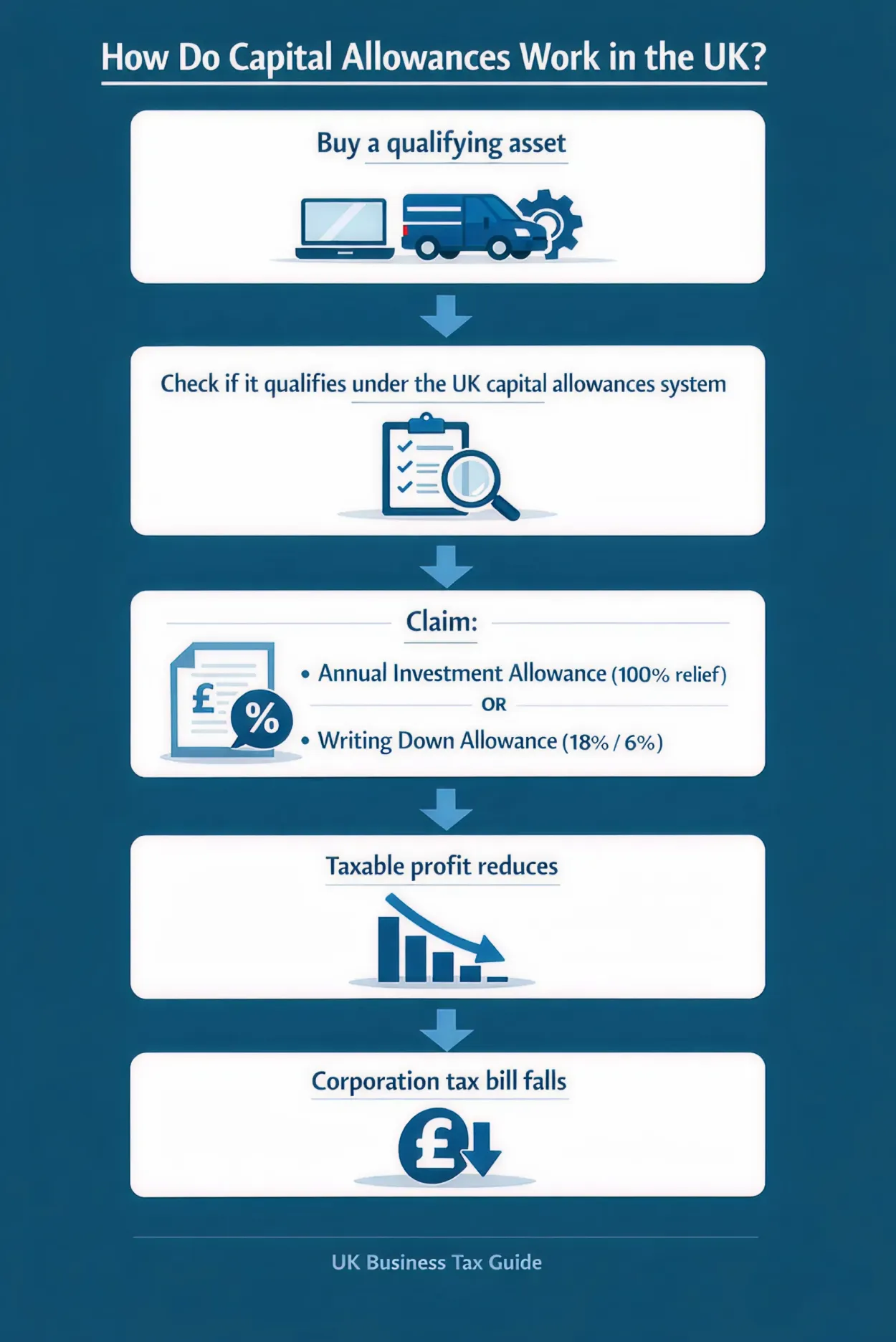

Cash flow is important to run the business. It is a fact that tax reduces profit. These allowances reduce tax when a firms invest in business assets. It means they pay less tax in the claim year.

Over time, this adds up. Many firms in the capital allowances UK system use it to buy tools. It is not only a tax rule. It is a growth tool.

How Do These Allowances Work in the UK?

When firms buy an asset, they cannot always deduct the full cost at once. Instead, they claim capital allowances based on set rates. Some items qualify for full relief in year one. Others go into a pool and get relief bit by bit.

