Posted by:

Admin

Date:

January 23, 2026

Category:

blogs

Payroll Compliance: What Every Business Needs to Know

Payroll compliance is the process of ensuring that your employees are paid on time and properly. It also means being compliant with all the UK laws pertaining to this matter. It includes calculations of tax, National Insurance, statutory payments, pensions, and accurate record-keeping. You might think, “Why does it matter?” Well, for one, mistakes can be costly. HMRC expects you to reasonably care in the payroll matters. If you fail to do so, you will get penalties. These can go to 30% of the underpaid amount. The other reason is that if you consistently keep making such mistakes, employees’ trust will actually erode. Thus, complying with payroll is very important. This payroll compliance guide covers everything that you need to know about it.

What is Payroll Compliance?

Payroll compliance means following UK laws when paying employees. It includes registering as an employer with HMRC and reporting wages on time. It also includes paying at least the minimum wage and enrolling eligible staff into workplace pensions. Keeping accurate records and providing payslips along with statutory pay are also part of payroll compliance. Staying compliant is beneficial in multiple ways. You can avoid fines and ensure employees are paid correctly.

Quick legal checklist: What every employer MUST do (short list / TL;DR)

Here is a brief outlook on what a payroll compliance guide may contain:

- Register as an employer with HMRC and set up PAYE.

- Report wages on time using RTI (send an FPS on or before payday).

- Pay at least the correct National Minimum or Living Wage.

- Enrol eligible staff into a workplace pension (employees are 22+ and earn over the threshold)

- Keep accurate employee records.

- Keep payroll records the right way

- Provide payslips

- Pay statutory entitlements (like sick pay and maternity pay).

PAYE & RTI: the reporting backbone

In the UK, PAYE (Pay As You Earn) is the main reporting system. Through this, the employers take tax and National Insurance (NI) from employees’ wages before paying them. The second main system is the RTI (Real Time Information). This is how you report these payments to HMRC. On making a payment to your staff, you have to send a Full Payment Submission (FPS) to HMRC. This is to be done on the payday. For a safety buffer, try sending FPS the day before payroll. These steps are important for payroll compliance.

What an FPS needs to show

At a high level, your FPS must include the following:

- The payroll period (when you paid your staff)

- Employee identifiers (like names and National Insurance numbers)

- Pay amounts

- Tax, NI, and other deductions from Pay

- Any statutory pay (sick pay, maternity/paternity pay, etc.)

Why getting it right matters

It is crucial to get FPS right. If you send it late or with mistakes, you will be in trouble. There are monthly penalties and interest on unpaid tax by the HMRC. Also, you must keep proof of your submitted FPS. This way, you can protect yourself even if there is a question about payment.

How to test your RTI feed

To steer clear, do a test run of your RTI feed. For this, run a test submission to HMRC before your first payroll. Many payroll systems allow this “dry run.” Ensure your software transmits the data accurately. Also, make sure that your employees’ details align with HMRC records.

Common FPS mistakes and how to avoid them

Here are some of the common FPS mistakes that can get you in trouble with the HMRC:

- Wrong employee details

- Incorrect National Insurance numbers

- Missing pay information

- Issues with statutory pay

- Forgetting deductions like student loans or pension contributions

To avoid errors, perform dry runs before actual submissions. Also, check vendor confirmations before you report to the HMRC. Also, perform a very careful review of your employees’ information. For complex RTI issues or tricky payroll situations, it’s wise to speak with a payroll compliance practitioner. They can guide you in detail about your payroll issues. They can also check your submissions and help keep your payroll fully legal.

National Minimum Wage

Paying staff the correct National Minimum Wage (NMW) is a key part of payroll compliance. When applicable, national living wage payment is also a must. The exact rate depends on a worker’s age. It also depends on the fact if they are an apprentice. The NLW applies to adults aged 21 and over. On the other hand, younger staff and apprentices have lower minimum rates. These rates usually change every April. For the latest updates, check the figures on GOV.UK.