The rate depends on asset type. The taxable profit falls by the amount they claim. The capital allowances system in the UK has set these rates.

What Is the Annual Investment Allowance?

The Annual Investment Allowance (AIA) allows firms to claim full relief on certain types of assets in the year. In this allowance, the UK government sets a limit. If they spend within that limit, they subtract the full cost from profit. This increases cash flow.

What Happens If Firms Spend More Than the AIA Limit?

If companies spend above the AIA limit, the extra amount goes into a pool. They can then claim relief at a set rate each year. This is called the Writing Down Allowance.

The rate can be 18% or 6% depends on asset type. This means firms will not get relief all at once. The structure makes sure large spenders still get relief. It just spreads it out.

How Are Cars Treated Differently?

Cars have different rules. Their rate of relief depends on CO₂ emissions. Cars with low emissions may qualify for higher relief and vice versa.

If a company has a plan to buy fleet cars, these rules matter a lot. So, always check emission bands before you buy.

How Is This Different From Capital Gains Tax?

Capital gains tax is different from this allowance. Capital allowances lower profit when you buy assets. Capital gains tax applies when you sell assets at a profit. They both work differently.

The capital gains tax shows how much gain you can make before tax is due. That rule applies to profit, not business asset relief claims. So do not confuse these allowances with their limits.

Related: How Capital Gains Tax is Changing in April 2026

Do Sole Traders and Limited Companies Both Qualify?

Yes, both can claim capital allowances if they buy assets to run a business. Sole traders claim through their tax return. Limited firms claim through corporation tax.

The relief works similarly for both. However, rates may differ. So the real cash savings may differ. The capital allowances system in the UK covers both.

What Can Firms Claim Under the Rules?

Firms cannot claim all costs. The asset must not be for private use only. It must be for business use. They can claim items like:

- Machinery and plant

- Vehicles

- Kits and tools

- Office new installations

- IT gear and software

They cannot claim relief for:

- Land

- Stocks.

- Homes built for sale

There are clear instructions for what to claim from the capital allowances system in the UK.

What About Full Expensing?

Full expensing is another type of relief for companies. Here’s how it works:

- It allows 100% relief for some plants and machinery.

- It is mainly for limited companies, not sole traders.

- It gives firms a strong reason to invest in new tools.

- It works alongside standard capital allowances.

The main purpose of this relief is to drive growth and boost spending in the UK.

Case Study: How UK Businesses Respond to Capital Allowances

Background

HM Revenue and Customs examined how UK firms make investment decisions in the presence of capital allowances. The study tested whether tax relief affected the timing and spending patterns.

What Businesses Did

Businesses had actedin different ways according to their plans. Like:

- Many firms invested in machinery, equipment, and IT systems.

- Some made planned purchases to claim relief within the same year.

- Some businesses also relied on their advisers to ensure they followed the rules correctly.

Results

The impact of these decisions is very clear. It shows that:

- Capital allowances influence how firms invest.

- Cutting the profit for tax helped businesses start new projects early.

- These are more than tax rules.

It helps businesses to grow faster.

What Common Mistakes Businesses Make?

Businesses make a lot of mistakes. They do not track assets well. Some mix up repairs with their spending. Others forget to claim on time. Some miss small items that still qualify.

Many of them confused these allowances with the capital gains tax allowance 2025/26. They are not linked in purpose or timing. If you miss allowances, you may pay more tax than needed. The UK system works very well, but only if you apply it with care and clean records.

How Can Firms Plan Purchases Smartly?

The firms need to plan their purchases. If they buy assets close to year’s end, they may reduce their taxes sooner and improve cash flow quickly. If they delay the purchase, relief may move to the next year, which can affect their plans.

Capital allowances help sort out tax bills. Many firms do high spending during high profit years. This approach reduces tax when it helps most. The systems work in their favour if they move with plans.

Related: Using Losses to Reduce Your Corporation Tax Bill

What Records Firms Need to Be Kept?

Firms must have clear proof of purchase. This includes:

- Invoices.

- Asset details.

- Payment dates.

- How the asset is used.

They have to show that it supports trade activity. If an item has private use, the claim may be reduced.

Firms need to have proper documentation. Poor records can cause delays or disputes in a tax check. The firm should have a strong and clean record. It protects their claims and peace of mind.