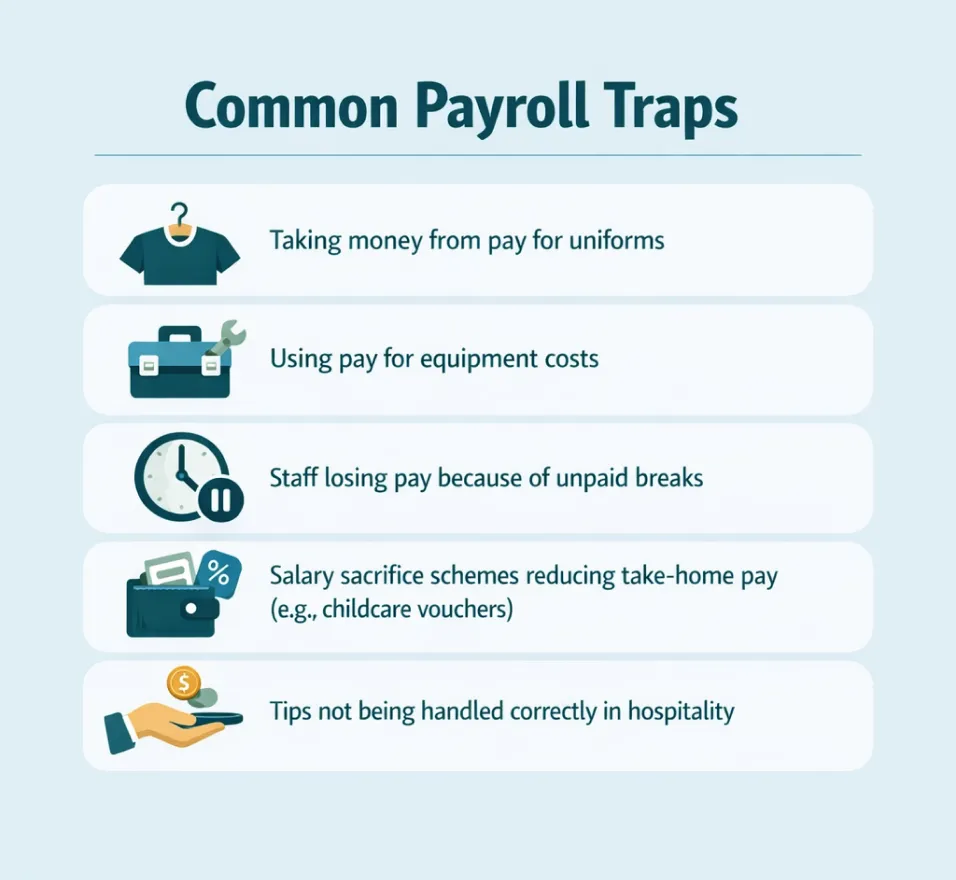

Common payroll traps

Payroll compliance can be tricky. Even well-meaning businesses can fall foul of the rules. They break the rules without meaning to. Common problems include:

- Taking money from pay for uniforms

- Using pay for equipment costs

- Staff losing pay because of unpaid breaks

- Salary sacrifice schemes reducing take-home pay (e.g., childcare vouchers)

- Tips not being handled correctly in sectors like hospitality

The basic rate may be fine, but these conditions can cause the pay to fall below the minimum level.

How to stay on track

The safest way is to run regular reports. They are supposed to calculate staff pay against hours worked. They can also factor in deductions. It’s also a good idea to do regular NMW checks. Paying the right wage is a vital part of payroll compliance. Getting it wrong can lead to fines and bad publicity. Ultimately, it can damage your business.

Statutory pay and family/carer rights

UK law gives employees certain rights to paid or unpaid time off. Some of the conditions are that they are sick, having a baby, adopting, or caring for family members. Payroll compliance includes handling these payments the right way.

Statutory Sick Pay (SSP)

Employees who are off work due to illness may qualify for SSP. This is if they earn at least the lower earnings limit. They also meet the sickness rules. The rate of SSP is reviewed every April. Therefore, employers have to check the GOV.UK “Rates and thresholds for employers” page. Using this information, they have to update payroll before the new tax year begins.

Statutory Parental Pay

Current rates are set by HMRC and also reviewed each April. Usually, employees receive 90% of their average weekly earnings for the first few weeks. It is followed by a fixed weekly rate or 90% of pay (whichever is lower). Here are the two types of parental pay.

- Statutory Maternity Pay (SMP) helps new mothers take time off after the birth or adoption of a child.

- Statutory Paternity Pay (SPP) helps new fathers take time off after the birth or adoption of a child.

Carer’s Leave

This has been in effect from April 2024, under the Carer’s Leave Act 2023. Employees are to get one week of unpaid leave each year to look after dependents with long-term care needs. This is day-one right. This means that there is no minimum service needed.

Practical steps for employers

So, how can employers ensure payroll compliance in these cases? Well, as an employer, you can take the following steps:

- You must set a reminder for April for new updates

- You must test payroll calculations (mainly for SSP, SMP, and SPP).

- You have to update employee handbooks to include family and carer rights.

Workplace pensions: Auto-enrolment duties

In the UK, every employer must follow the auto-enrolment rules for workplace pensions. This means you must put certain staff into a pension scheme and pay money into it. Employees must be auto-enrolled if they are aged 22 up to state pension age and earn at least the set earnings level (for example, around £192 a week, always check the latest figures on The Pensions Regulator website).

Employer contributions and records

Employers must pay at least the legal minimum into the pension, and staff also pay a part. You must keep clear records showing who has been enrolled, how much was paid, and any staff who chose to opt out. Every three years, you must re-enrol staff who are still eligible, even if they previously left the scheme. In case you ignore any rules, you will get penalties.

How to stay on track

To ensure payroll compliance, run a pension-eligibility report. This should be done every time you process payroll. This makes sure no one is missed and that contributions are correct.

Data & record-keeping obligations

Every employer must keep certain records to prove that staff are paid correctly. These records also show that legal rules are followed. This includes:

- Employee personal details

- Records for pay and tax

- Records for National Insurance

- Pension assessments

- Contributions to pension

- Any other payroll-related information

According to HMRC, the records should be kept for at least 3 years. However, most employers keep records longer than this just to be on the safe side.

Protecting payroll data

There is sensitive information stored in payroll, i.e., personal data of the employees. Employees, thus, must take care of payroll’s security, complying with laws such as GDPR. Here are some of the steps they should take:

- The access should be limited so that only the concerned staff can see it

- Systems should be secured, preferably with encryption

- Keep audit logs that track who accessed or changed records

This protects both the business and employees.

Why records matter

Records are not just about doing payroll calculations. They are a major chunk of payroll compliance meaning. They are proof that you acted with reasonable care if HMRC or The Pensions Regulator checks your business. Basically, they depict that you followed the law. You have evidence to prove that. As a result, you are ready for inspection every time.

Controls, processes and tools

Payroll needs to be kept safe and accurate. There are certain controls and processes that can help businesses in this regard. Using these, fraud and mistakes can be prevented. These tools and processes also prove to HMRC that payroll is being managed properly.

Core internal controls

- Duties should be segregated. This means that different people should handle data entry, approvals, and payments.

- There should be reconciliation at the end of every month. For this, check payroll totals against bank payments and HMRC reports.

- Do a sample check. Review a few payslips, each run to confirm pay is correct.

- Keep a clear log of who did what in the system.

- Keep approval gates at every checkpoint. For instance, payroll should not move forward until managers approve.

Technology support

Modern payroll software can make this easier. Useful tools include:

| Technology | What it Does | Examples of Software |

|---|---|---|

| Automated RTI / FPS Submissions | Sends payroll data (wages, tax, NI) directly to HMRC in real time. | Sage Payroll, BrightPay, Xero Payroll, QuickBooks Payroll |

| Automatic Pension Feeds | Connects payroll software to workplace pension providers so contributions are sent automatically. | NEST integration tools, Smart Pension API, The People’s Pension link, Sage Pensions Module |

| Employee Self-Service (ESS) Portals | Lets employees update details, download payslips, and request leave, reducing admin errors. | Sage HR, BambooHR, Fourth Hospitality ESS, HiBob |

| Audit Trail & Reporting Tools | Tracks changes in payroll data, shows who approved, and produces compliance reports. | Fourth, ADP Workforce Now, IRIS Payroll, PayFit |

| Data Security (Encryption & Access Control) | Protects sensitive payroll and employee data; controls who can access it. | Microsoft Azure AD, Okta, Sage Payroll with 2FA, KeyPay |

Training and updates

Payroll rules change often. Staff should stay updated with HMRC bulletins, software release notes, and regular training. Many payroll teams follow CPD (Continuing Professional Development) to keep skills current.

Standard process template

A simple “payroll run SOP” might look like this:

- Data intake (collect hours/salary info)

- Validation (check accuracy)

- Approvals (manager sign-off)

- FPS submission to HMRC

- Payment to staff

- Reconciliation (compare payroll vs. bank/HMRC)

- Archiving records

Practical Payroll Compliance Checklist

Use this payroll compliance guide checklist to stay on track with UK payroll rules. You can copy and keep it as a quick reference:

Immediate actions

The following actions are crucial for payroll compliance. They are your first priority.

- Register for PAYE with HMRC

- Set up RTI reporting.

- Check all employee details (NI number, date of birth, bank details, tax code).

Recurring process items

These steps have to be taken recurrently for successful payroll compliance.

- Create a yearly payroll calendar. This has to include FPS deadlines, P60s, and HMRC year-end dates.

- Set up payroll software for automatic FPS submissions. Do the same for pension feeds.