How Do These Allowances Affect Cash Flow?

If the firms saved Tax today, it means they have more money for investment. Capital allowances reduce profit for tax. As a result, the tax bill drops. The saved money can be used for stock and staff. It can also be used for tech or paying off debt. Over time, this improves the firm’s position. Businesses that use the relief well often grow faster. Others miss out. If firms use it within the limits, this relief becomes a lasting cash tool. It is more than a yearly saving.

What Happens When Firms Sell an Asset?

If businesses sell an asset, the outcome of the tax may change. They may face a balancing charge if the sale price is high. They may get extra relief if the sale price is low. This is also possible.

This change relates to their original claim. It is separate from the capital gains tax allowance 2025/26 rules, which apply to gains above a fixed limit. So even when assets are sold, allowances still matter.

How Do Allowances Compare With Other Reliefs?

Capital allowances’ main focus is on spending on assets. Other reliefs may focus on staff training, research, or local growth. Each tax scheme works in a different way.

The system reduces taxable profit from plant and machinery. It does not depend on new ideas like R&D, but relief does. It is not about gains from selling assets. That is what the capital gains tax allowance 2025/26 covers. This is a sort of steady form of tax relief.

When Should Firms Seek Advice?

If firm spend is large or includes mixed-use assets, expert adviceis inevitable. The rules on pooling and rates can be complex to understand. Some firms also discover that they missed them for years.

In some cases, backdated adjustments are allowed. This can bring unexpected savings. A clear expert review canmake sure that claims are accurate and aligned with business goals.

How Do These Allowances Support Long-Term Growth?

This is a matter of fact that growth needs reinvestment. When businesses reduce tax through allowances, they free up working capital. That capital can fund upgradesand tech shifts. It also leads to team expansion. Over time, this compounds.

It is not just a relief. Strong firms use allowances as part of their yearly planning cycles. Within the framework, it is a growth lever that supports scale and resilience.

Final Thoughts

Capital allowances allow firms to reduce tax when they invest in their assets. They improve cash flow and support reinvestment. It also helps firms to improve their financial stability.

They differ from the capital gains tax allowance 2025/26, which applies when gains arise on disposal. The system gives clear guidance, but good planning does better.

Sterling Cooper understands how these allowances can kick in a broader tax plan. We help companies to plan investments according to the law.

To get specific instructions on it or clarity on how they compare with the capital gains tax. Contact us today and let our team support you.

Don’t leave tax relief unclaimed. Tax planning decisions made today can significantly affect your future liabilities.

Our expert team can review your position, optimise your claims, and structure your investments tax-efficiently. Speak to our specialists now and secure the relief your business deserves.

FAQs

Capital allowances are tax reliefs that allow UK businesses to deduct the cost of qualifying assets from taxable profit. Instead of claiming the full cost as a normal expense, the relief is given under specific rules. These rules form part of the capital allowances UK framework.

Sole traders, partnerships, and limited companies can claim capital allowances if they purchase assets for business use. The claim must relate to qualifying expenditure. Private use may reduce the amount claimed.

Common qualifying assets include plant and machinery, vans, tools, office equipment, and certain fixtures. Land and buildings generally do not qualify. The capital allowances uk rules define which assets are eligible.

The Annual Investment Allowance allows businesses to claim 100% tax relief on qualifying assets up to a set annual limit. If expenditure exceeds the limit, the remaining amount is added to a pool and relieved over time.

No. Capital allowances apply when a business purchases qualifying assets. The capital gains tax allowance 2025/26 applies when an individual or business makes a gain on selling an asset. They relate to different tax events.

Yes. By reducing taxable profit, capital allowances reduce the tax payable in a given year. This may increase available cash within the business for reinvestment or operational use.

When an asset is sold, a balancing adjustment may apply. This could increase or decrease taxable profit depending on the sale value compared to its tax value. This adjustment is separate from the capital gains tax allowance 2025/26 rules.

Capital allowances are claimed in the tax year in which qualifying expenditure is incurred. Ongoing claims may apply through writing down allowances in later years, depending on the type of asset and the capital allowances under UK rules.

Recent Posts

Understanding s455 Tax: When HMRC Taxes Your Company Loans

February 27, 2026

Understanding the 40% Tax Bracket in the UK

February 25, 2026