- Do a monthly payroll reconciliation.

- Check payroll totals vs. bank payments.

- Keep an error log.

- Run quarterly checks on National Minimum Wage (NMW)

- Check pension eligibility quarterly as well.

- Keep payroll records and audit trails safely.

Escalation & governance

For better governance, take the following steps:

- Keep separate duties, i.e., one person enters data, another approves, and so on.

- Set a clear sign-off process for payroll.

- Subscribe to HMRC and The Pensions Regulator updates.

- Test payroll software updates.

- Test vendor patches at least once a year.

Following this checklist reduces mistakes. Your business will be protected from penalties as well. These steps keep your payroll fully legal.

Sector Special Notes for Payroll Compliance

Hospitality & tips

In the hotel industry, tips and service charges are widespread. These must be taxed via payroll. They cannot be used to calculate the National Minimum Wage (NMW). If employees are paid too little in basic pay, the business risks violating the law. This holds even with the tips being paid.

Zero-hours contracts

For zero-hours and casual staff, holiday pay must still be given. Since 1 April 2024, new rules allow “rolled-up holiday pay” for some workers. This means holiday pay is added to each payslip instead of being taken later. Employers must check the GOV.UK guidance to apply this correctly.

International payroll

When paying staff in more than one country, each country has its own tax and employment laws. This can be very complex. Many businesses use Employer of Record (EOR) services. They can also use specialist global payroll providers to manage compliance across borders.

Risks, Penalties, and Enforcement

HMRC wants all employers to exercise “reasonable care” while processing payroll. This means that your records should be up-to-date. You should also be following all laws, and your calculations must be correct. If there are errors due to you being careless, there will be penalties from the HMRC. The penalties are majorly severe if the errors are intentional or hidden.

Penalties and public action

Employers who break payroll rules can face fines. There can also be back payments to staff and interest charges. In serious cases, HMRC publishes a list of businesses that underpaid staff. This is sometimes called “naming and shaming.” For instance, millions have been returned to workers in hundreds of companies. This was a result of enforcement actions over the National Minimum Wage (NMW). Employers who neglect worker pensions may also be subject to fines from the Pensions Regulator. They either have not set up or paid pensions.

Payroll Penalty Table

Here are the rates of penalties that you can get from the HMRC.

| Type of Error | Penalty Rate |

|---|---|

| Careless Inaccuracy (HMRC) | 0%–30% of extra tax due (if unprompted); up to 15%–30% if HMRC prompts you |

| Deliberate Inaccuracy (HMRC) | 20%–70% of extra tax due (unprompted reduces slightly) |

| Deliberate & Concealed (HMRC) | 30%–100% of extra tax due (penalty max if hidden errors) |

| NMW Underpayment Penalty | Up to 200% of the underpaid amount; minimum £100 per notice; capped at £20,000 per worker |

| NMW Penalty Reduction | Reduced by 50% if the unpaid wages and penalty paid within 14 days |

| Naming & Shaming (NMW) | Employers may be publicly listed if arrears exceed £500; significant reputational damage |

How to reduce risk

Employers can protect themselves by keeping strong documentation. They should also have audit trails. They must be testing payroll each month and fixing errors quickly. Some businesses also use payroll insurance to reduce financial risk. Indemnity covers are also an option. Acting early and proving “reasonable care” often reduces penalties.

Where to Get Help: Payroll Compliance Practitioner & Services

Payroll can become complex very quickly. If you manage staff across multiple locations, deal with frequent law changes, the situation might be particularly tricky for you. In these cases, outsourcing to experts can save time and reduce risk. It is best that you speak to a specialist. At Sterling Cooper Consultants, we understand this. Our experienced payroll compliance services experts deal with RTI reporting, automated pension feeds, and keep strong audit trails. We offer you the right setup, checks, and ongoing support.

Struggling With Payroll Compliance?

Sterling Cooper Limited offers expert payroll compliance services to help you meet every HMRC requirement, avoid penalties, and keep your payroll running smoothly. Contact us now and make sure that you never have to worry about requirements or penalties again.

FAQs

Payroll compliance means following all UK laws when paying employees — including tax, pensions, minimum wage, and record-keeping rules.

Yes. Even if you have just one employee, you must register with HMRC, run PAYE, and follow payroll rules.

HMRC may charge a penalty and interest. Always file on or before payday.

Most modern payroll software helps with RTI, pensions, and records, but you must still check settings and updates.

If payroll feels too complex or you risk errors and penalties, a payroll compliance practitioner can handle everything for you.

Recent Posts